On 1 October 2025, the Albanese government launched its expanded 5% deposit scheme for first home buyers, with:

- Unlimited places for first‑home buyers

- No income caps

- Higher property price caps

- No Lenders Mortgage Insurance (LMI)

Prior to expansion, the government reported that more than 185,000 Australians had been supported into home ownership through earlier versions of the scheme (i.e., before 1 October 2025).

The Australian Government has not released any public data on the number of mortgages issued under the expanded 5% deposit scheme.

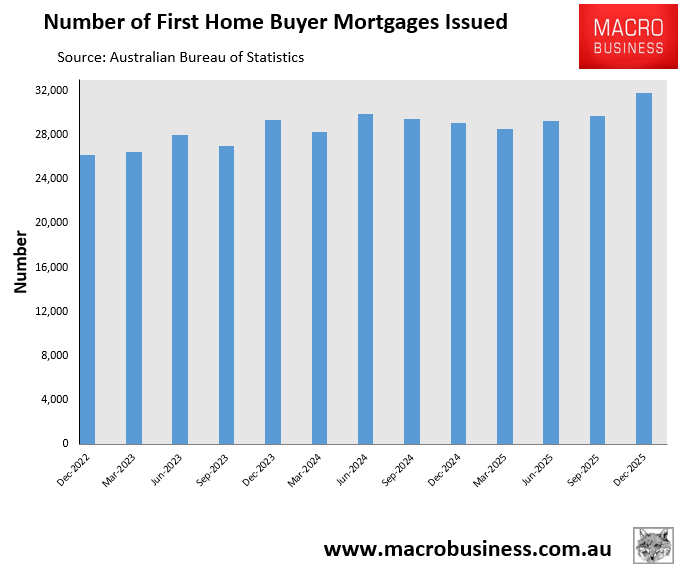

However, the Australian Bureau of Statistics (ABS) did report that the number of first home buyer mortgages issued lifted by 6.8% in the December quarter of 2025, following the expanded scheme’s introduction, to be 9.1% higher year over year:

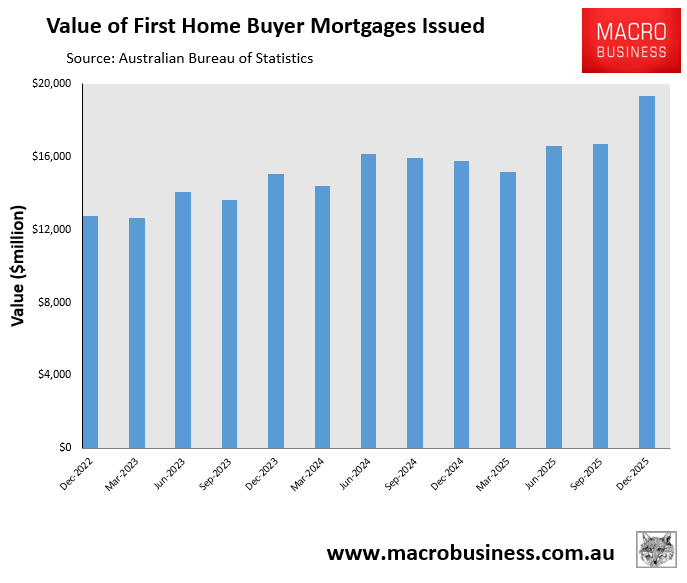

The value of mortgage commitments to first home buyers jumped by 16% on the prior quarter and was the highest value since the March quarter of 2021:

Therefore, it appears that the expanded 5% deposit scheme was well subscribed after its introduction.

Analysis released this week by Equifax suggested that first home buyer demand continued to surge over the first two months of 2026, with first home buyer enquiries for the 18–25 age bracket surging by 9.87% year-on-year in February.

“I think it’s clear that the government’s First Home Buyer Deposit Scheme continues to be a driver of First Home Buyer activity, almost insulating FHBs from the immediate chill of rate hikes”, Moses Samaha, Executive General Manager at Equifax, stated via media release.

