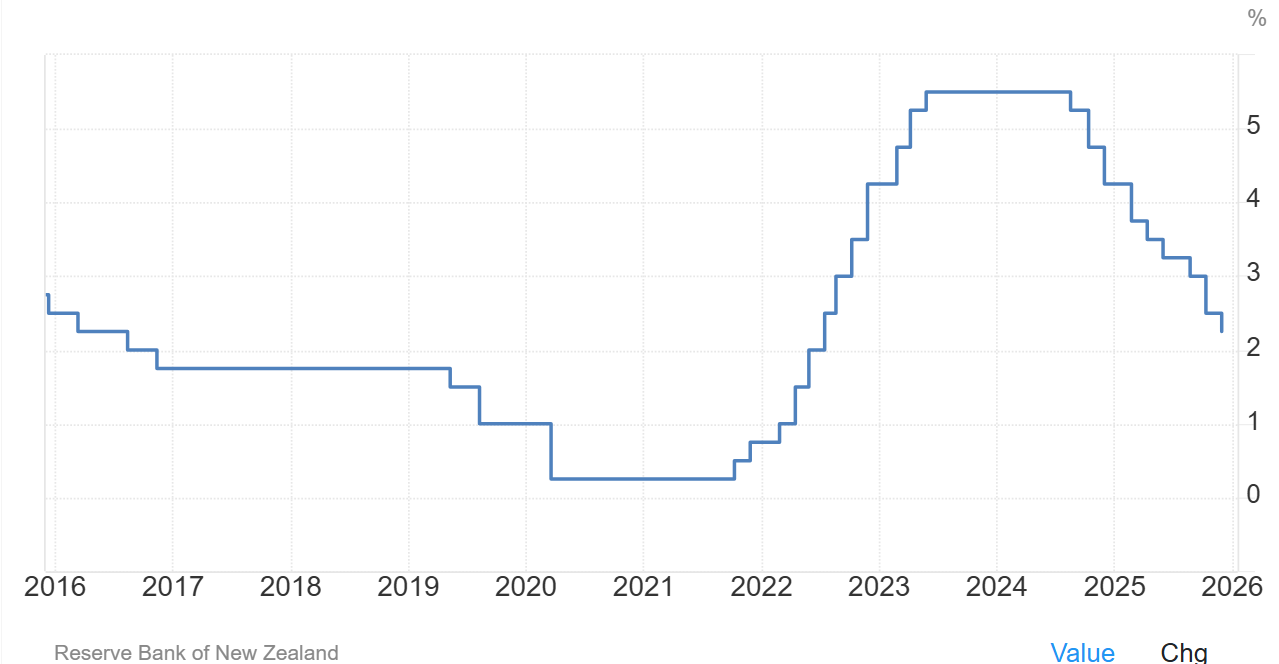

The Reserve Bank of New Zealand has slashed the official cash rate (OCR) by half (2.25%) since mid-2024:

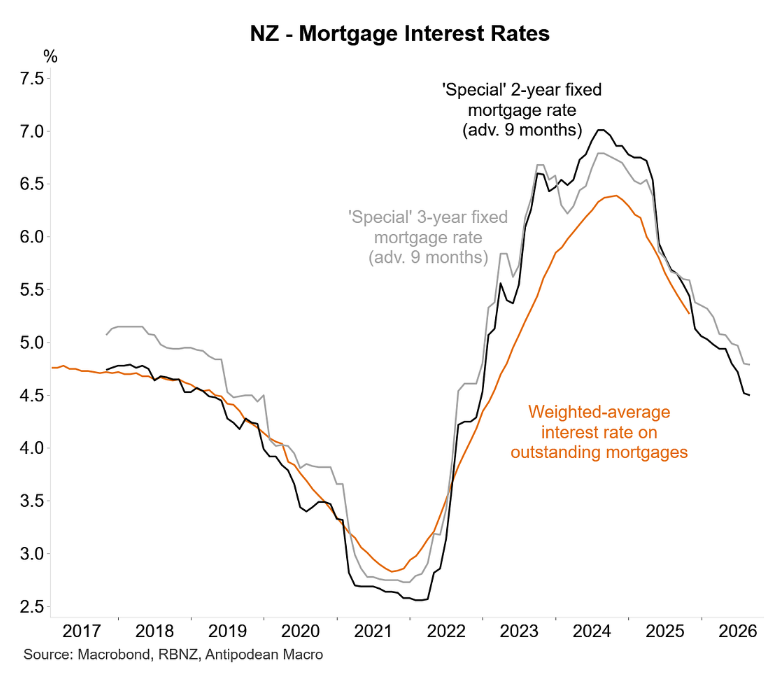

These rate cuts by the Reserve Bank have reduced mortgage borrowing costs dramatically, as illustrated below by Justin Fabo from Antipodean Macro:

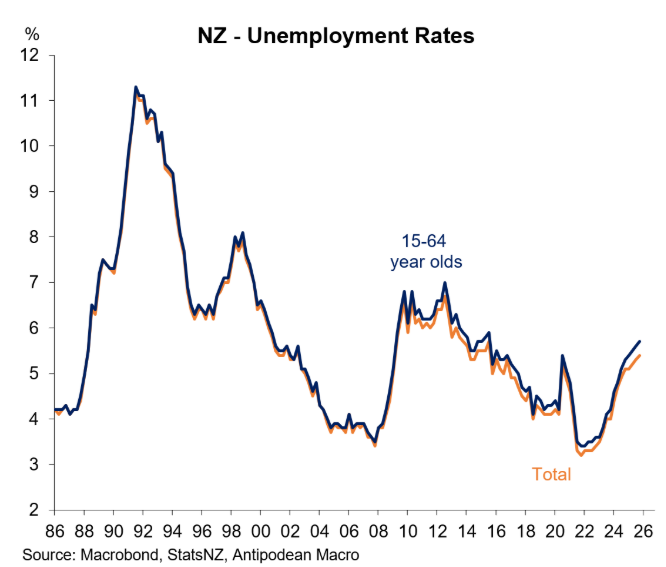

Normally, such a sharp reduction in interest rates would stimulate activity, leading to a rebound in the labour market.

