Independent economist Tony Alexander argues in a new report that New Zealand’s three-decade, investor-driven house price boom is over.

Average house price growth has structurally slowed, investor participation has fallen, and the psychological “must buy now” pressure that dominated since the mid‑1990s has dissipated.

Chart by Justin Fabo at Antipodean Macro

Alexander believes that housing will still rise over time, but at a more modest pace and with far less investor‑driven heat.

Why urgency has faded:

Alexander notes that the 1990s–2010s saw a unique combination of falling interest rates, migration surges, construction constraints, and strong cultural messaging around property investment.

Those conditions no longer exist.

Alexander lists a long set of structural headwinds reducing investor appetite, namely:

- Financing & tax – Debt‑to‑income (DTI) restrictions limiting investor borrowing.

- Ring‑fencing of rental losses.

- Reduced depreciation allowances.

- Higher operating costs—rising rates, insurance, maintenance, and Healthy Homes compliance.

- Rule changes favouring tenants.

- Market fundamentals, including:

- No repeat of the 1990s migration boom.

- Foreign buyer restrictions (except Australians/Singaporeans).

- No long-term downward trend in interest rates anymore.

- More residential-zoned land and higher construction volumes (especially townhouses).

- Greater awareness of alternative investments (KiwiSaver, managed funds).

- Demographics—Older investors are now selling to fund retirement—often more expensive than expected.

- Sentiment:

- Expectations for long-term capital gains have moderated.

- Fear of future capital gains tax.

- Property investment seminars are attracting fewer people; “rentvesting” has faded.

As a result, investor FOMO (“fear of missing out”) has evaporated. Experienced long-term investors remain, but mass‑market speculative buying has structurally declined.

Investor sentiment has collapsed:

Alexander’s surveys show that a record net 38% of investors plan to sell in the next 12 months:

Net purchasing intentions from investors are at record lows:

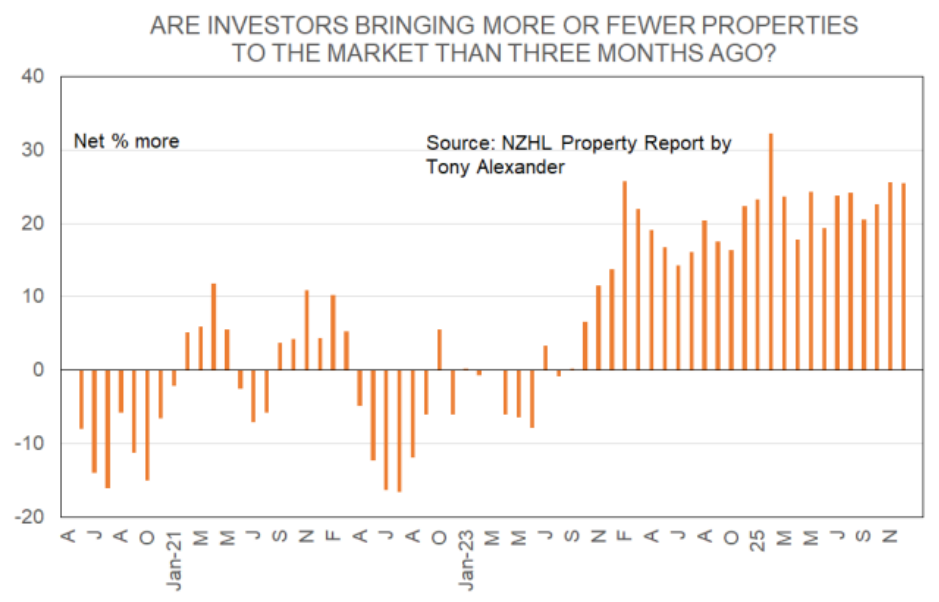

Real estate agents also report more investors looking to sell:

Even with economic recovery and easing debt‑servicing costs in 2024–25, investors still want to reduce their exposure.