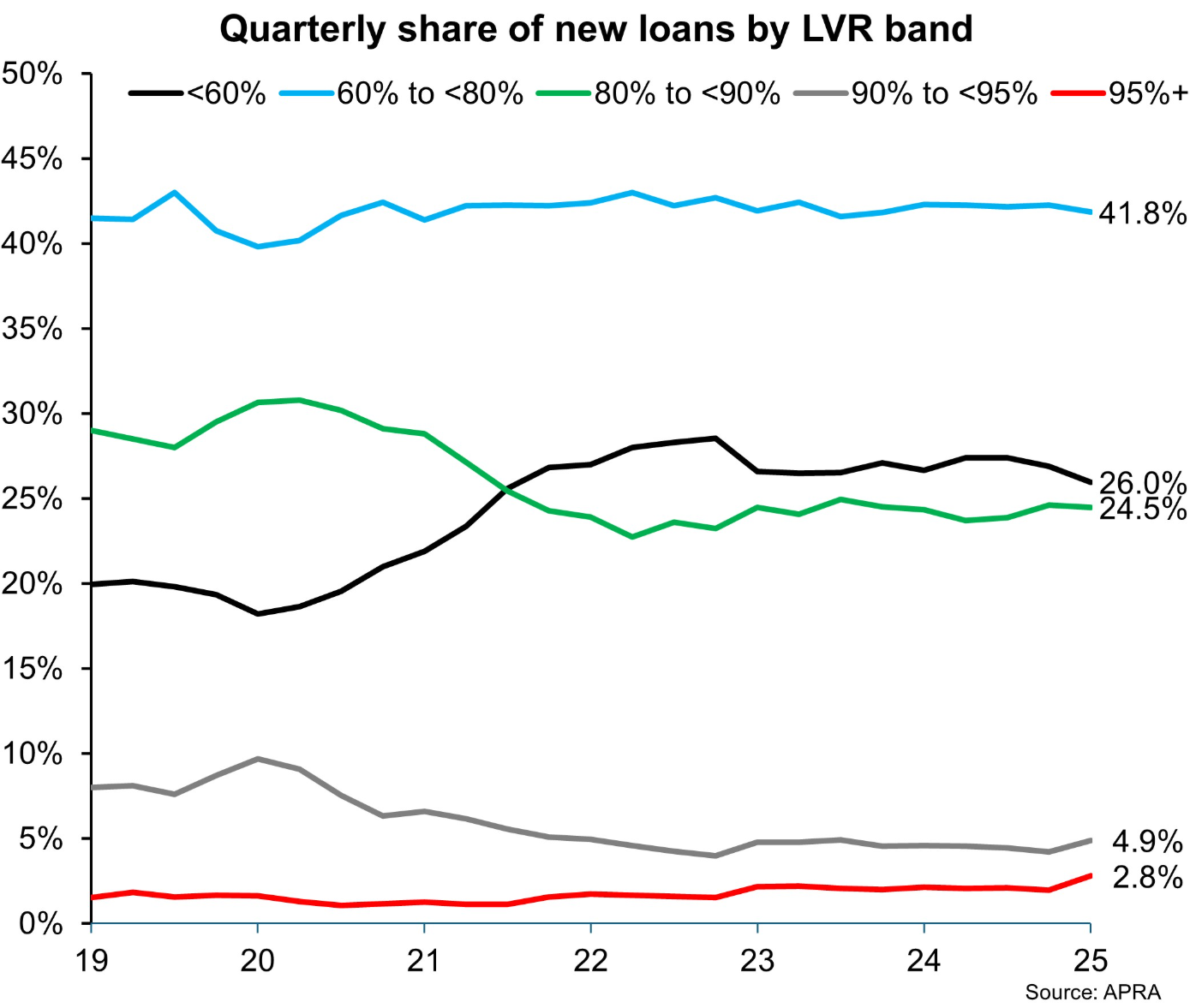

Independent property analyst Cameron Kusher from Oz Property Insights has posted an analysis of the latest Australian Prudential Regulatory Authority (APRA) property exposures data for the final quarter of 2025.

As illustrated below, the share of new mortgages with a loan-to-value ratio (LVR) of 90% to less than 95% was the highest it has been since June 2024 at 4.9%.

The share of new loans with an LVR of 95% or more (2.8%) rose sharply and reached the highest level on record due to the expanded 5% deposit scheme and the launch of the Help to Buy Scheme:

