The Reserve Bank of Australia (RBA) on Tuesday lifted the official cash rate (OCR) by 0.25% to 3.85%, adding around $110 to the monthly cost of servicing the average new mortgage of $700,000.

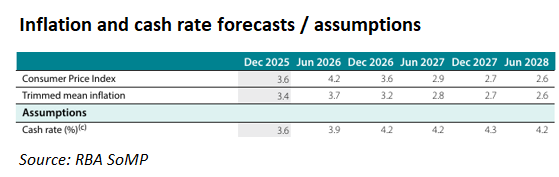

To make matters worse, the forecasts presented in the February Statement of Monetary Policy (SoMP) show that the RBA does not expect trimmed mean inflation to return to the mid-point of its target range until after June 2028:

The RBA also assumed that the OCR would peak at 4.3% in December 2027, implying two more rate hikes.

Two additional rate hikes would also imply a cumulative increase of around $330 in monthly mortgage repayments for the average new mortgage of $700,000.

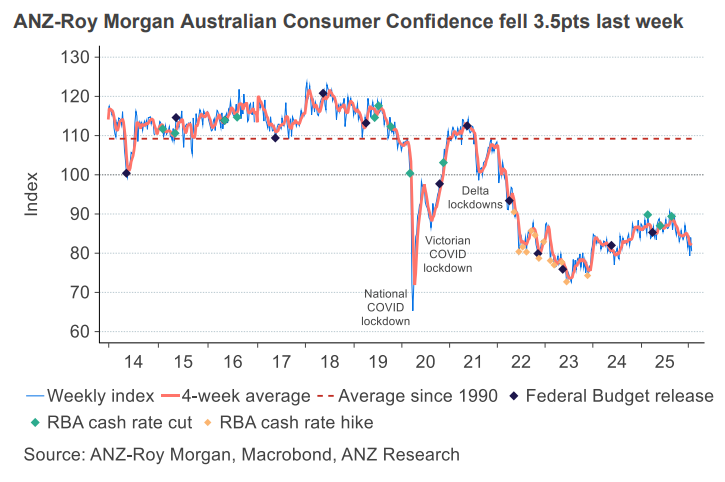

The latest weekly ANZ-Roy Morgan consumer confidence survey was released on Tuesday, which showed that confidence plunged by 3.5pts to 80.5pts last week, following the high inflation print and expectations of imminent interest rate hikes.

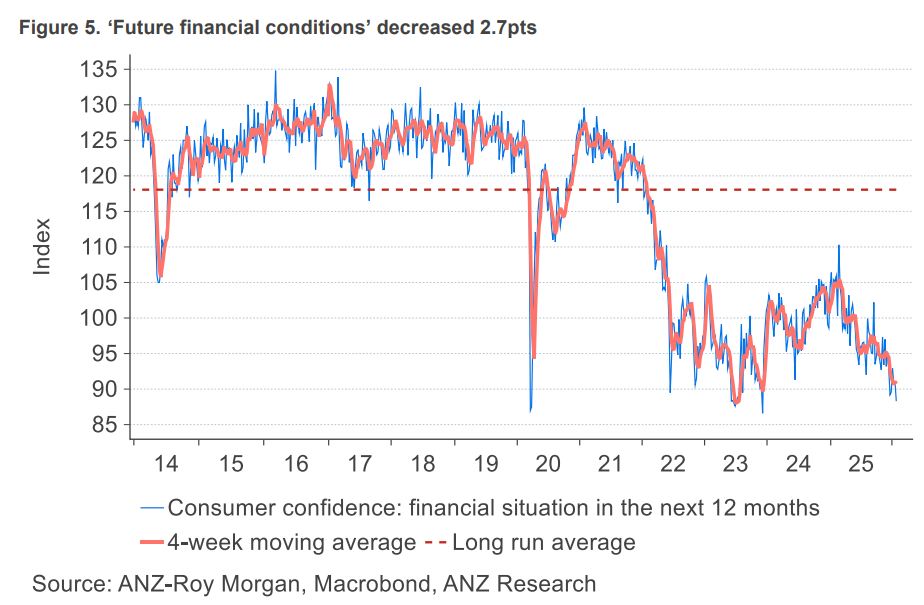

In particular, households are feeling less optimistic about their personal finances, with the ‘future financial conditions’ subindex at its lowest level since late November 2023 (soon after the RBA increased the cash rate to 4.35%).

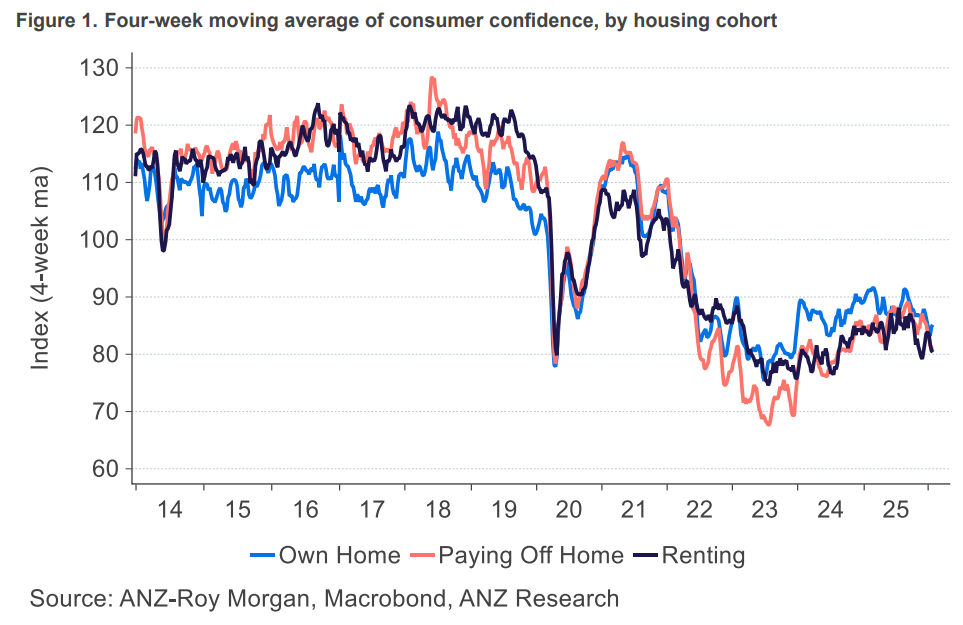

As expected, mortgage holders and renters were the most pessimistic, which makes sense given the prospect of imminent rate hikes (now delivered) and the reacceleration of rents:

With the OCR looking certain to rise again, it will be interesting to see how next week’s consumer confidence survey prints.

Spare a thought for recent first home buyers enticed into the market by the Albanese government’s 5% deposit scheme. They will have borrowed to the hilt and stretched themselves financially just prior to the RBA whacking them with a series of rate hikes.

If house prices turn lower, which is a distinct possibility if the OCR is increased three times, then many could also face the prospect of falling into negative equity, owing the bank more than their home is worth.