Finally, some positive news on inflation

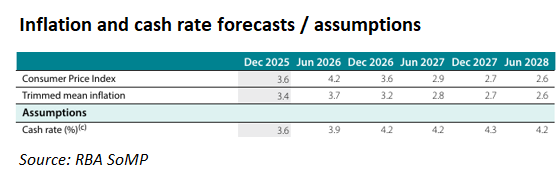

The Reserve Bank of Australia’s (RBA) February Statement of Monetary Policy (SoMP) forecast that trimmed mean inflation would rise in the near term to 3.7% and would remain above the midpoint of the RBA’s 2% to 3% target band until the end of 2028.

The RBA also assumed that the official cash rate would rise two more times by the end of 2027.

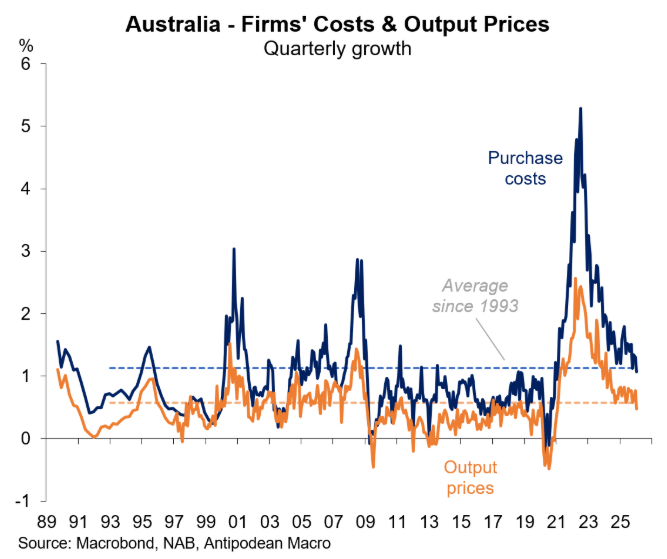

The NAB Monthly Business Survey, released on Tuesday, contained some rare good news on the inflation front.

As illustrated below by Justin Fabo from Antipodean Macro, “Australian firms reported slower input and output price inflation in January”, with “both measures around the averages since 1993 (the inflation targeting period)”.

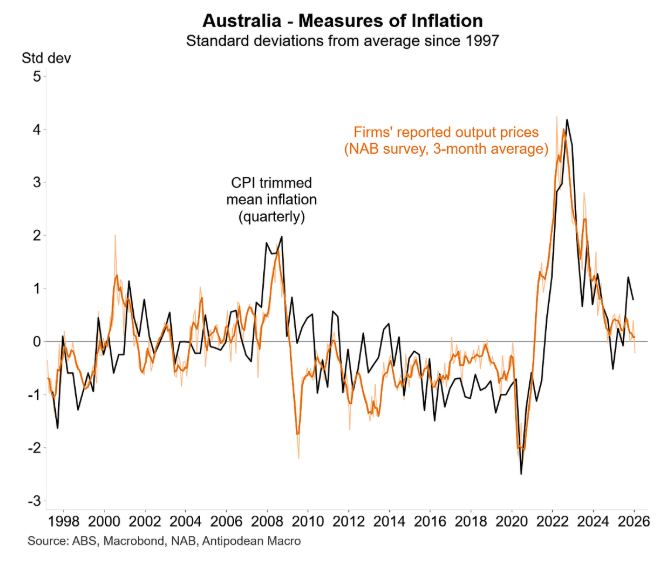

According to Fabo, NAB’s survey of output price inflation points to downside risk for trimmed mean inflation, contrary to the RBA SoMP’s latest forecast:

