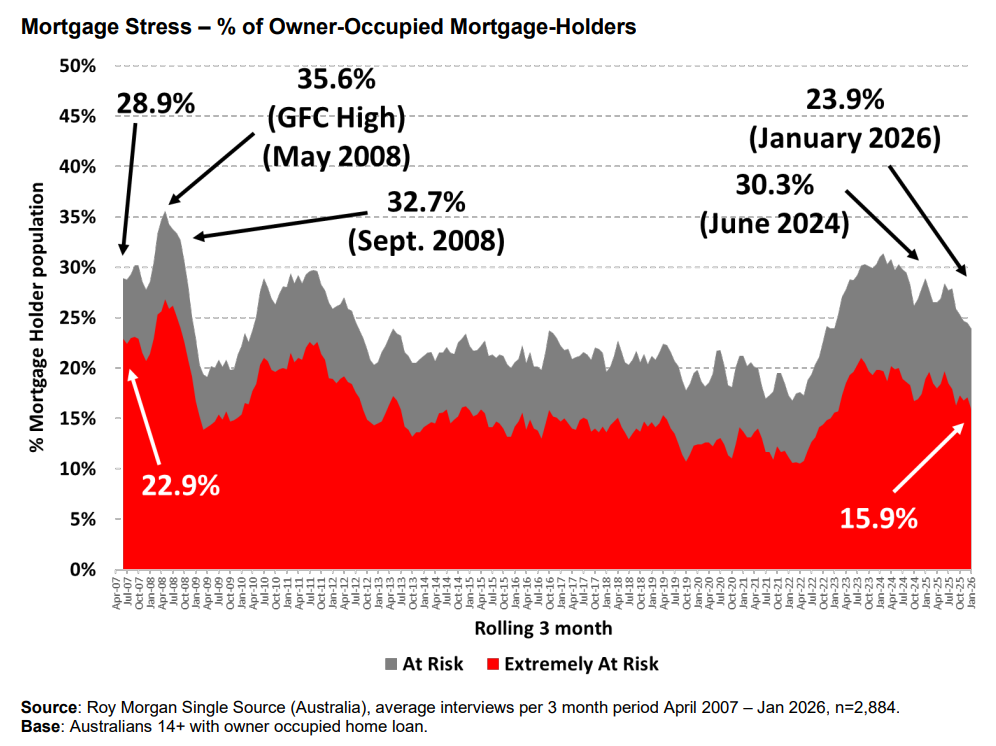

Roy Morgan’s latest mortgage stress report notes that the risk of mortgage stress fell to its lowest for three years in January, before the Reserve Bank of Australia (RBA) hiked the official cash rate:

Roy Morgan estimates that 23.9% of mortgage holders (1,184,000) were ‘At Risk’ of ‘mortgage stress’ in January 2026, down 4% from August 2025 and the lowest share since January 2023.

However, this is where the good news ends.

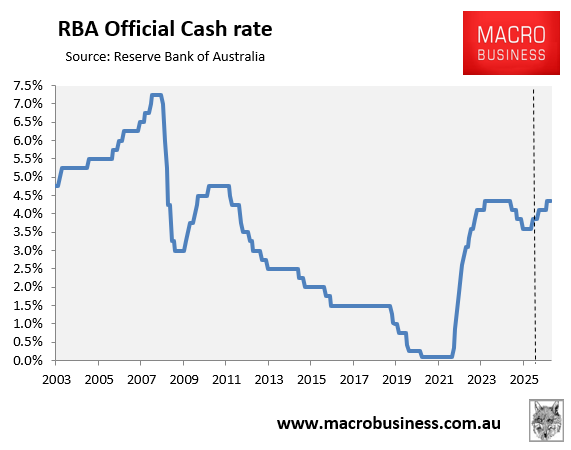

The RBA hiked the official cash rate by 0.25% in February and is widely tipped to hike again in May and then again later in 2026.

In fact, the interest rate futures market has priced a low probability of a fourth 0.25% rate hike by the end of 2026, although three hikes are the base case:

If the RBA were to hike two more times this year, the official cash rate would return to its recent peak of 4.35%:

As a result, the discount variable mortgage rate would increase from its pre-tightening level of 5.50% to 6.25%.

The average new mortgage size in Australia was $736,000 in the December quarter of 2026, according to the Australian Bureau of Statistics (ABS). Three 0.25% rate increases imply a cumulative increase in monthly mortgage repayments of $353:

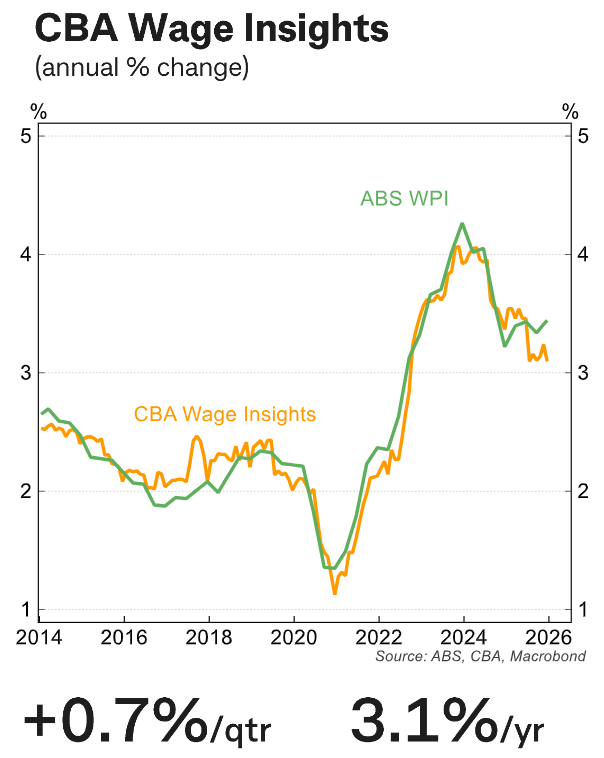

At the same time, Australian wage growth is slowing and tracking well below inflation:

This means that real wages will erode as rising inflation eats away at purchasing power.

