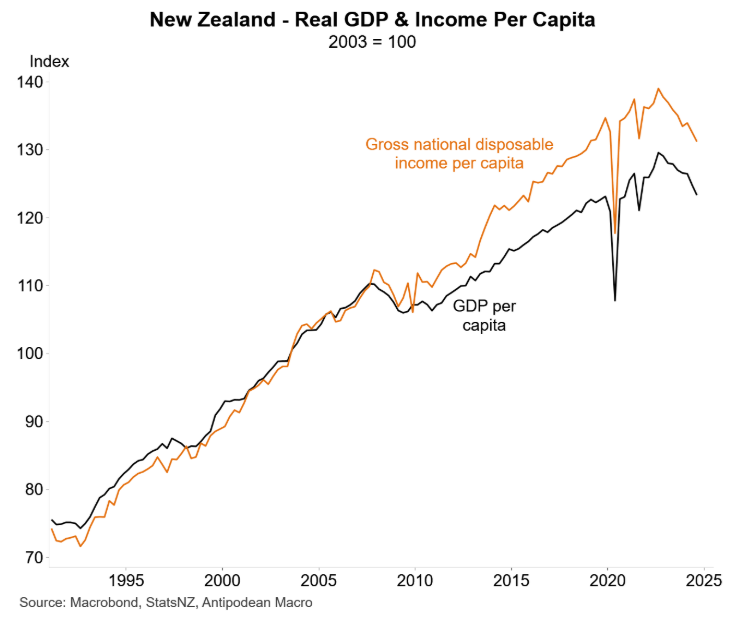

New Zealand is slowly recovering from its sharpest economic downturn since the Global Financial Crisis.

As illustrated below by Justin Fabo from Antipodean Macro, real GDP and income per capita have fallen sharply from their recent peak:

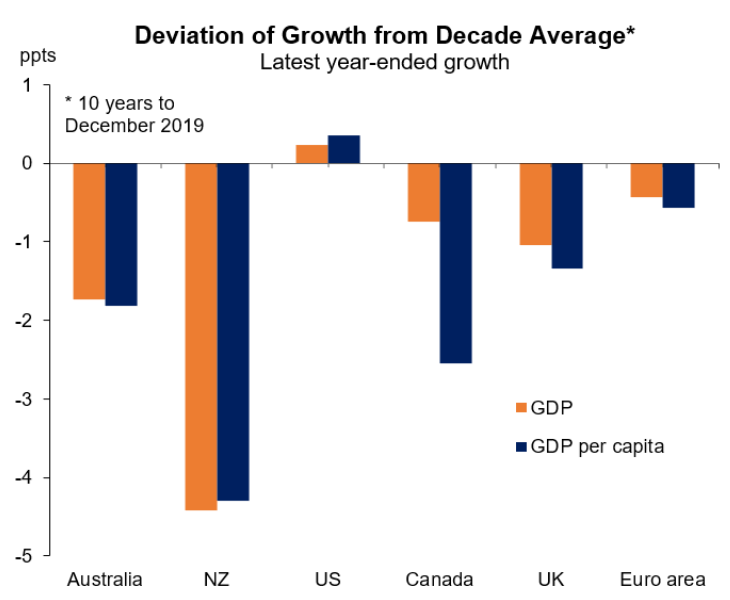

New Zealand’s decline in real GDP per capita is among the sharpest in the advanced world:

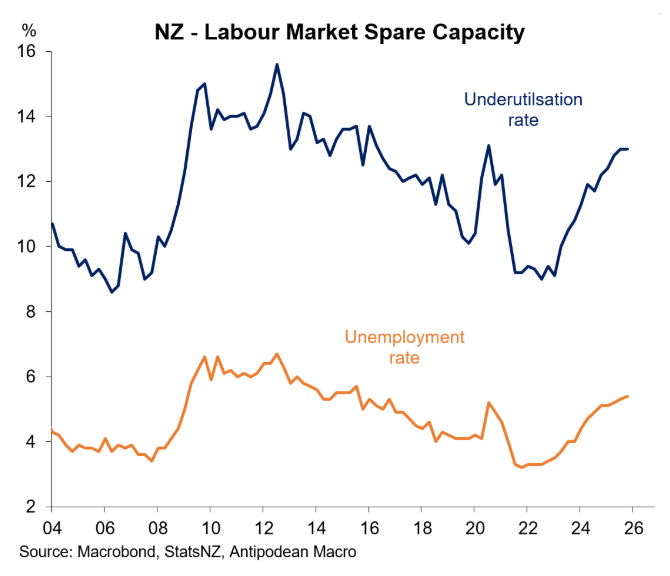

New Zealand’s unemployment and underemployment rates have also lifted sharply:

