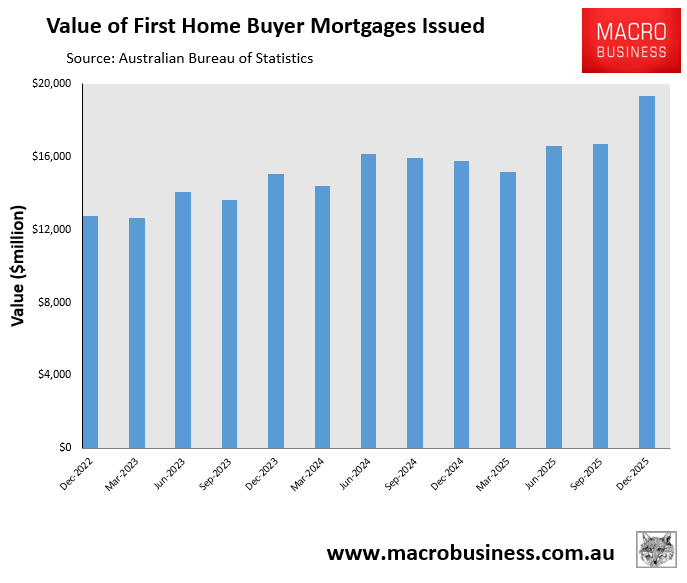

The recent housing finance data from the Australian Bureau of Statistics (ABS) revealed that over the December quarter of 2025, $19.310 billion in mortgages was lent to first-home buyers. This was an increase of 16% over the prior quarter and the highest value since the first quarter of 2021:

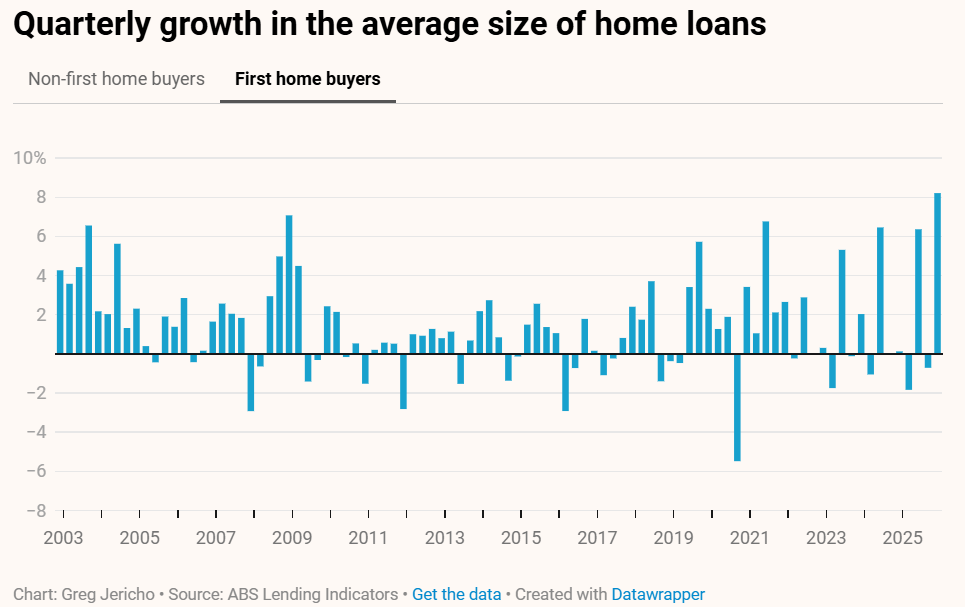

The average size of first-home buyer mortgages also surged by a record 8.3% in the December quarter of 2025 to a record high of $607,500:

Chart by Greg Jericho (The Guardian)

It has been revealed that 22,921 guarantees were issued under the federal government’s 5% mortgage deposit scheme for first-home buyers in the four months since it underwent a major expansion on 1 October 2025.

This represents a 75% rise compared to the previous four-month period between June and September, in which 13,105 guarantees were issued.

Almost two-thirds of properties purchased under the scheme in the four months since October were houses, while under-30s make up two-fifths of those who have benefited from the scheme in that time.

AMP deputy chief economist Diana Mousina told The ABC that the figures from the past four months represented a “massive jump”.

