Should the RBA hike interest rates into an energy shock?

Economists are debating the merits of interest rate hikes.

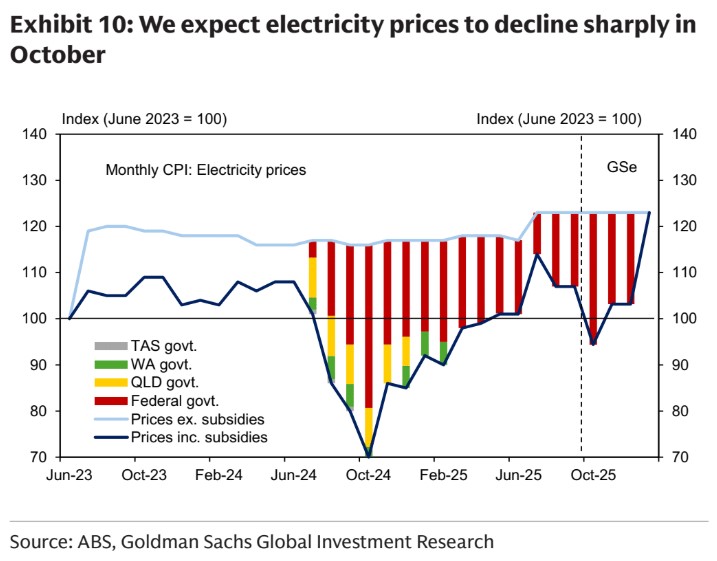

Expectations of a higher quarterly inflation rate have driven a near 60% chance of an interest rate hike at the Reserve Bank’s meeting next week, keeping pressure on the Albanese government to address the rising cost of living from, most notably, higher electricity prices.

…The results will show the last of the soft electricity prices that had been artificially suppressed by federal government rebates, before they rolled off at the end of 2025.

…Without the rebates, electricity prices are expected to contribute to higher inflation, forcing the Albanese government to demonstrate that its ambitious renewable energy and decarbonisation targets are not costing families through higher cost-of-living pressure.

The energy transition has not caused the recent price spikes. They have been caused by the East Coast gas cartel and its war profiteering during the Ukraine War energy shock.

The government’s stupid response to the shock was to offer temporary energy subsidies rather than permanent LNG export levies, which would have prevented price rises entirely.

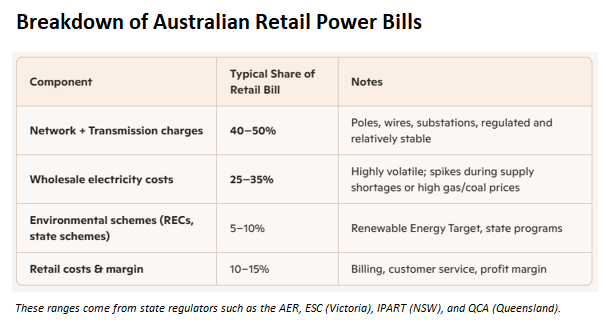

This does not mean the energy transition is free. It is not. Wholesale power is 25% to 35% of the retail bill. Network costs are about 40% to 50% and would have crept up. Then there are environmental schemes like renewable energy certificates, which have added between 5% and 10% to power bills.

However, the shock is all down to the gas cartel. The question is, should the RBA “make room” for such a grotesque economic entity?

CBA says yes.

Commonwealth Bank of Australia economist Trent Saunders said the inflation pressure will be too much for the RBA to hold the official interest rate at 3.6%. It will have to hike to 3.85%.

“We expect the CPI print will confirm that underlying inflation pressures are strong, with this seeing the RBA hike the cash rate at its February meeting,” Mr Saunders said.

He expects housing costs, especially rents, will show up as a significant driver of Wednesday’s inflation reading, while electricity prices were likely to cause bigger headaches in the next set of quarterly inflation results.

WBC makes much more sense to me.

Westpac chief economist Luci Ellis, a former RBA official, expects only a slight rise above the central bank’s forecast. However, she suggested that government-controlled prices have been a significant part of the inflation figures.

“Policy-driven price changes, covering electricity, tobacco, childcare, water and sewerage, education, property rates and charges, postal services, and motor vehicle‑related services have been central to recent inflation,” Dr Ellis said.

“These areas mostly lie outside the influence of monetary policy.”

I see no reason, theoretical or practical, why Australian households should be punished with rate hikes to pay for their energy bill hikes.

This is absurd central banking. A cost-push inflation burst like this passes after it is fully absorbed. It is not like a wage breakout that repeats year after year.

The central bank should ignore cost-push inflation while pressuring fiscal authorities to address it.

This is especially so when the shock is so eminently preventable with the stroke of the treasurer’s pen.

He just doesn’t seem to have one, or a spine.