However, despite showing recent improvement and climbing out of recession, New Zealand’s economy remains soft.

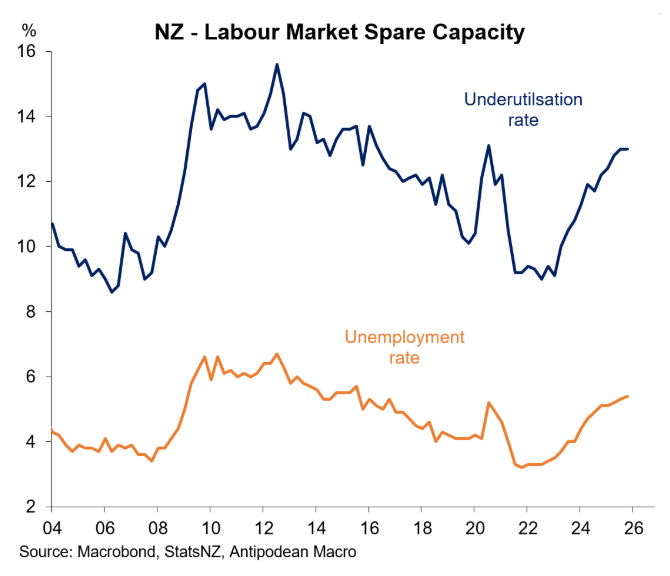

Nowhere is this more apparent than in the labour market, where New Zealand’s unemployment rate continues to climb.

Data released on Wednesday by Stats NZ showed that the nation’s unemployment rate lifted to 5.4% in the December quarter, its highest level in a decade:

The result disappointed economists’ expectations, with most bank economists expecting the unemployment rate to remain the same as the September quarter—i.e., holding at 5.3%.

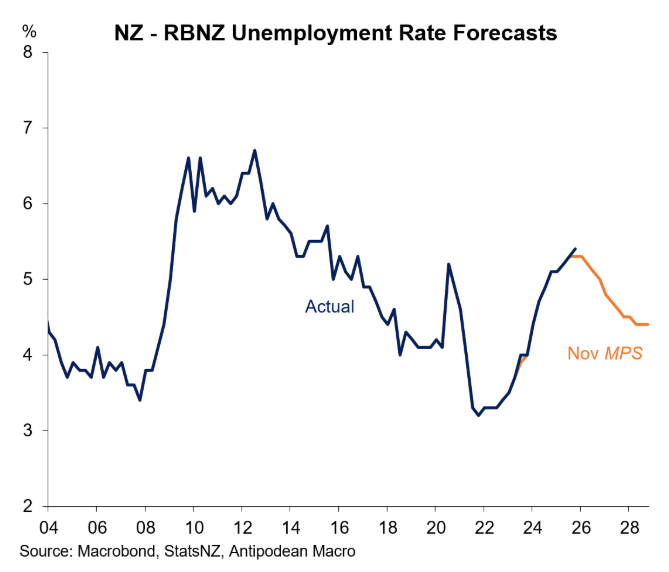

As illustrated below by Justin Fabo, New Zealand’s unemployment rate is tracking above the Reserve Bank’s forecast:

The Reserve Bank’s November Monetary Policy Statement forecast that the unemployment rate would remain at 5.3% for the December quarter as well as the March 2026 quarter before slowly falling.

New Zealand’s underutilisation rate—i.e., unemployment and underemployment combined—also remained at a post-pandemic high of 13.0% in the December quarter, suggesting the labour market remains fragile:

While there are certainly green shoots emerging, such as the recent decline in job ads and vacancies and the positive employment growth recorded in Q4, the data strengthens the case for another rate cut from the Reserve Bank at its upcoming meeting on 18 February.

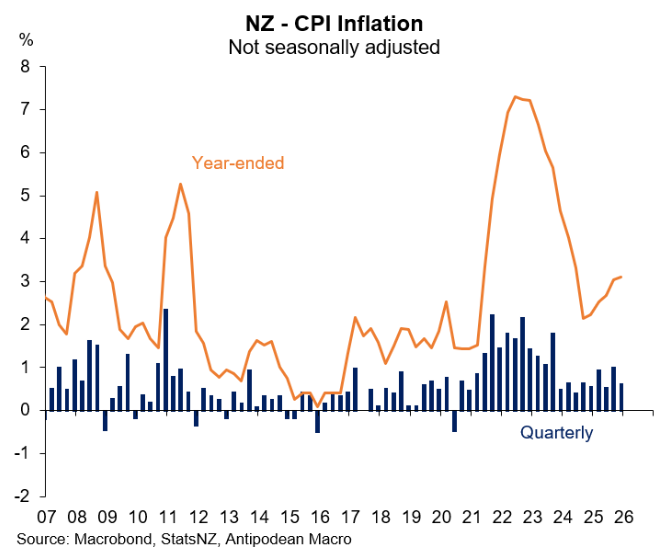

That said, the recent rebound in New Zealand’s inflation rate works against another rate cut.

Unlike in Australia, the Reserve Bank of New Zealand is caught between rising unemployment and rising inflation, making any decision on interest rates less clear-cut.