A few more days of this, and we’ll be getting rate cuts, not hikes.

DXY cratered overnight as a new government shutdown, this time over ICE constraints, looms.

The Australian dollar went berserk with CNY and JPY relief post-election.

Oil and gold did not waste the day.

AI mentals were a little less hysterical.

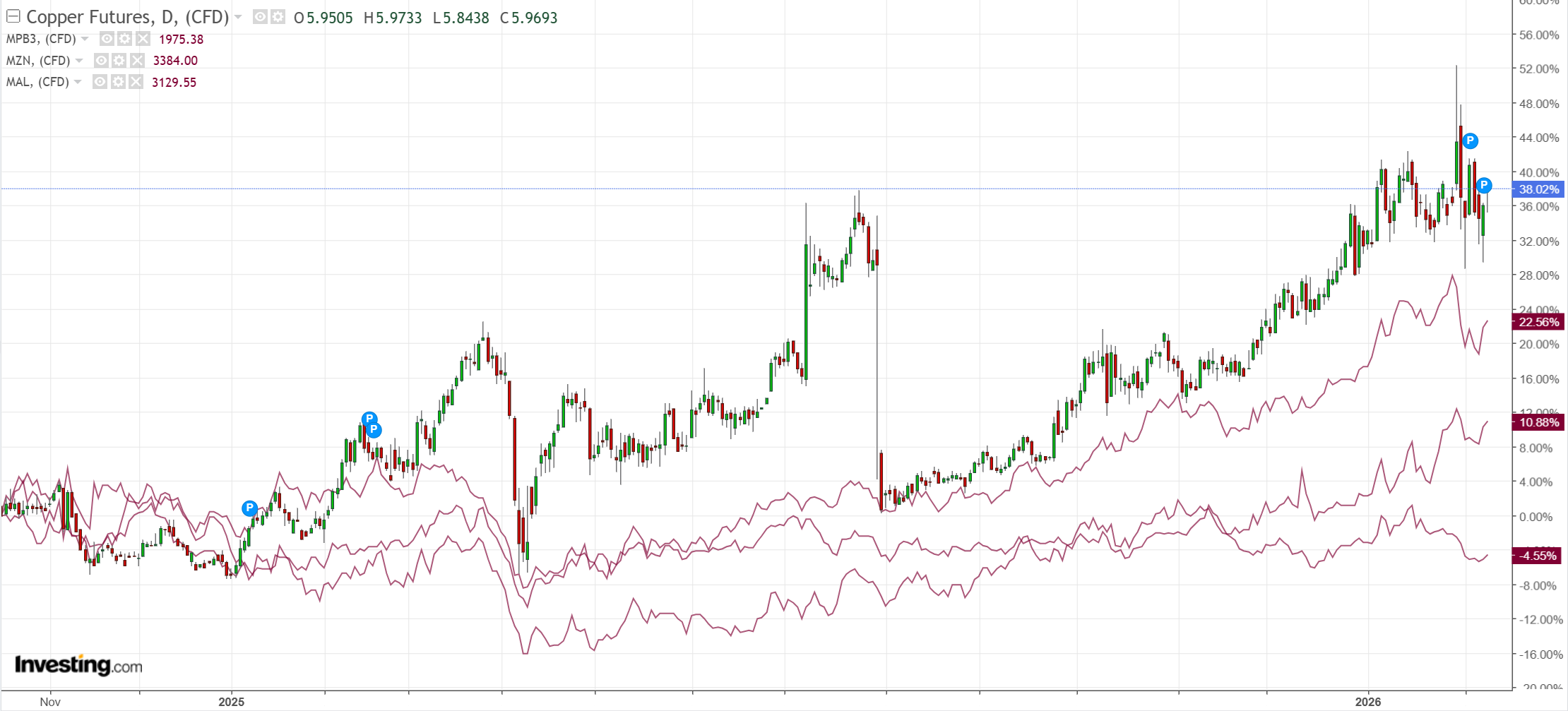

Gapping is the new normal for big miners.

EM stocks are raging on.

Junk is fast asleep.