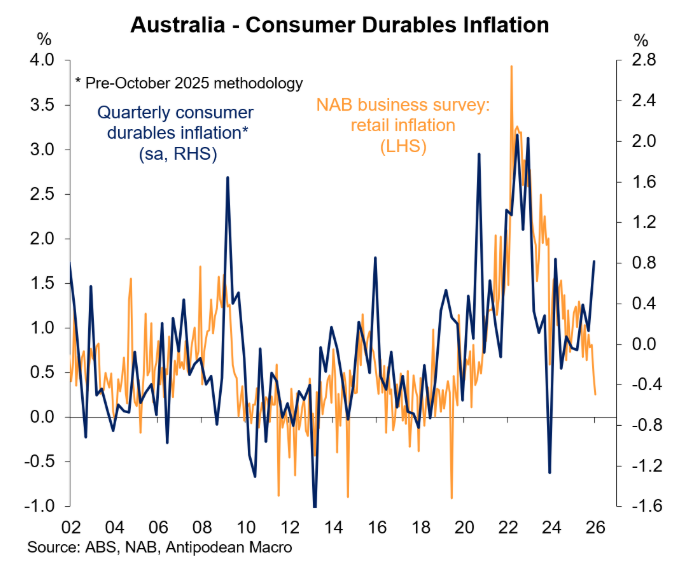

The NAB business survey’s retail price inflation measure also moderated further in January, pointing to slower consumer durables CPI inflation in the period ahead:

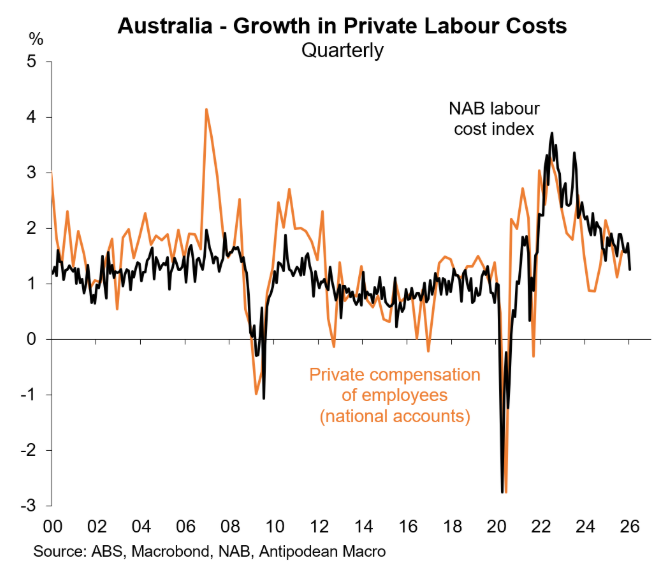

Finally, the following chart from Fabo shows that Australian firms in January reported the weakest labour cost growth since September 2021:

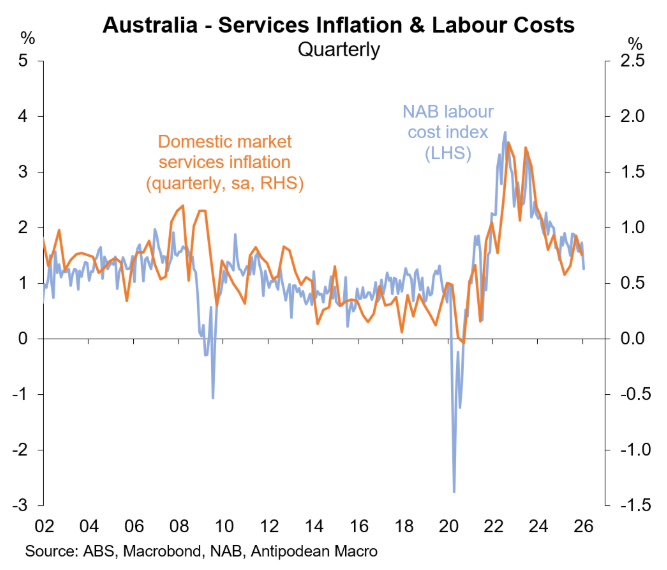

Fabo noted that if sustained, the measure “bodes well for further moderation in domestic market services inflation”, although he cautioned that a monthly move of this size is not unusual:

While it is important to not get too carried away by one survey’s data, the data presented above provides some comfort that inflationary pressures may not be as severe as the latest RBA SoMP implies.