“We know that incentives really matter in the housing market”, she said. “Whenever we get some sort of grants or discounts, we always see a big take-up of these things”.

The demographic breakdown shows the scheme is being used mostly by groups already relatively advantaged, namely:

- Under‑30s make up 40% of participants.

- Regional buyers account for almost 30% (10,700 people).

- Houses (not units) make up nearly two‑thirds of purchases.

- Key workers represent 18%.

- Single parents have a relatively low uptake.

“I don’t think this scheme is good overall because it’s just another demand-side policy, which increases prices over the long term—that’s fundamentally the flaw with it”, Mousina said.

“We haven’t seen a commensurate increase in supply. We have more people wanting to get into the market but supply hasn’t really moved in line with demand”.

“That’s why it’s just going to add to price pressures”, she said.

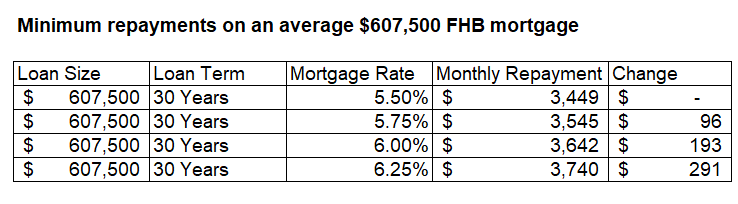

According to the ABS, the average loan size to first home buyers was $607,500 as of the December quarter of 2025:

This means that the 0.25% rate hike delivered last month by the Reserve Bank of Australia (RBA) added $96 to the average monthly cost of a new first-home buyer mortgage.

The interest rate futures market expects the RBA to raise the cash rate again in May, with a very high probability of another hike before the end of 2026.

Should the RBA raise the official cash rate two more times to 4.35% (the previous peak level), it would add a cumulative $291 to the monthly servicing cost of the average first-home buyer mortgage.

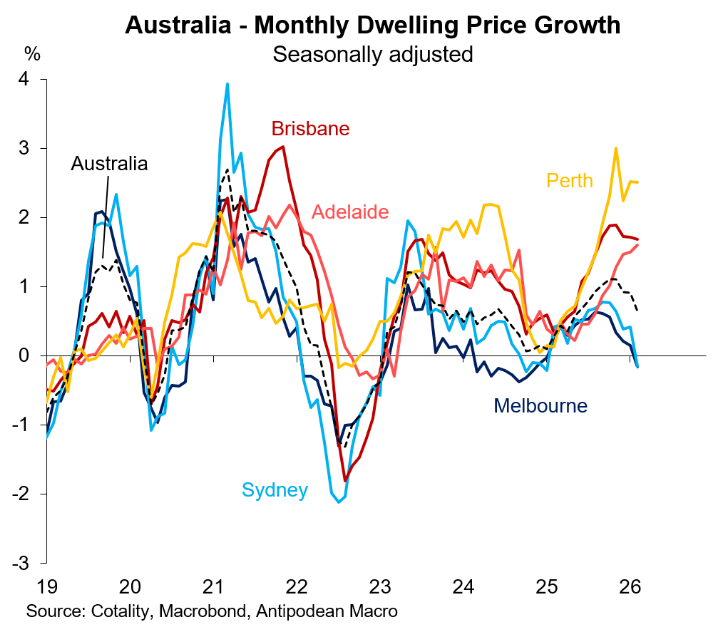

Recent borrowers who extended themselves using the 5% deposit scheme face extreme mortgage stress and the possibility of falling into negative equity if the housing market experiences a significant price correction, as appears to be likely in Sydney and Melbourne:

Chart by Justin Fabo from Antipodean Macro

Mortgage delinquencies also expose Australian taxpayers to possible losses.

Unfortunately, first home buyers have been drawn into the market at a potentially pivotal point. Many could end up as collateral damage in the RBA’s struggle to keep inflation under control.

They will be urgently hoping that the financial markets are wrong and that the RBA does not continue to tighten interest rates.

If you want to save thousands of dollars on mortgage payments, use the MB Compare n Save mortgage comparison tool. It’s quick and easy.

If you decide to refinance, Compare n Save will handle the transaction.