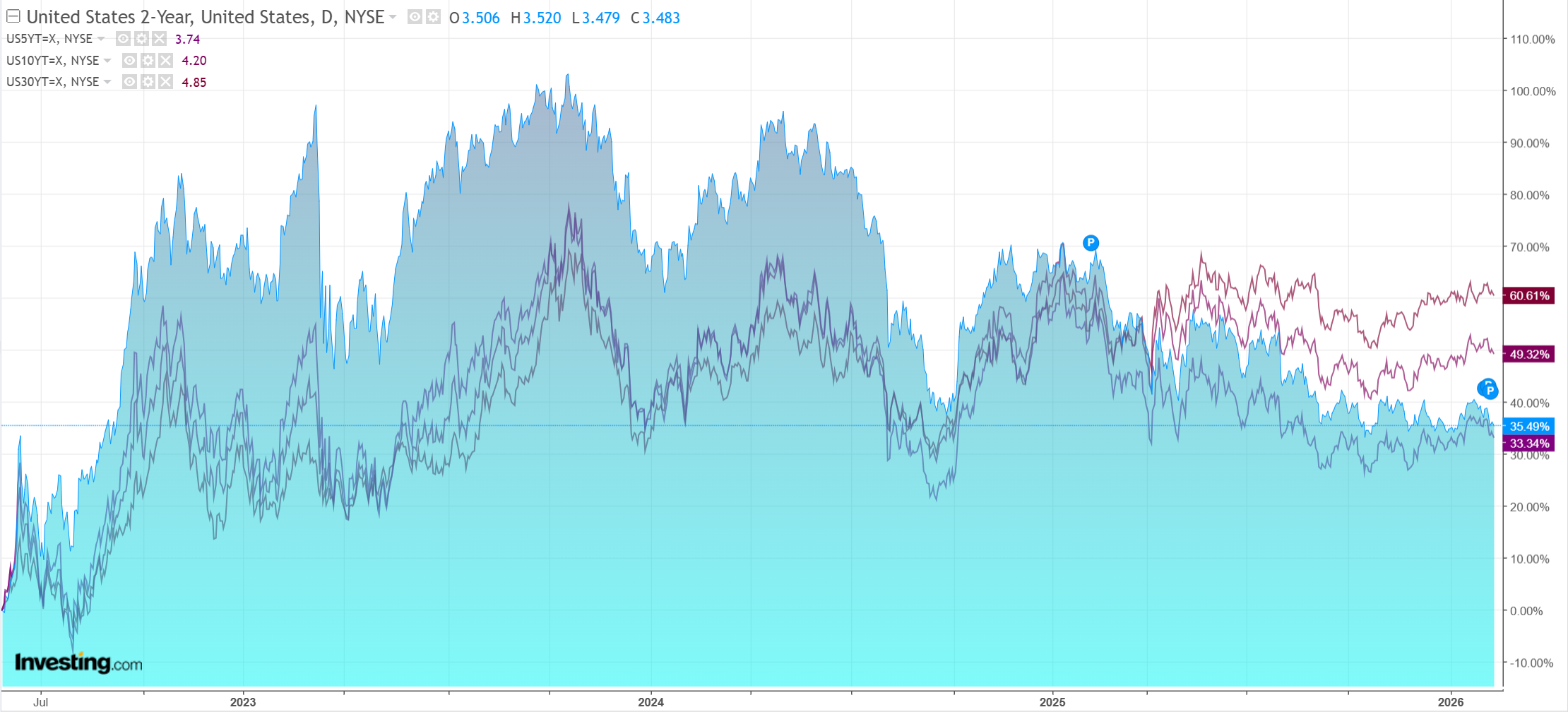

Yields were down as Takaichi made soothing fiscal sounds.

Stocks to the moon!

The Japanese election delivered a strong mandate, but the government immediately offered some salve to the market by imposing conditions on its tax exemptions, which worked for the day to stabilise yields and yen.

There is no crowding in any position for JPY so perhaps a sideways drift is most likely.

We cannot say the same of the EUR/USD which remains extreme.

I cannot see how DXY can continue today’s pace of collapse with this level of overextension.

Any new government shutdown in Washington is quite sensible if it curbs ICE’s fascistic impulses and helps contain inflation.

This is the kind of constraint being placed upon Trump that I expect will eventually stabilise the USD as policy risk declines.

Perhaps it was China’s blather about its banks selling Treasuries that will really hit the DXY, but so what?

They’re not going to. They’ll just hide them in Belgium. There is no other market substantial to put them in.

Anyway, my call that the end of the Trump trades in forex is not far is obviously early today, and I still expect AUD to rise to 0.75 before it is over.

