Australians have a resolute belief in the property market.

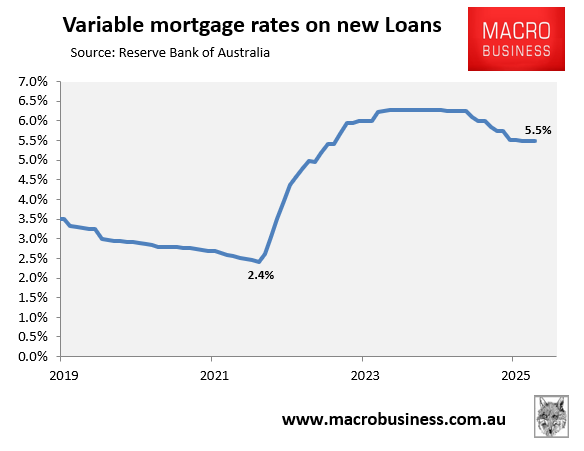

The discount variable mortgage rate has soared from a low of 2.4% in April 2022 to a peak of 6.25% between November 2023 and January 2025 before falling to 5.5% following last year’s three 0.25% rate cuts from the RBA.

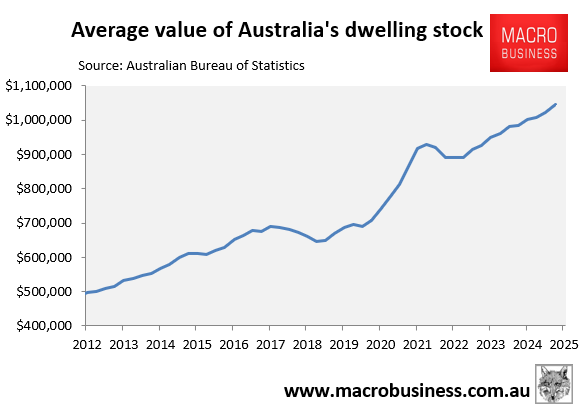

Despite the surge in mortgage rates, the Australian Bureau of Statistics (ABS) valued the average home at a record $1,045,000 as of the September quarter of 2025, up from $668,800 as of the September quarter of 2019.

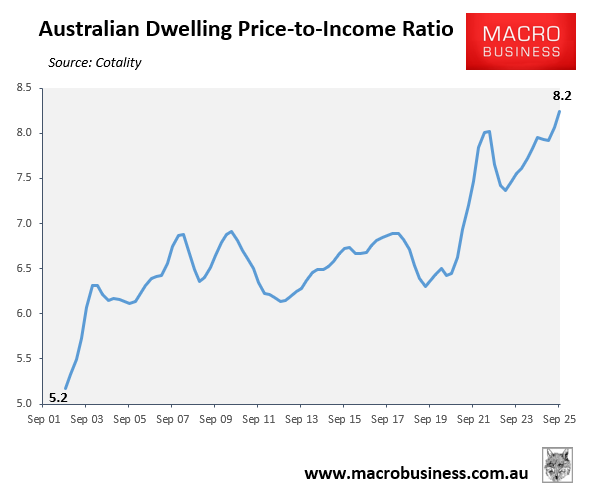

This surge in house prices has lifted the dwelling price-to-income ratio to an all-time high of 8.2 in the September quarter of 2025, according to Cotality.

Last week, the Reserve Bank of Australia (RBA) lifted the official cash rate by 0.25% to 3.85%, with the Statement of Monetary Policy (SoMP) indicating two more rate hikes.

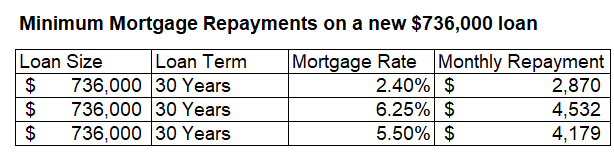

According to Wednesday’s Lending Indicators report from the ABS, the average new mortgage size for owner-occupiers was $736,000 for the December quarter.

The table below uses the average new loan amount of $736,000 to show the effects of this increase in mortgage rates:

The minimum monthly payment was just $2,870 when variable mortgage rates fell to 2.4%.

When the average variable mortgage rate on new mortgages peaked between November 2023 and January 2025 at 6.25%, the minimum monthly repayment on a $736,000 loan was $4,532, a $1,662 or 58% increase.

Following the RBA’s rate reduction last year, mortgage rates dropped to 5.5%, yet the minimum monthly repayment on a $736,000 loan was still $4,179, or 46%, higher than the crisis low.

If the RBA were to raise rates three times, as assumed in its February SoMP and by financial markets, then average mortgage repayments would rise back to their peak level of $4,532 per month.

Amazingly, despite the worst housing affordability on record and the prospect of further interest rate hikes, Australians remain hyper bullish on house prices.