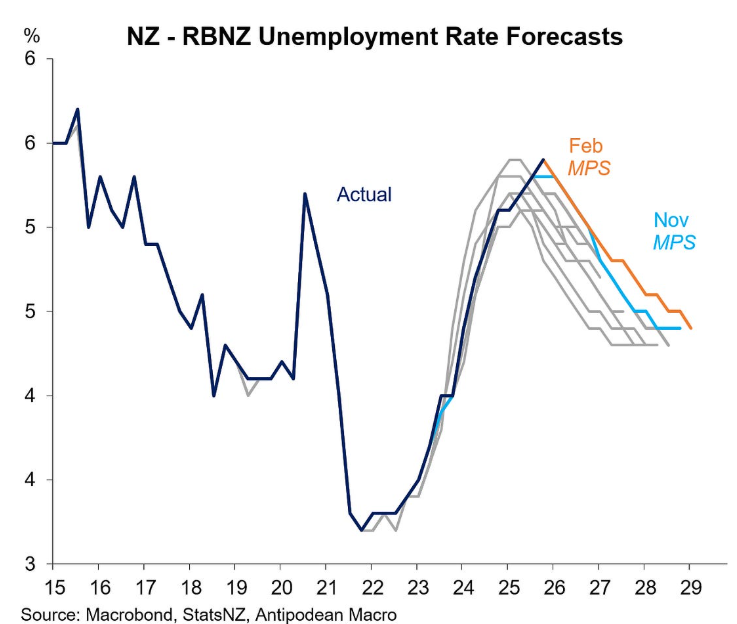

And while the Reserve Bank forecasts the unemployment rate to fall over 2026, it will be a slow grind, given that New Zealand house prices continue to decline in real terms.

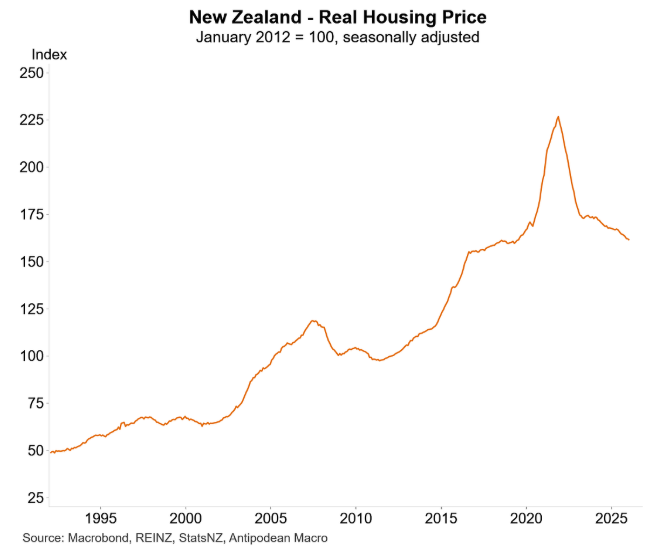

New Zealand house prices have declined by 16.2% from their previous market peak in early 2022 and by more than 30% in real inflation-adjusted terms back to 2019 levels:

ANZ forecasts only 2% price growth in 2026, below inflation (3.1%), implying real prices will continue to fall.

Liam Dann, business editor at the New Zealand Herald, warns that the slowdown in housing and construction has left a “villa‑shaped hole” in the economic recovery. However, the realignment will likely be healthy in the long-term, argues Dann, with the economy undergoing “resistance training”, i.e., “we are making the economy sweat” and rebuilding without relying on housing bubbles or high immigration.

Dann sees four significant benefits from having an economy that is no longer built upon high migration and housing speculation:

- More productive investment in businesses rather than property.

- Real wealth creation instead of paper gains.

- Gradual improvement in housing affordability.

- Possible social benefits from a less distorted housing market.

“If we can achieve stable growth with lower unemployment and higher wages without falling back on the familiar props of high immigration and housing bubble, we will have achieved something significant”, Dann says.

“We’ll have created a more solid foundation on which to build our long-term economic goals”.

Separately, Simplicity’s Shamubeel Eaqub argued that much of New Zealand’s post‑2000 growth was low‑quality and inflated by property speculation, not productivity.

Eaqub says that New Zealand can grow without a housing boom but cautions that the mortgage market is a major source of capital for small businesses. When house prices don’t rise, less equity is available to borrow against, which can slow business investment.

Thus, growth is possible, but recoveries may be slower and less “supercharged”.

The Takeaway:

New Zealand’s economy appears to be entering a new phase in which income expectations, not house prices, drive spending, and regional and export sectors lead growth.

Housing will play a smaller, more muted role, likely resulting in a slower, more uneven recovery, as consumers adjust their spending habits in response to shifting income expectations rather than relying on fluctuating house prices.

However, the economy could emerge healthier and more productive than the old growth model, no longer distorted by asset speculation and focused on real investment and innovation in various sectors, leading to sustainable economic growth and improved living standards for the population.