That will kill local inflation. We’re already at a 10% rise, and that’s as much as a 1% fall in the CPI.

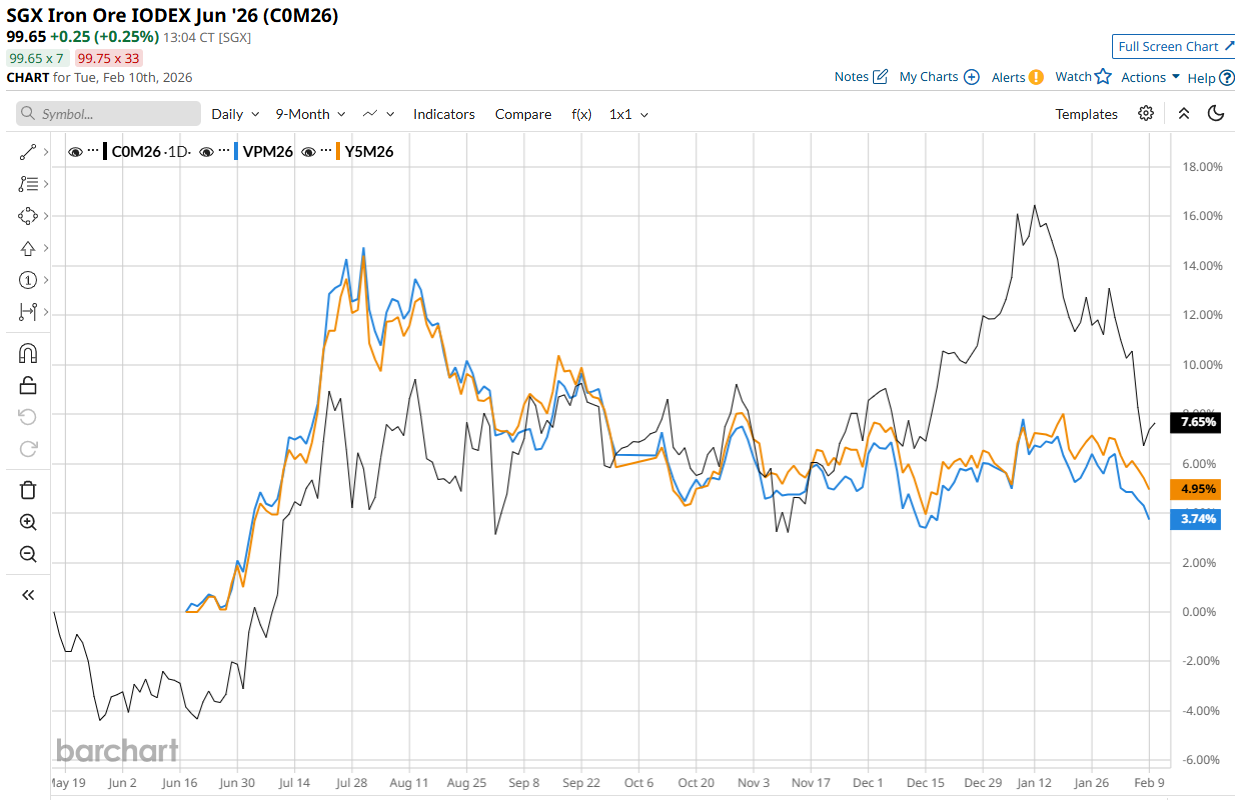

Turning to iron ore, there was a little price relief from Cyclone Mitchell, but everybody is back up and running.

