The Albanese government’s 5% deposit scheme has encouraged many Australian first-home buyers to enter the market.

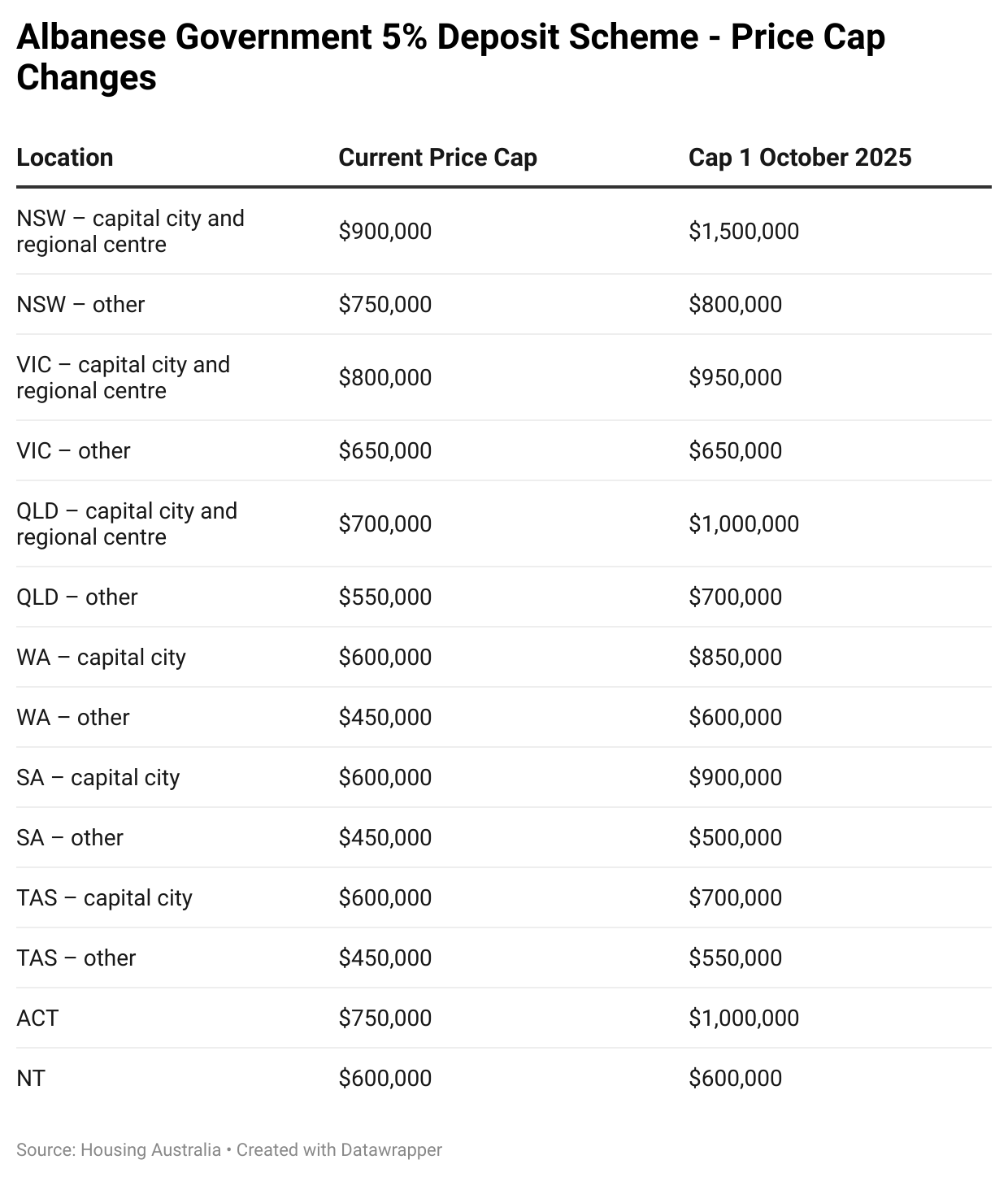

Introduced in October 2025, the First Home Buyer Guarantee program allows eligible buyers to purchase a home with a 5% deposit, with the federal government guaranteeing the remaining 15%.

