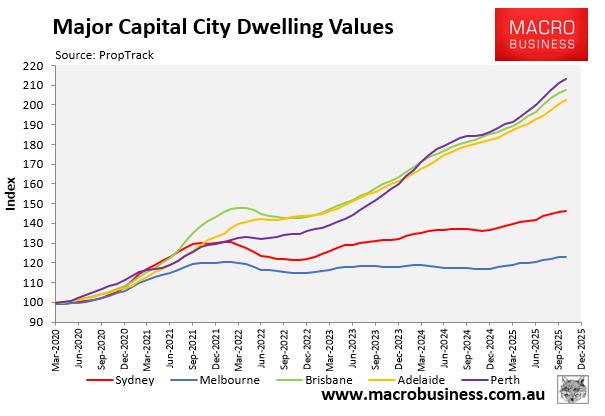

Since the COVID-19 lockdowns began in Australia in March 2020, housing prices in the country’s largest cities have grown at dramatically different rates.

As shown below using PropTrack data, home values in Brisbane, Perth, and Adelaide have roughly doubled, whereas values in Sydney and Melbourne have grown at significantly slower rates.

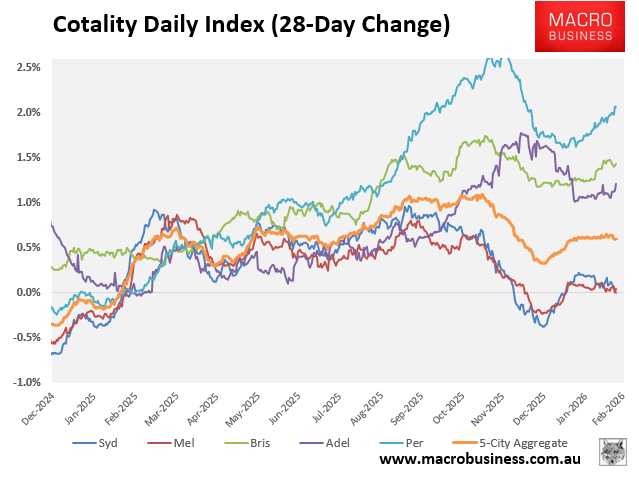

According to Cotality’s daily dwelling values index, home values continue to grow at significantly faster rates in Perth, Brisbane, and Adelaide than in Sydney and Melbourne, where growth has stalled.

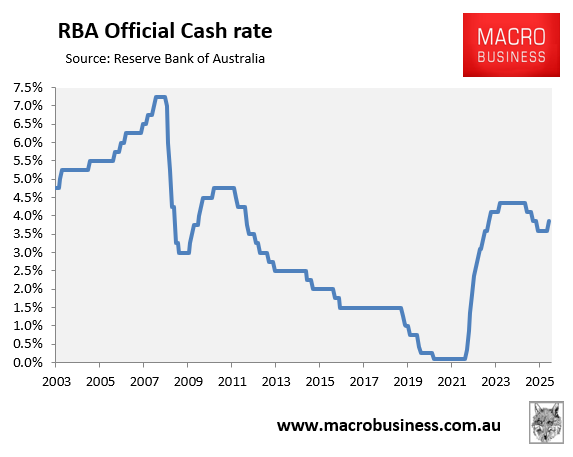

Michael Matusik published an interesting article last week examining why some markets perform so much more strongly than others, despite experiencing the same interest rates.

Matusik argued that interest rates influence behaviour at the margins but do not determine prices. Housing markets diverge because they are fundamentally local, shaped by population, jobs, wages, supply, and demographics—not by a single national cash rate.

Recent experience highlights Matusik’s argument. Interest rates rose more than 400 basis points, yet price outcomes varied dramatically.

If interest rates were the primary driver, markets would have moved together. But they didn’t. Smaller capitals like Brisbane, Adelaide, and Perth massively outperformed Sydney and Melbourne despite identical mortgage rates and lending rules.

Instead, Matusik identifies seven indicators that actually drive housing growth, namely:

- Population growth–must rise meaningfully above long‑term trends.

- Employment growth–durable, high-quality job creation matters more than temporary projects.

- Real wages–rising inflation‑adjusted incomes support sustained price growth.

- Tight supply–low resale stock, low rental vacancies, and constrained new construction pushes prices up.

- Undervalued housing–locals buying, renovating, and investing are early signals of genuine value.

- Demographic mix–long-term growth requires younger buyers and upgraders, not just downsizers.

- Education–strong school catchments create micro‑markets that outperform.

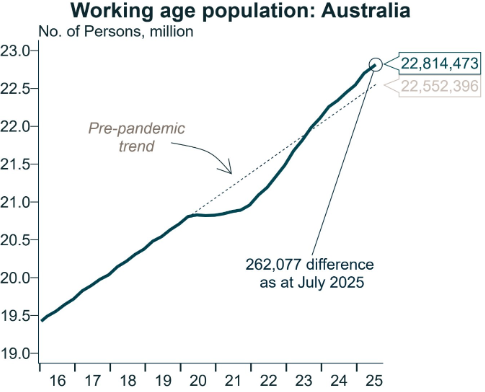

Six months ago, Alex Joiner, chief economist at IFM Investors, published charts showing how the working-age population growth has differed across markets versus the pre-pandemic trend.

