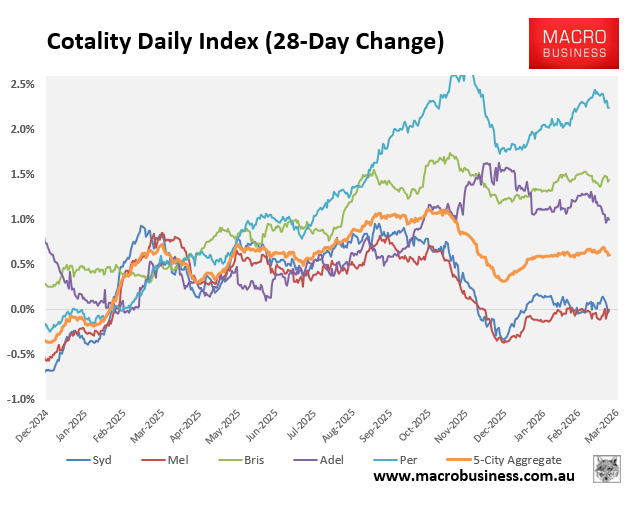

So far, Cotality’s daily dwelling values index is holding up amid back-to-back interest rate hikes by the Reserve Bank of Australia (RBA).

At the 5-city aggregate level, dwelling values have risen by 0.6% over the past 28 days, although there is wide variation across the major markets.

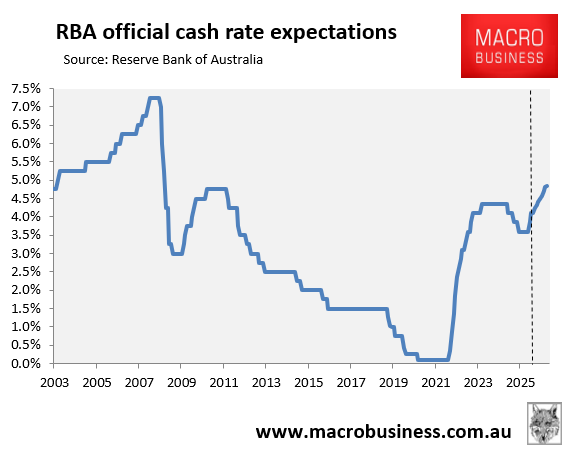

The interest rate futures market has fully priced three more rate hikes for 2026, which would take the official cash rate to 4.85% by year’s end, a 16-year high:

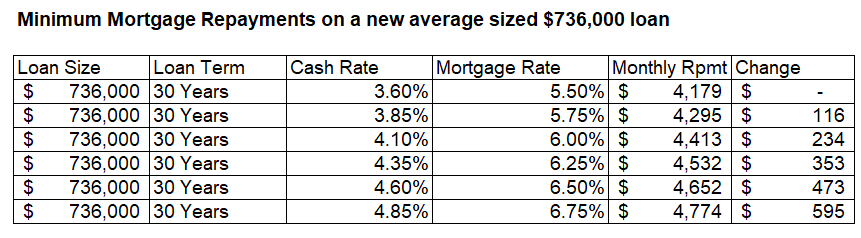

If these interest rate forecasts were to come to fruition, monthly repayments on the average-sized new mortgage would increase by $595 per month, compared with what they were before the RBA’s first hike in February:

Dale Gillham, founder and chief analyst at Wealth Within, and Ray White Group Chief Economist Nerida Conisbee told Realestate.com.au that Australian house prices will remain resilient because demand remains strong, migration is high, and construction is failing to keep up, creating a structural housing shortage.

Australia’s chronic undersupply is the dominant force that will keep prices elevated, they say.

High migration is adding demand faster than homes can be built. Construction delays, labour shortages, and high building costs are limiting new supply.

As a result, they argue that prices can’t meaningfully fall when there aren’t enough homes.

I am not so sure. Australia’s two most similar economies—New Zealand and Canada—have experienced major declines in house prices.

