RBA smashes mortgage holders with 0.25% hike

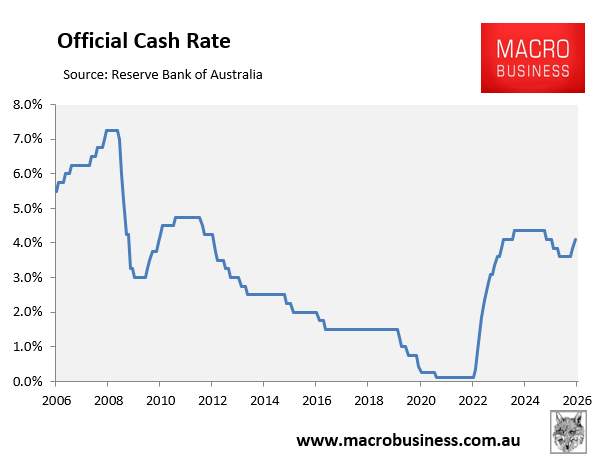

As widely expected, the Reserve Bank of Australia (RBA) has raised the official cash rate by 25 basis points to 4.25%—a back-to-back increase.

The decision was a close call, with five members voting to increase the cash rate target by 25 basis points to 4.10% and four members voting to leave the cash rate target unchanged at 3.85%.

In arriving at its decision, the RBA noted that “some of the increase in inflation reflects greater capacity pressures”, while “the conflict in the Middle East has resulted in sharply higher fuel prices, which, if sustained, will add to inflation”.

Moreover, “short-term measures of inflation expectations have already risen”.

“In large part, higher interest rates reflect expectations for the path of monetary policy, which have risen in Australia and most other advanced economies in response to the expected inflationary implications of the conflict in the Middle East”, the RBA statement read.

The differing opinions on whether to hike rates were in recognition of “the conflict in the Middle East [which] poses substantial risks in both directions”.

Overall, the RBA remains highly concerned about inflationary pressures, which “picked up materially in the second half of 2025”.

“In light of these considerations, the Board judged that inflation is likely to remain above target for some time and that the risks have tilted further to the upside, including to inflation expectations. It was therefore appropriate to increase the cash rate target”.

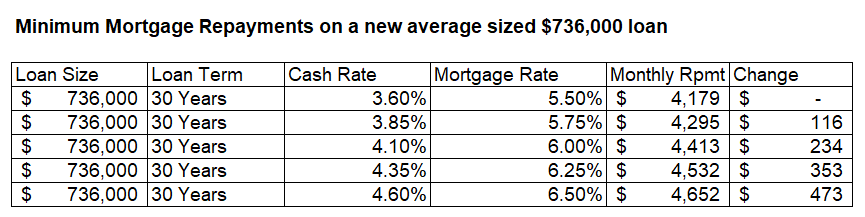

Before the decision, financial markets had tipped four interest rate hikes in 2026 (including February’s and March’s hikes) and a 15-year high cash rate of 4.60% by year’s end:

If these hikes came to fruition, the average new mortgage holder would face a cumulative $473 increase in monthly repayments on the average $736,000 loan:

First home buyers who stretched themselves with mega-mortgages under the Albanese government’s 5% deposit scheme are especially exposed and face extreme mortgage stress and potential negative equity should home prices decline.

In my view, the current situation mirrors the RBA’s aggressive hiking in the lead-up to the Global Financial Crisis (GFC). Except this time, we face a global recession stemming from the war in the Middle East.

I would not be surprised if the RBA cuts rates later in the year, similar to the GFC.