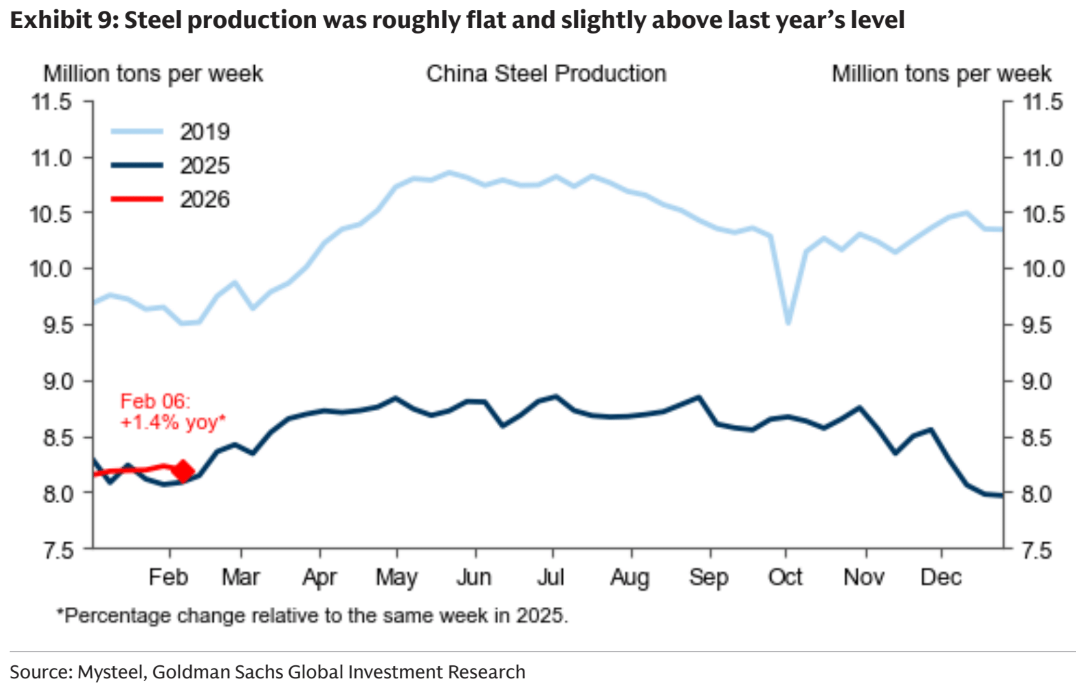

The ferrous jaws have largely closed, but steel is now falling.

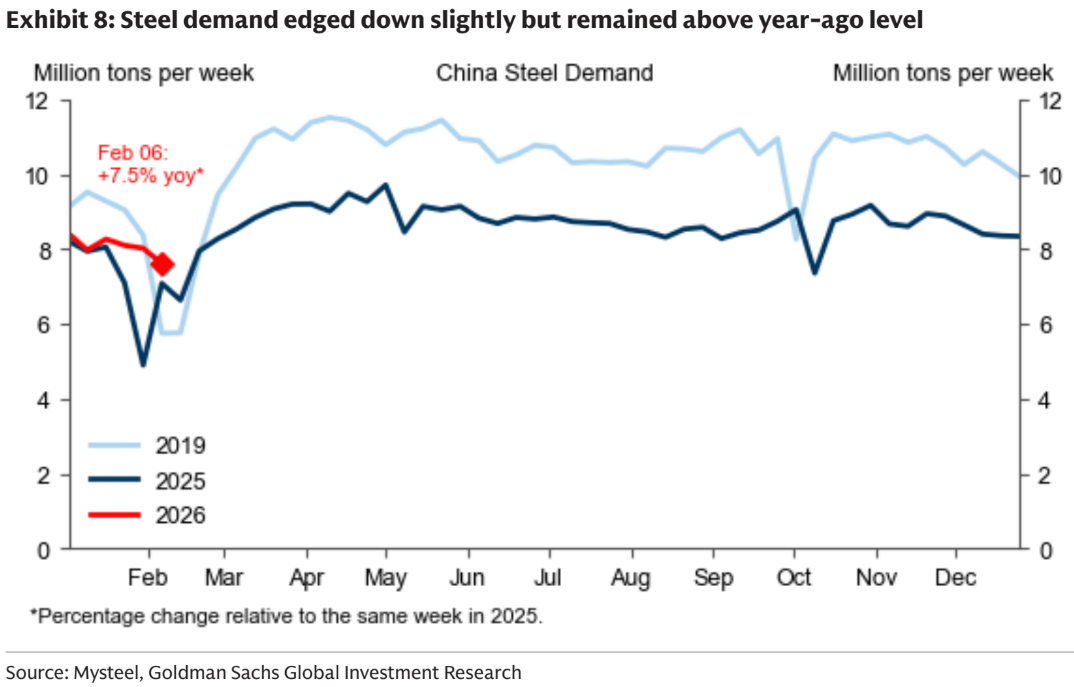

MySteel indexes this week are indecisive, with both steel demand and supply distorted by the late CNY.

Hot metal output is rumored to be disappointing, but we won’t know for sure until we emerge from the holiday.

If it is decent, we’ll get a price bounce. If not, we will fall straight through June without passing go.