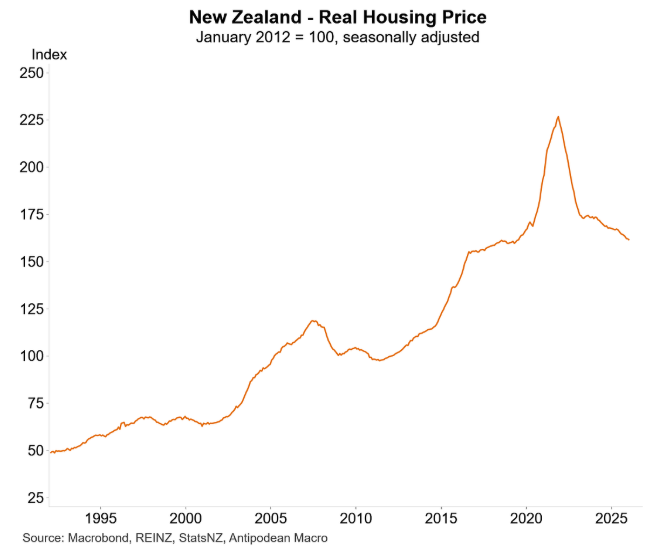

New Zealand house prices have declined by 16.2% from their previous market peak in early 2022 and by more than 30% in real inflation-adjusted terms back to 2019 levels:

Chart by Justin Fabo from Antipodean Macro

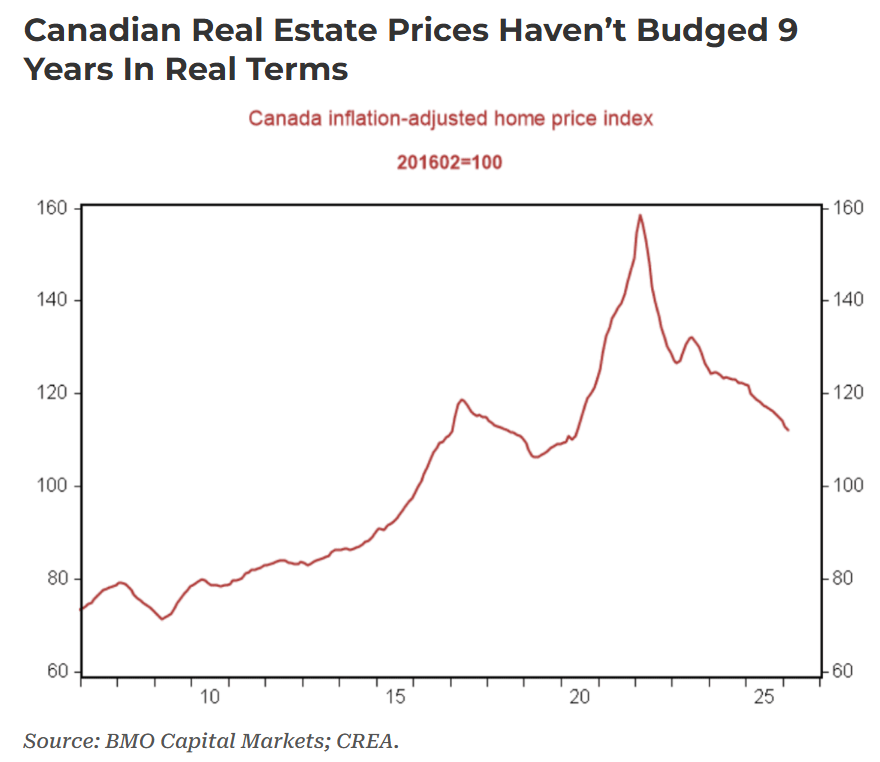

Canadian house prices have fallen 20.1% from their peak, taking real inflation-adjusted values back to 2017 levels:

If Australia’s two most similar housing markets can experience sharp house price declines, could Australia’s housing market experience a similar fate?

After all, Australian housing valuations are extreme, making prices vulnerable to a severe correction or crash as interest rates rise.