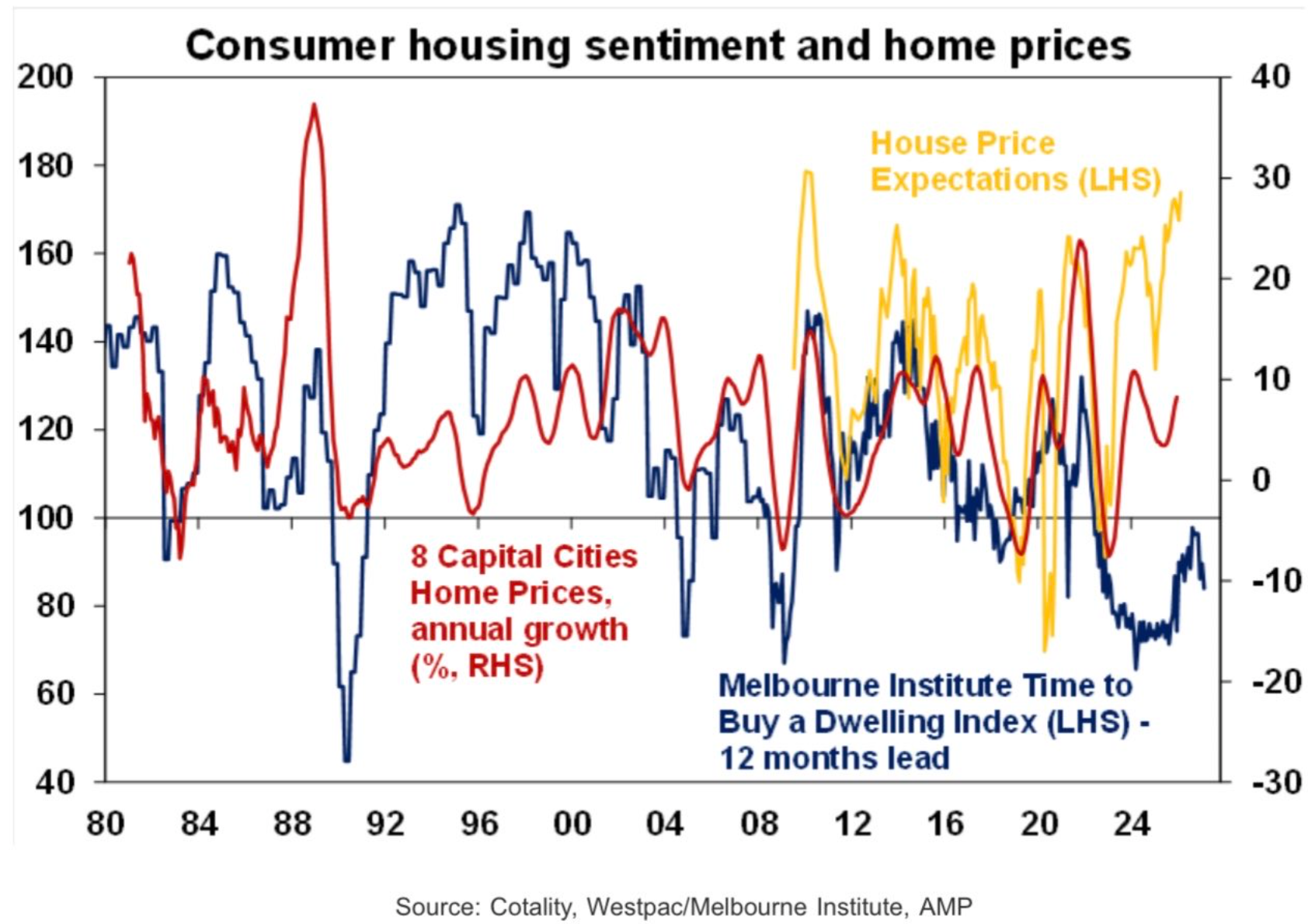

The latest Westpac consumer sentiment index was released on Tuesday and showed that consumer expectations for house prices hit their highest level in 15 years, although fewer people think now is a good time to buy.

Chart by Shane Oliver (AMP)

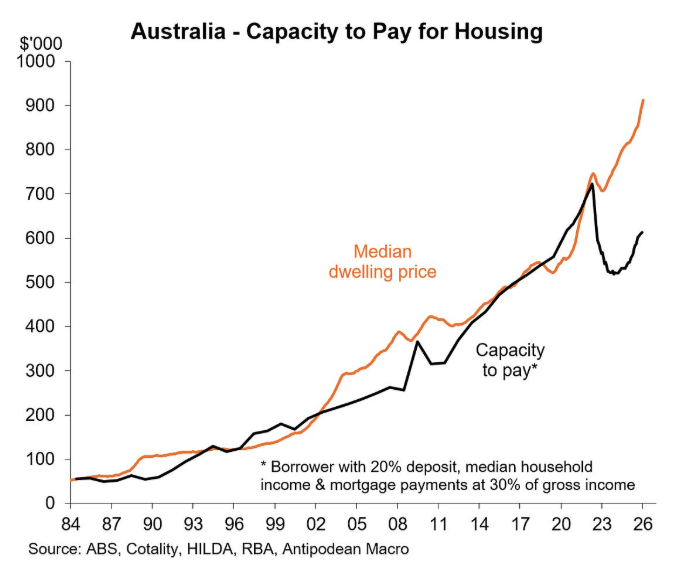

The decline in the ‘Time to Buy a Dwelling Index’ likely reflects the severe decoupling between borrowing capacity and house prices:

Chart by Justin Fabo from Antipodean Macro

In summary, Australians have turned hyper bullish on house prices, although fewer believe that they can afford to buy.

Given the deteriorating housing affordability amid rising prices and interest rates, house price sentiment will eventually turn down.