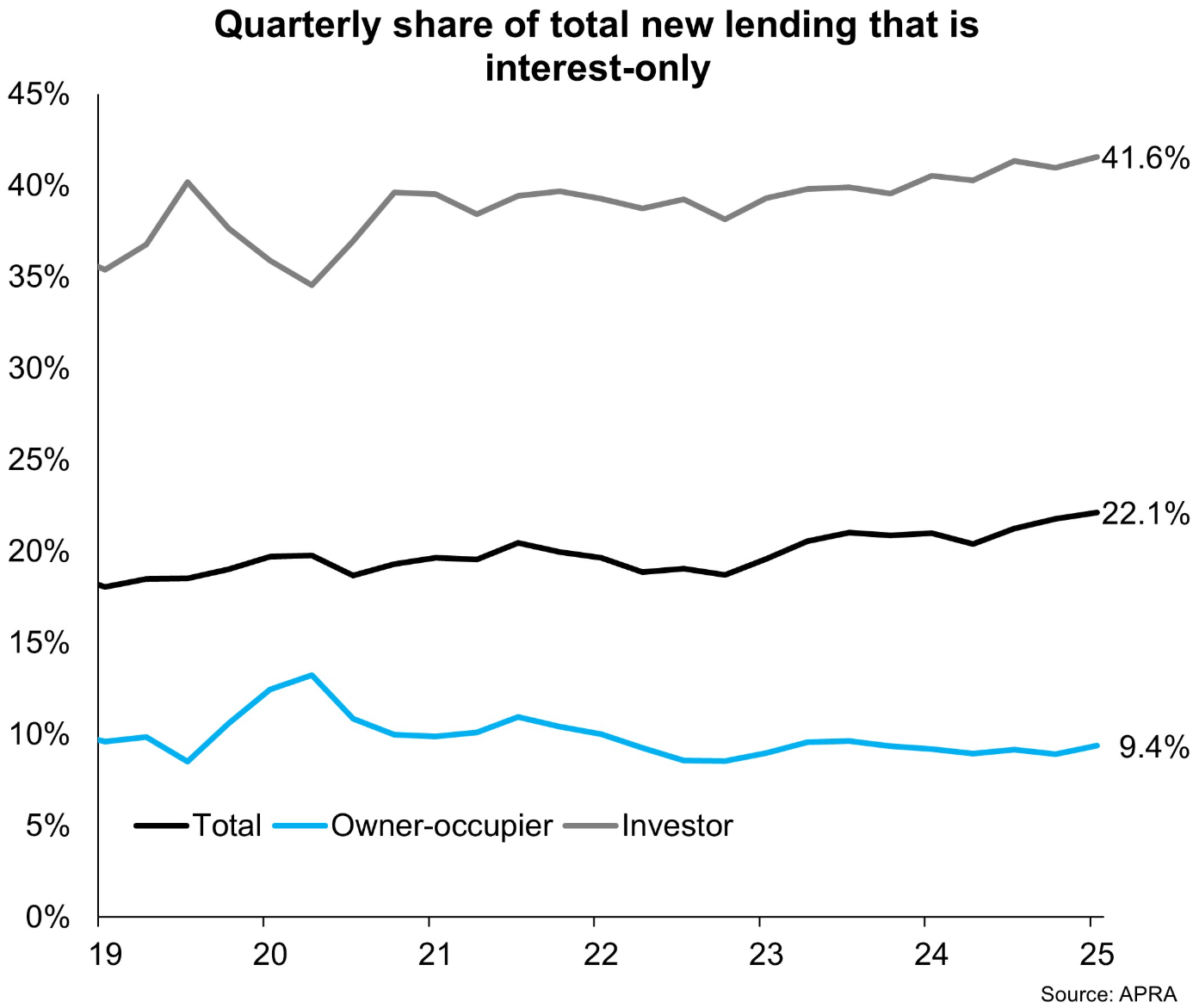

To add insult to injury, 22.1% of all new loans written were interest-only loans in the December quarter of 2025, which was the highest share in records dating back to March 2019.

Most interest-only lending was to investors, where 41.6% of all new loans were on an interest-only basis over the quarter, a historic high:

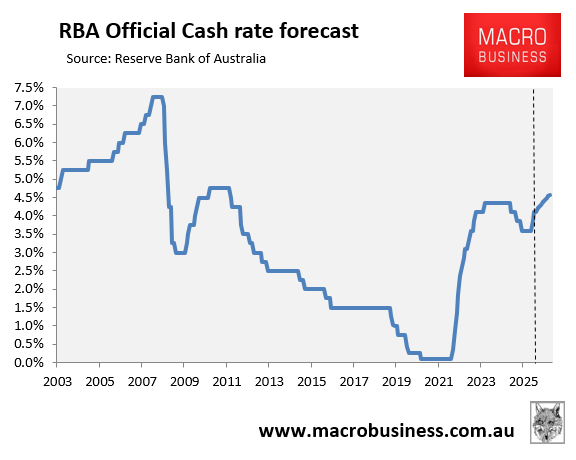

Thus, the data clearly indicates that Australians engaged in riskier mortgage lending in the December quarter of 2025. This is worrying given financial markets have priced a high likelihood of four rate hikes for 2026 (i.e., February’s, March’s and two more):

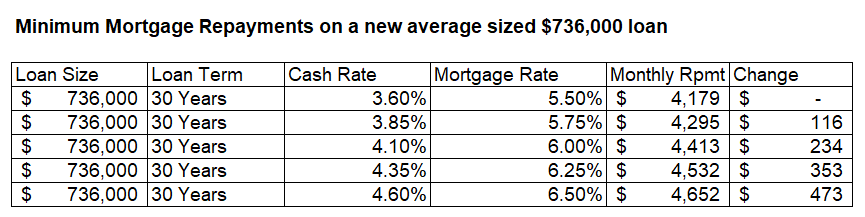

Four rate hikes over 2026 would add around $470 to the average monthly cost of an average $736,000 new mortgage:

Leveraging up into property in a rapidly rising interest rate environment is risky business.