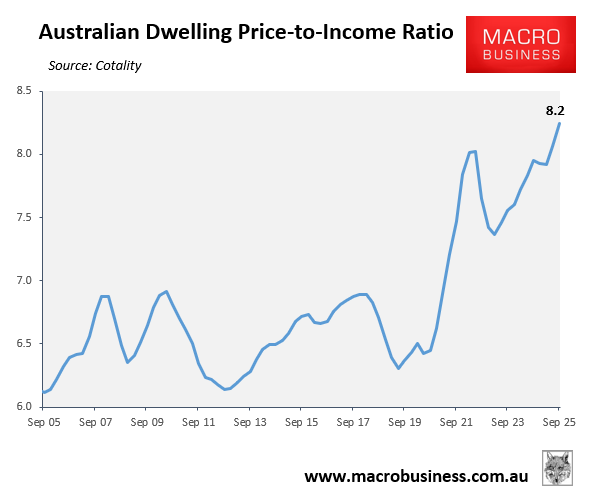

According to Cotality, Australia’s dwelling value-to-income ratio was tracking at a record high of 8.2 in the September quarter of 2025. It would be higher now.

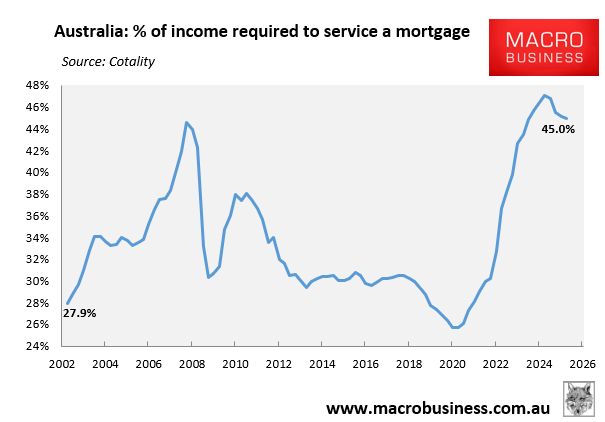

The share of median household income required to service a new mortgage on the median-priced home was also tracking at a historically high level of 45.0% in the September quarter of 2025, before the latest series of rate hikes from the RBA:

If the RBA does hike a cumulative 1.25% over 2026, as predicted by financial markets, then mortgage repayments relative to household incomes would rise to their highest level in history.

The ‘fear of missing out’ may eventually transform into a ‘fear of overpaying’ as a result of the reduced mortgage affordability and borrowing capacity or a sharp rise in unemployment. This could then result in a sharp reduction in demand and a severe price correction.

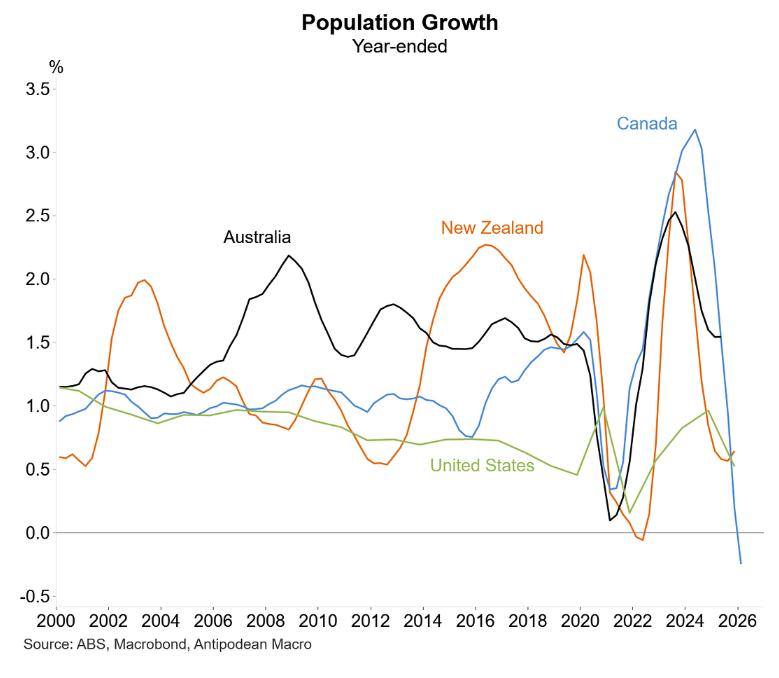

That said, one of the most significant distinctions among Australia, New Zealand, and Canada is that immigration remains at historically high levels in Australia. In contrast, it has fallen sharply in the other two countries.

Chart by Justin Fabo from Antipodean Macro

Consequently, the housing market in Australia is significantly undersupplied, whereas it is oversupplied in Canada and New Zealand.

Even so, I would be very wary of borrowing large sums of money to buy into Australia’s housing market. At some point, gravity will take hold.