Australia’s 5% deposit scheme has triggered a surge in first‑home buyer activity, but mortgage brokers warn the same policy is now likely to hurt those buyers the most if interest rates rise on Tuesday.

Loan Market data shows a 49% jump in first‑home buyer mortgage applications in October (when the scheme began). Activity slowed in November but rebounded in December to 17% above the pre‑scheme average.

Cotality data showed that homes within the scheme’s price caps rose by 1.2% in October, outpacing the broader market’s 1%.

Investors also piled into the same price bracket, intensifying competition.

Loan Market’s Sam White criticised the 5% deposit scheme for stimulating demand without addressing supply.

“You can have government policies which are generally done with good intentions but generally come back to harm the people they most intend to help”, White told The Australian Financial Review. “This is an example of one”.

Now, financial markets are tipping at least two, and possibly three, 25-bp interest rate hikes by the end of this year.

If these forecasts come to fruition, variable mortgage rates would climb to around 6% by year’s end, adding around $220 per month in repayments on the average-sized new mortgage of $700,000.

Loan Market’s Sam White warns that homes have become more expensive due to the scheme and that buyers who are stretching themselves to enter the market with a 5% deposit will soon be able to borrow less as rates rise.

White estimates that a 0.25% rise in the interest rate reduces borrowing capacity by about 4%.

Sucking first home buyers into the market near the top of the cycle was always a recipe for disaster.

Apart from being inflationary for prices, the policy will leave future first home buyers carrying larger mortgages with thinner equity than they otherwise would have, making them increasingly vulnerable to future house price corrections and negative equity.

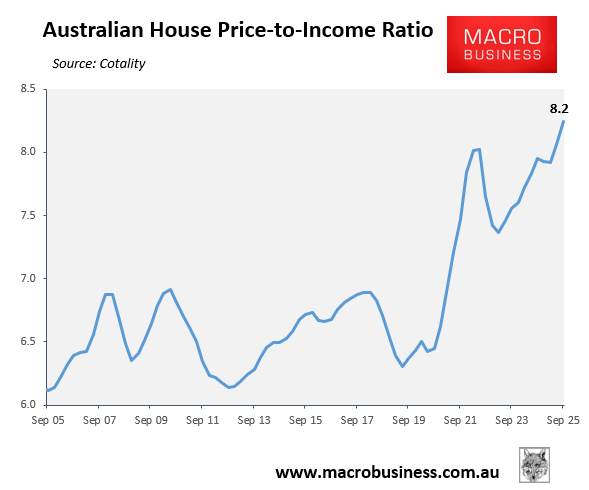

For more than a decade, Australia’s financial regulators cautioned against high loan-to-value ratio (LVR) lending. Nonetheless, the federal government has thrown caution to the wind with its state-sponsored 5% deposit scheme, which effectively institutionalises high LVR lending.

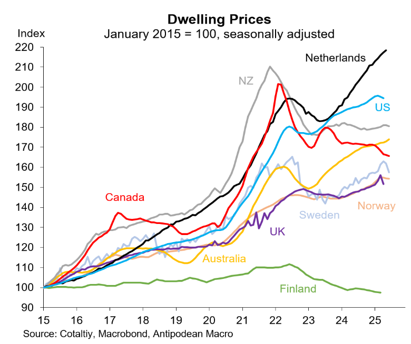

Australia’s most similar economies, New Zealand and Canada, have both seen substantial house price falls of more than 15% from their recent peaks.

Chart by Justin Fabo from Antipodean Macro

If Australia’s property market experiences a similar fall, many recent first home buyers will find themselves in negative equity, with mortgages exceeding the value of their properties.

They would have been suckered into a ‘bubble’ market before a correction.

Australian taxpayers, who have guaranteed 15% of first home buyer mortgages under the scheme, could also face billions of dollars in contingent liabilities.