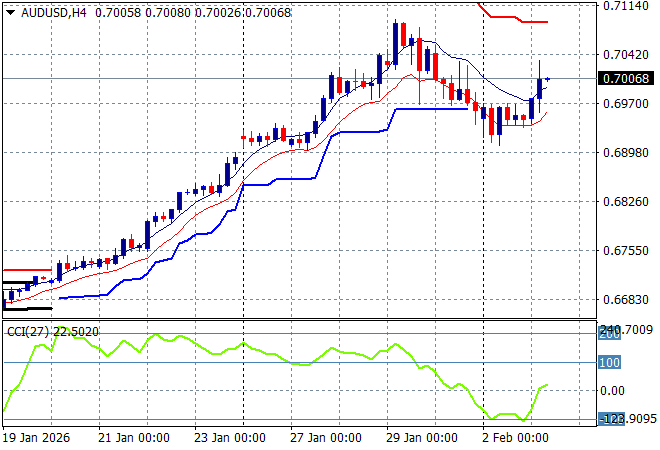

Asian share markets are bouncing back strongly on the back of a solid US manufacturing PMI print overnight and a possible resolution to the latest Epstein distraction as Iran deliberates on shutting down its nuclear capabilities. The USD remains strong against the undollars amid its recent resurgence with Euro heading below the 1.18 handle while the Australian dollar pushed back above the 70 cent level on the long expected RBA rate rise this afternoon.

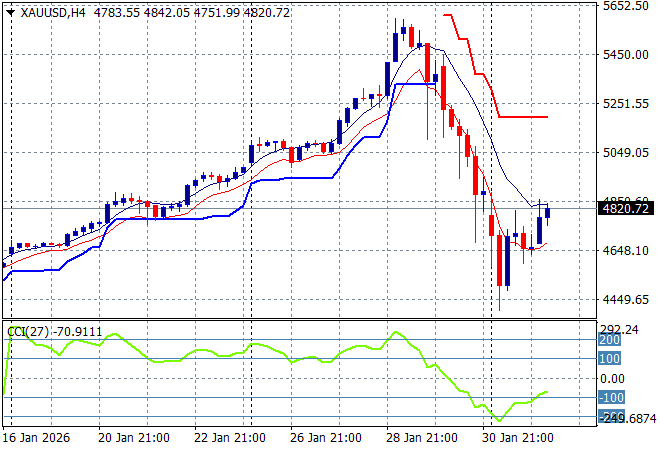

Brent crude has gone nowhere after reversing course as we await if bombs will drop on Iran or not and remains at the $66USD per barrel level while gold has bounced back slightly after falling nearly $1000USD per ounce as it tries to steady here at the $4800 level, with silver also back to the $84USD per ounce level:

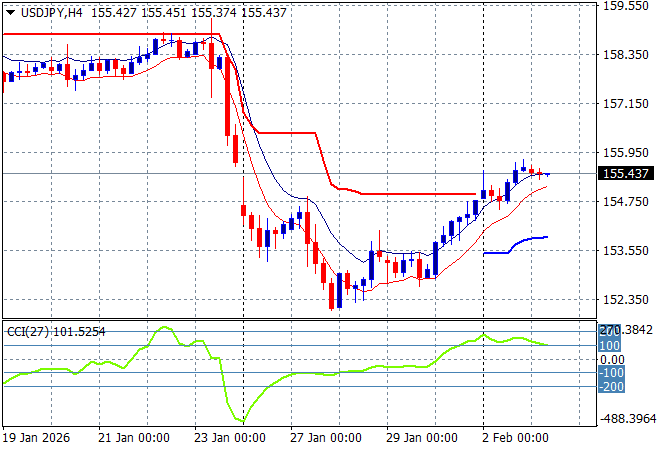

Mainland Chinese share markets are lifting in the afternoon session with the Shanghai Composite up more than 1% to stay above the 4000 point level while the Hang Seng Index is just treading water at the mid 26000 point level. Japanese stock markets are bouncing back the strongest with the Nikkei 225 up more than 3% to zoom through the 54000 point level while Yen is stabilising again as the USDPY pair steadies above the 155 level:

Australian stocks still managed a lift in line with the region with the ASX200 closing nearly 1% higher to 8857 points while the Australian dollar initially lifted on the RBA rate hike but has settled right on the 70 cent level as we now pivot towards the end of week NFP print from the US:

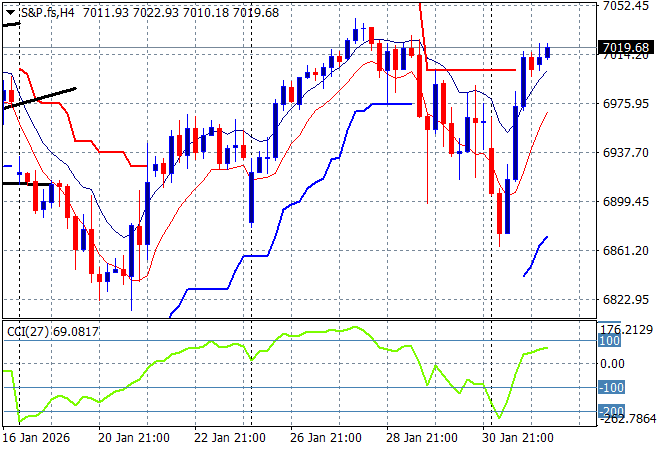

S&P futures are settling in after last night’s rebound with the S&P500 four hourly chart showing a fill after bouncing off support at the 6900 point level to return to the recent highs:

The economic calendar includes some flash inflation data from Europe and then the next PMI print, the US ISM Services for January.