Australia’s 50% capital gains tax (CGT) discount for individuals (introduced in 1999) has come under renewed scrutiny, with a broad coalition calling for reform to ease the housing affordability crisis, bolster the federal budget, and improve intergenerational equity.

The push spans economists, think tanks, former regulators, international bodies, the New South Wales Treasurer, and even some property‑sector voices.

Those calling for reform widely argue that the 50% discount encourages speculative property investment, makes leveraged property more attractive than other asset classes, and pushes first‑home buyers into direct competition with investors.

The CGT discount amplifies investor returns, especially when combined with negative gearing, making housing less affordable for owner‑occupiers.

They argue that the CGT discount is far more generous than intended initially because, when it was introduced in 1999, inflation and interest rates were higher, and home prices grew more slowly.

As a result, the CGT discount disproportionately benefits wealthier households and is eroding the federal budget, as it is one of the fastest‑growing tax expenditures.

Critics also argue that the CGT discount encourages unproductive investment by distorting investment decisions and channelling capital into existing housing stock rather than into productive business investment. It also contributes to Australia’s high household debt.

The most common proposal is to reduce the CGT discount from 50% to 25%.

Most proponents argue that reducing the CGT discount would cool investor demand, reduce speculative buying, level the playing field for first‑home buyers, and reduce price pressures in the lower‑priced segments of the market.

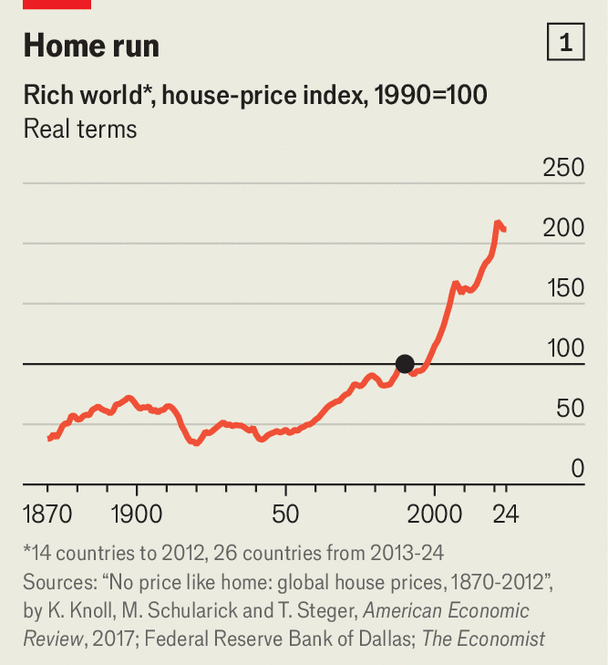

I don’t hold the CGT discount responsible for the absurd rise in Australian house prices this century, given that prices have soared globally:

Chart from The Economist Magazine

This suggests that global deregulation of bank capital rules and mortgage financing played the most significant role. However, the CGT discount would have contributed marginally to Australia’s house price inflation.

Even so, the CGT discount is costly to the federal budget, promotes investor demand, crowds out first-home buyers, worsens inequality, and lowers the country’s homeownership rate.

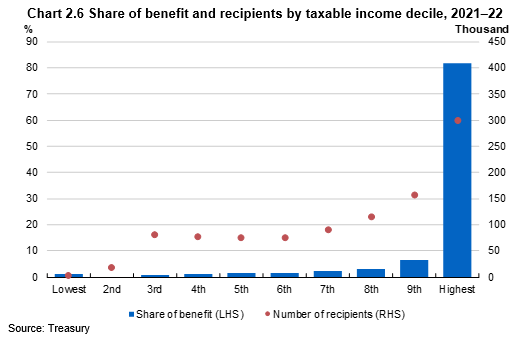

The Australian Treasury’s analysis of the 2021-22 tax year revealed that individuals in the highest income decile received around 82% of the benefit from the CGT discount:

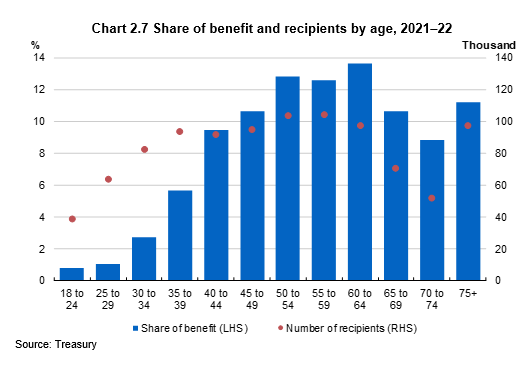

Older Australians aged 50 to 64 received the most significant share of the benefit, followed by those aged 60 to 64 (13.6%):

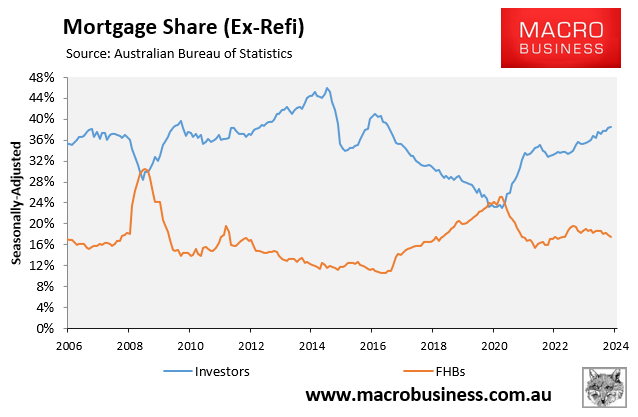

It is also a statistical fact that if policymakers want Australia’s homeownership rate to increase, it needs fewer investors in the market and more first-time buyers:

Therefore, on fiscal sustainability, homeownership, and equity grounds alone, the CGT discount should be made less favourable.

The implementation of the 50% CGT discount in 1999 was a clear policy error. The pre-1999 CGT settings should be restored. These taxed real capital gains (i.e., after adjusting for CPI inflation) at one’s marginal tax rate.

Taxing real gains would also discourage short-term speculation and asset flipping by encouraging investors to hold assets for the long term.