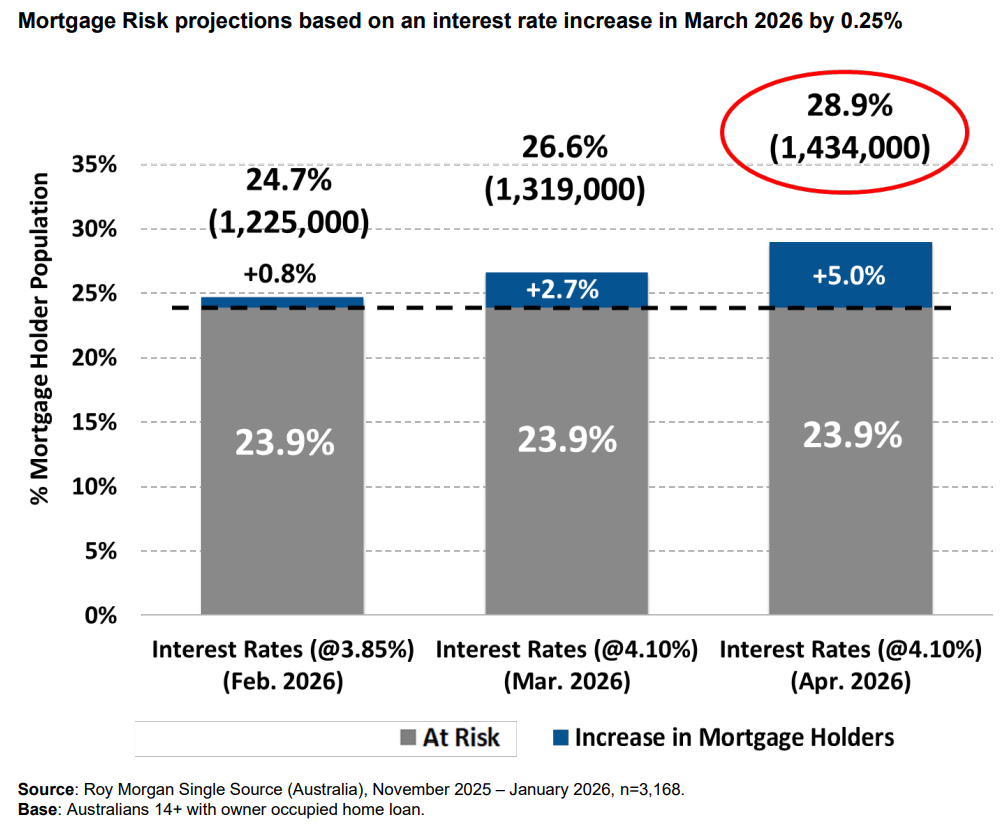

Roy Morgan estimates that “if the RBA increases interest rates next week, the share of mortgage holders ‘At Risk’ would increase to 28.9% in April – up 5% points from now and equivalent to 1,434,000 mortgage holders, up 250,000 from now”:

Obviously, this analysis hasn’t factored in a second, or possibly even a third, rate hike this year, which would lift mortgage stress back towards its recent peak in mid-2024.

Recent first-home buyers who utilised the government’s 5% deposit scheme and borrowed heavily are most exposed to rate hikes.

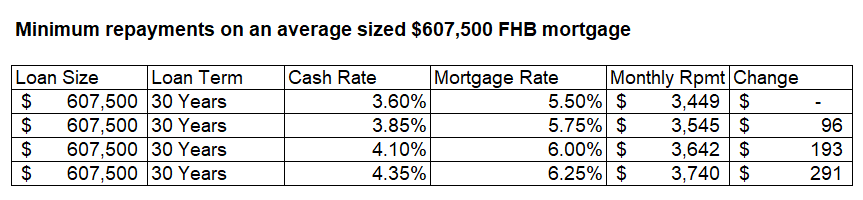

According to the ABS, the average first home buyer mortgage was $607,500 as of the December quarter, although buyers utilising the 5% deposit scheme may have borrowed more.

As illustrated below, three 0.25% rate hikes imply a cumulative $291 per month increase in repayments on the average first home buyer mortgage:

Recent first-home buyers who leveraged themselves to purchase in Sydney and Melbourne should be feeling especially vulnerable, given that home prices in these two markets are facing imminent price falls.

SQM Research’s Louis Christopher gave the following predictions on Monday regarding Sydney and Melbourne home prices:

“We have downgraded our forecasts with this revision for Sydney and Melbourne. We’re now expecting housing price falls in Sydney by the order of up to 6% for the course of 2026 and for Melbourne up to 4% for the course of 2026”.

Thus, recent first home buyers in these two markets face the real prospect of falling into both mortgage stress and negative equity.