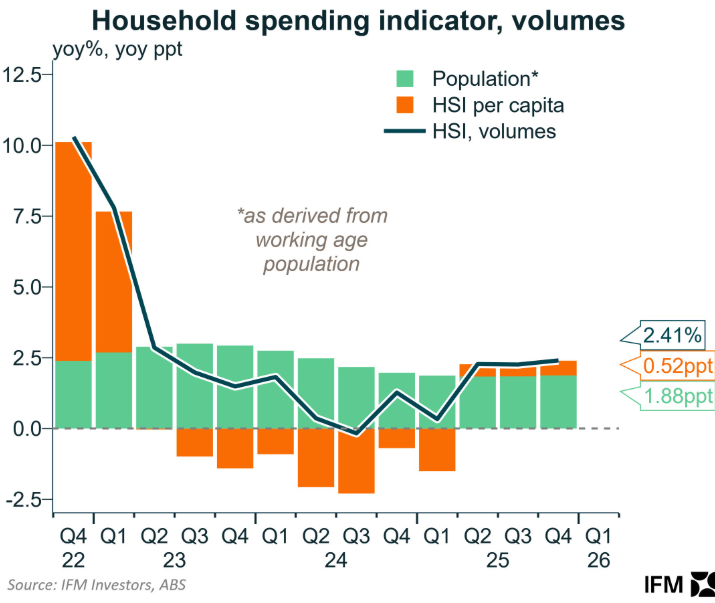

The data also follows Monday’s softer household spending data from the Australian Bureau of Statistics (ABS), which reported a monthly decline of 0.4%, with annual growth moderating to 5.0%.

As IFM chief economist Alex Joiner shows below, in quarterly volume terms, per capita household spending also remained soft:

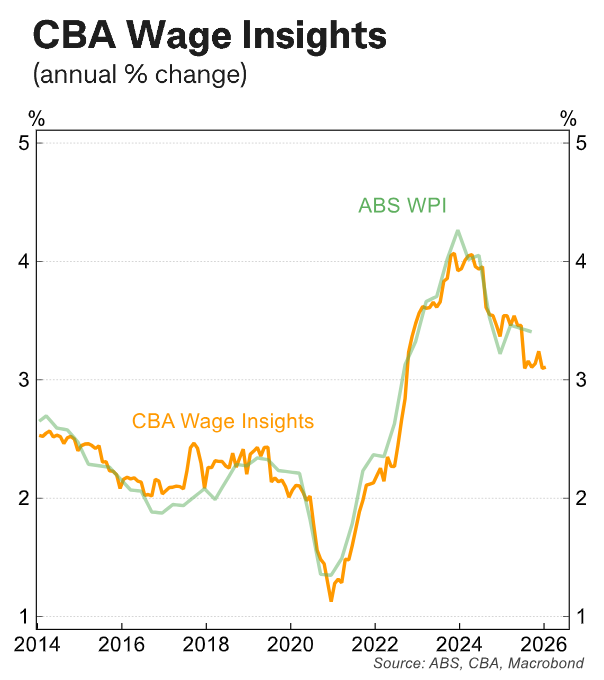

Finally, CBA’s wage insights series for January, which are compiled using CBA internal salary transaction data to create a proxy for wage inflation, have moderated, growing by 0.8% over the quarter and by 3.1% year over year:

The CBA’s wage insight series is tracking below the headline CPI of 3.8% and the trimmed mean inflation of 3.3% reported by the ABS in December. Thus, it suggests that real wages are falling.

It is also tracking below the 3.4% wage growth recorded by the ABS in the September quarter.

The above data, viewed in isolation, argues against back-to-back rate hikes from the RBA.

The RBA will likely wait for additional top-tier data to inform future rate decisions.