Yesterday’s monthly inflation number was softer than expected, easing fears of a February rate hike.

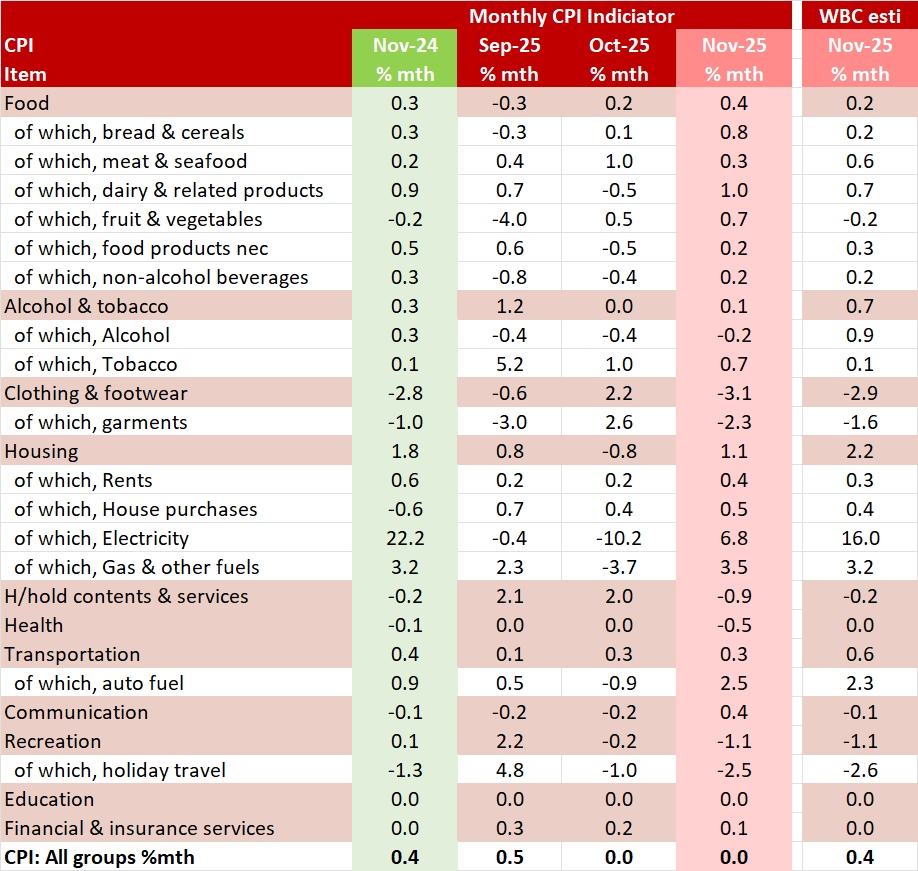

Summing up, headline CPI was lower than Westpac had anticipated, coming in at 0.0% for the month as opposed to its projection of 0.4%.

This puts Westpac’s current December quarter nearcast of 0.6%qtr for the Headline CPI and 0.8%qtr for the Trimmed Mean at risk of being too high.

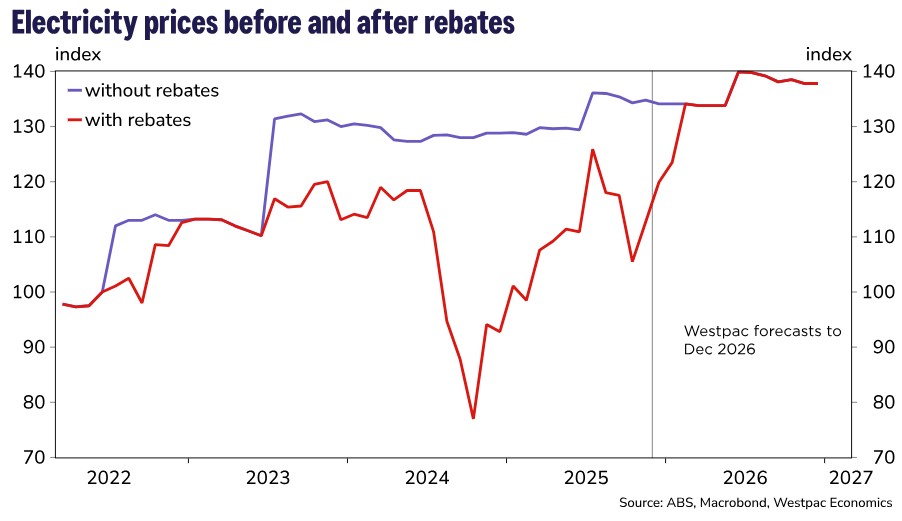

The breakdown of numbers shows the energy shock remains very prominent.

There is more of that ahead, thanks to Canberra’s energy management.

However, this is cost-push inflation, and a central bank will typically look through it.

Westpac continues to expect inflation to ease and for no hikes in 2026.

Adding to this, ANZ notes that it anticipates that the RBA will maintain the cash rate at 3.60% at its Monetary Policy Board meeting next month and across its forecast horizon.

It believes that the Q4 trimmed mean inflation result will be sufficiently near to the November Statement on Monetary Policy’s prediction for interest rates to stay constant.

Moreover, that the Board may also be able to decide that the policy is rather restrictive at 3.60% in light of recent indications of cooling in the housing market, such as auction clearance rates and prices.

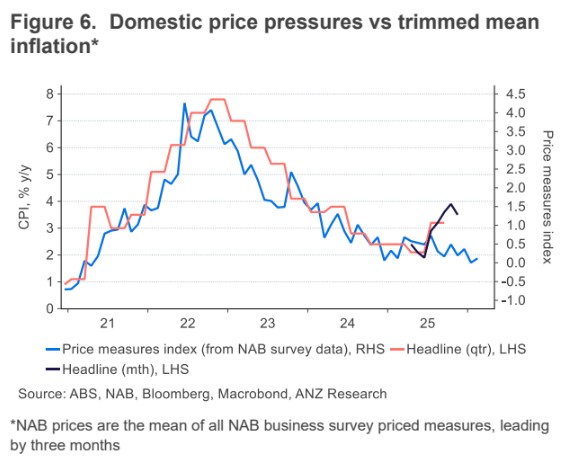

It is clear that the inflation rebound is idiosyncratic, not broad-based.

Goldman is more jumpy. It notes that market services inflation (not including volatile items) eased 31 basis points to 2.9% year over year, but housing inflation was stronger than anticipated, while prices for a number of durable goods and domestic vacation travel decreased.

Overall, it says, the data from yesterday indicates an uncomfortable level of underlying inflation.

Given the contents of the monthly CPI release, GS maintain an existing headline projection at 0.63%qoq but has increased its tracking estimate for the 4Q2025 trimmed mean to 0.91%qoq (previously: 0.83%qoq).

It says the February decision is quite tight because this forecast is higher than the RBA’s November forecast of 0.8%qoq.

In my opinion, there won’t be any rate hikes in 2026, given that the energy shock will trigger a one-time price increase that washes through by H2, housing is already in decline, consumption will soon follow, and wage growth will continue to decelerate due to mass immigration.