At the national level, Joiner estimated that the working-age population was 262,077 larger than inferred by the pre-pandemic trend as at July 2025.

Source: Alex Joiner (IFM Investors)

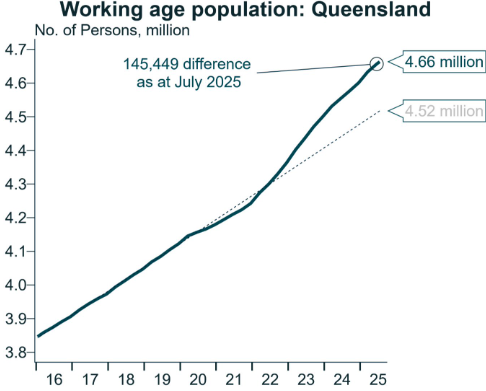

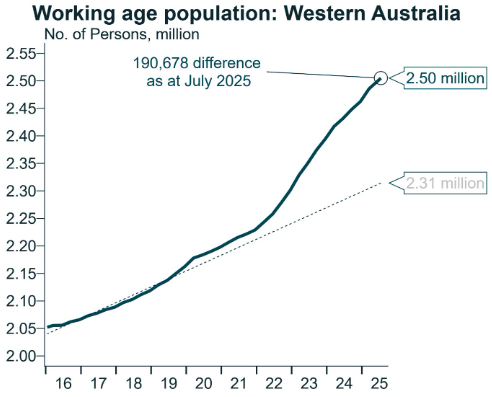

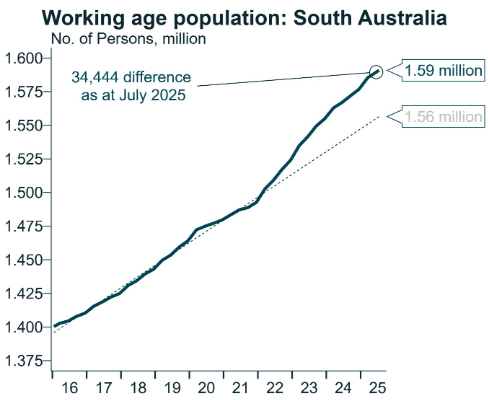

The stronger population growth nationally was driven by Queensland, Western Australia, and South Australia.

Queensland’s resident population was tracking 145,449 above the pre-pandemic trend as of July 2025:

Source: Alex Joiner (IFM Investors)

Western Australia’s population was tracking 190,678 above its pre-pandemic trend as of July 2025:

Source: Alex Joiner (IFM Investors)

South Australia’s population was tracking 34,444 above its pre-pandemic trend as of July 2025:

Source: Alex Joiner (IFM Investors)

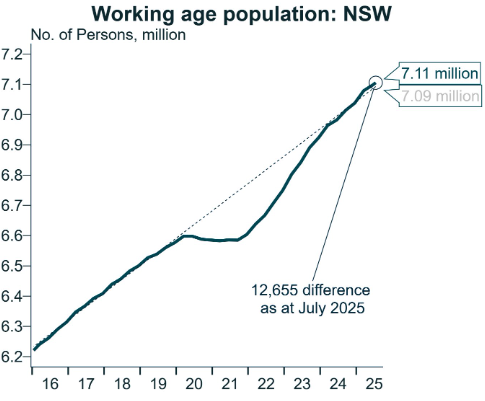

Meanwhile, population growth in New South Wales, where Sydney has experienced softer (albeit still solid) price growth, was tracking bang in line with the pre-pandemic trend as of July 2025:

Source: Alex Joiner (IFM Investors)

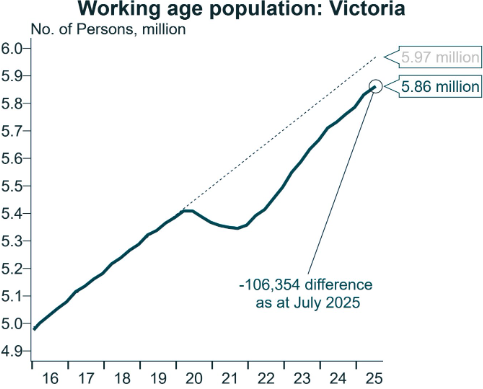

Finally, Victoria’s population was tracking 106,354 behind the pre-pandemic trend as of July 2025. This helps to explain Melbourne’s soft price growth:

Source: Alex Joiner (IFM Investors)

The sharp divergence in price growth between Brisbane, Perth, and Adelaide versus Sydney and Melbourne partly reflects the divergence in population growth relative to pre-pandemic norms.

Another factor is the relative shortage of homes for sale in Brisbane and Perth (less so in Adelaide) versus Sydney and Melbourne, which are relatively well supplied:

Source: Cotality