This means buyers avoid paying Lenders Mortgage Insurance (LMI), which can save buyers $10,000–$30,000 depending on the property, and can enter the market much sooner.

The scheme has no income caps or limits on the number of places. The only constraint is price caps, which were set just above the median dwelling prices of their respective markets.

While there is no official data on the scheme’s numbers, media reports suggest that around 20,000 people have taken advantage of the 5% deposit scheme since its launch on 1 October 2025. However, these figures referred to early uptake estimates, not official Housing Australia data.

Loan Market reported a 49% surge in first home buyer mortgage applications in October (the month the scheme began), with December applications remaining 17% above the pre‑scheme average.

Cotality data also showed that homes within the scheme’s price caps jumped in value after the 5% deposit scheme took effect.

Therefore, the policy has been highly successful in pulling first-home buyers into the market.

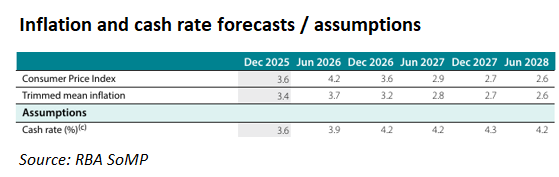

Tuesday’s 25 bps rate hike from the Reserve Bank of Australia (RBA) has placed first-home buyers firmly in the firing line.

The increase will add roughly $110 to the monthly servicing cost for the average new $700,000 mortgage.

The forecasts outlined in the RBA’s Statement of Monetary Policy (SoMP) assumed that the official cash rate would increase to 4.30% by the end of 2027, implying two more rate hikes.

Two additional rate hikes would also imply a cumulative increase of around $330 in monthly mortgage repayments for the average new $700,000 mortgage. The impact would be especially severe for first-home buyers who borrowed to the maximum, entering the market with a 5% deposit.

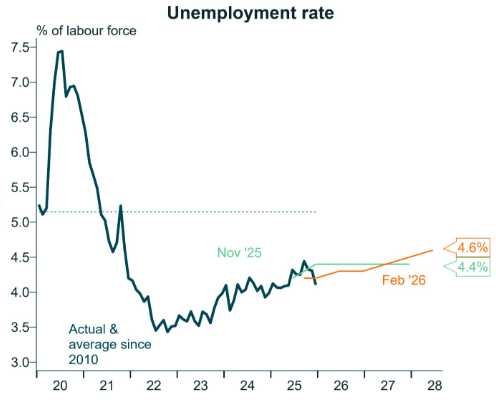

To exacerbate the situation, the Reserve Bank of Australia (RBA) has revised its unemployment forecast from 4.1% to 4.6%.

Chart by Alex Joiner (IFM Investors)

“So effectively, they’re saying that the labour market needs to loosen quite a bit from where it is now if inflation is going to get back to the midpoint of the target band”, said independent economist Gareth Aird on Sky News.

Therefore, first home buyers who have been enticed into the market by the Albanese government’s 5% first home buyers’ scheme are facing the double whammy of sharply rising mortgage rates and a significant rise in unemployment.

It’s important to note that a 25-bp increase in mortgage rates reduces borrowing capacity by 4%. Therefore, the impact will also extend to prospective first-home buyers.

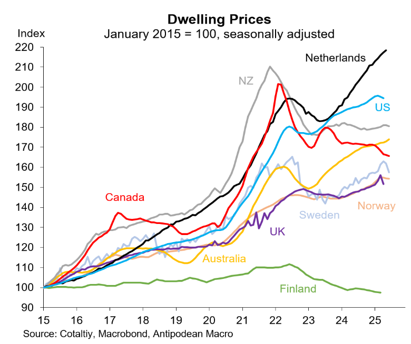

The worst-case scenario entails a significant house price correction, similar to those experienced in New Zealand and Canada, where prices have fallen by around 15% in nominal terms.

Chart by Justin Fabo from Antipodean Macro

A similar magnitude price decline in Australia would likely push many of these recent first-home buyers into negative equity, leaving them carrying mortgages that exceed the value of their homes.

Regrettably, the Albanese government has lured first-home buyers into the market at an unfavourable time. Many could end up becoming collateral damage in the RBA’s fight to contain inflation.