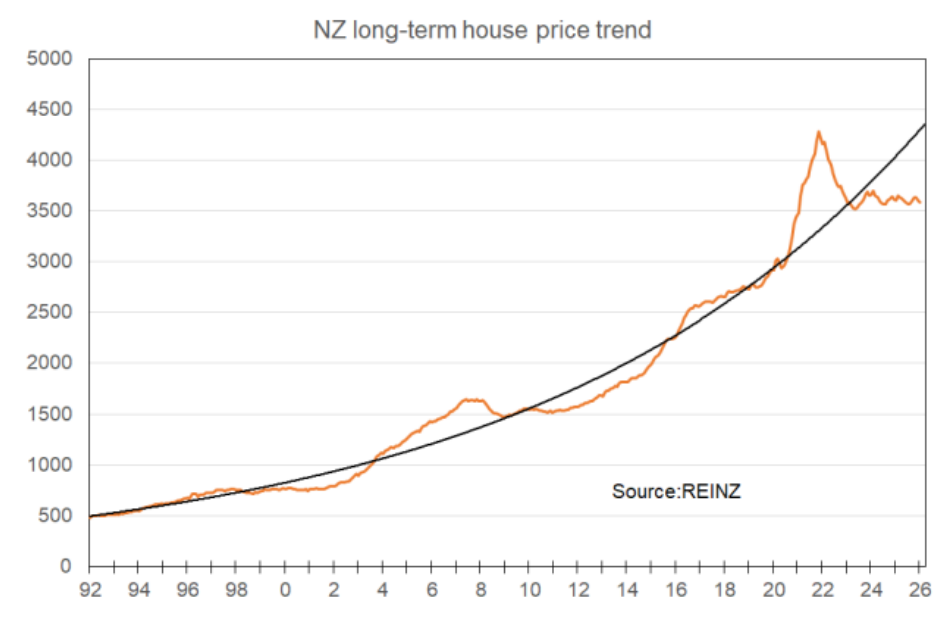

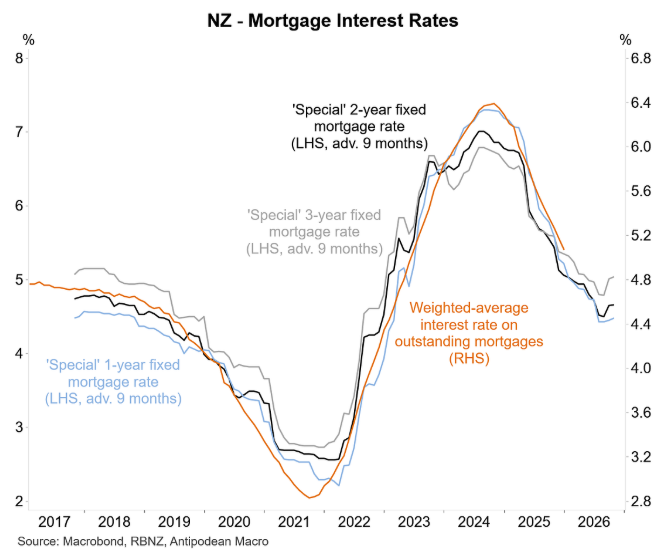

As a result, since mid‑2022, house prices have shown no clear trend—essentially going sideways:

This is despite 3.25% of interest rate cuts from the Reserve Bank, which has dropped mortgage rates to pre-pandemic levels:

Chart by Justin Fabo at Antipodean Macro

“Base animal spirits are no longer a strong driver of swift house price changes, and the long-run will simply sometimes manifest as flat to easing prices and sometimes as a period of catchup”, Alexander argues.

“For young home buyers, this is what they’ve been waiting for”.

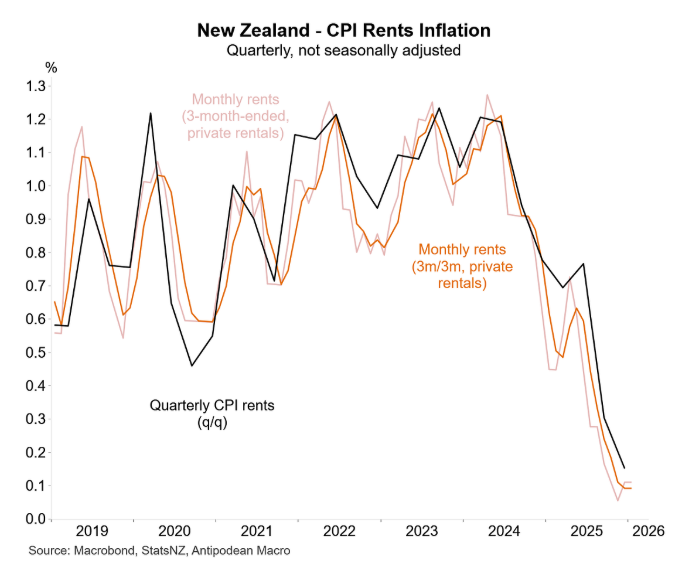

I will add that rents in New Zealand are also becoming rapidly more affordable:

Chart by Justin Fabo at Antipodean Macro

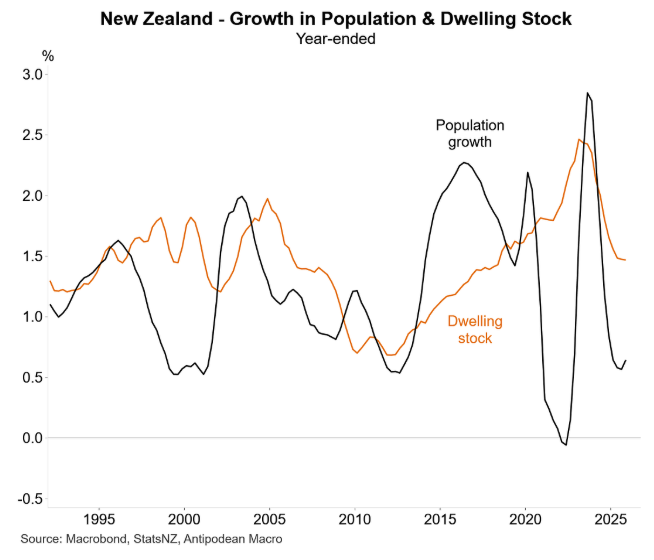

Rental affordability in New Zealand is improving because population growth (via net overseas migration) has slowed significantly and is now tracking well below new dwelling supply:

Chart by Justin Fabo at Antipodean Macro

Australia’s housing market is experiencing the polar opposite, with housing affordability—both to purchase and rent—tracking at its worst level in recorded history and continuing to deteriorate.