While December itself was weak, the 12 months ending on 31 December were a good year for international stocks. Being overweight internationally, with a healthy exposure to AI, our portfolios all outperformed their benchmarks. Our international fund finished up 20%, and our Australian fund finished up around 9%. Our tactical growth finished up around 11%. All of our funds look attractive relative to their benchmarks, especially as they were all significantly less volatile than the market.

January has seen some of the heat come out of prices, but the key story leading into reporting season is the strength of company earnings underpinning the market. While there are economic problems in many countries, they are mostly affecting consumers and workers – companies are doing pretty well.

Company Earnings vs Politics

There is a pretty big divergence in the state of politics in countries across the globe and company earnings.

There is clearly economic pain, or at least fear, among consumers and workers. Combined with fear of AI and immigration, historical political relationships are undergoing a turbulent reshaping.

In contrast, company earnings are looking really strong. Maybe a reasonable amount of that is causation rather than correlation? Higher company profits usually mean greater economic inequality. Greater economic inequality usually means more political turbulence.

As investors, we need to do three things:

- Separate political concerns from economic concerns.

- Separate economic concerns for households, governments or small businesses from economic concerns for listed companies

- Recognise when a system is fragile and could reach a breaking point

My take is that we are in a weakish growth phase, but company profits are booming. Politics is fraught, and needs to be watched closely.

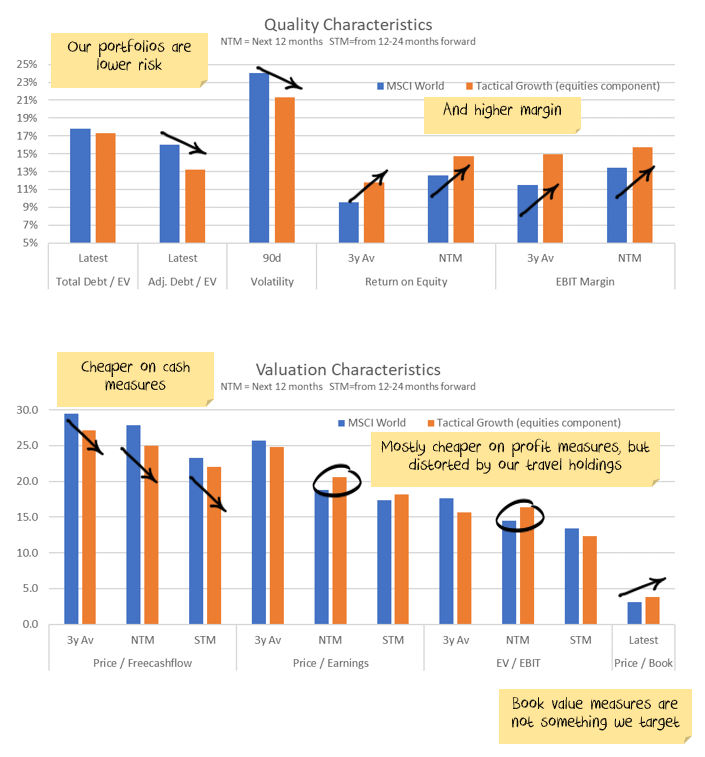

Q1 earnings are about to start, and look good

Stocks are expensive on most simple metrics.

The question is whether earnings can grow fast enough to justify those prices. For now, the answer is yes. Forward earnings—the best simple proxy we have—is rising at a rising rate:

What could break the earnings story?

- A policy shock that endures. Tariffs that lift input costs and depress demand at the same time. A tax change that hits cash flows. A regulatory swing that curtails investment in a key growth area.

- A demand shock. If the consumer slows sharply and services spending stalls, revenue growth will slip. That would expose margins that look fat today.

- A financing squeeze. If high‑yield spreads gap and banks tighten lending standards more than they already have, small and mid‑sized firms will cut capex and headcount.

- A supply constraint that proves binding. AI is power‑hungry. Data center build‑outs require transformers, switchgear, and grid upgrades. If the bottlenecks worsen, revenue timing slips.

Politics are going through a transformation

Tail risks abound

- A durable tariff regime that raises costs across supply chains and provokes credible retaliation from Europe. A U.S.–EU trade war would not be a sideshow. It would hit autos, machinery, chemicals, and services. It would dent confidence and capex.

- A meaningful fracture in NATO. Even a serious threat to withdraw support would force Europe to rethink defense burdens, debt issuance, and industrial policy. That would ripple through currencies and rates.

- Domestic institutional stress. If rulemaking is sidelined in favor of unilateral edicts, if independent agencies are bent to political ends, then policy volatility rises. Businesses delay decisions. Multiples compress.

Balance that against two important constraints. First, markets themselves act as a brake. Trump is sensitive to stock market reactions. When equities swoon and credit spreads widen, rhetoric often softens. Second, the machinery of policy is slow. Most big changes have to pass through comment periods, court challenges, and congressional action. That lag creates time to reassess, reposition, and hedge.

Key things to watch

- Focus on forward 12‑month earnings and the slope of revisions. Up is good. Down is a warning.

- Look for breadth. Widespread upgrades beat a narrow AI‑plus‑a‑few story. If breadth improves, the market’s foundation strengthens.

- Examine margins and unit labor costs sector by sector. Resilient margins in the face of cost pressures suggest real pricing power. Cracking margins say the opposite.

- Track capex plans, especially in AI infrastructure and adjacent industries. Delays signal demand fading or supply constraints biting.

- Separate rhetoric from rulemaking. Executive orders, formal notices, draft rules, and legislation matter more than press conferences.

- Watch hard policy markers: tariff schedules, quota rules, procurement guidance, and NATO commitments. These change incentives and cash flows.

- Study market reactions across assets. If equities drop but credit spreads and rates shrug, the move is probably noise. If credit spreads gap, the risk is real.

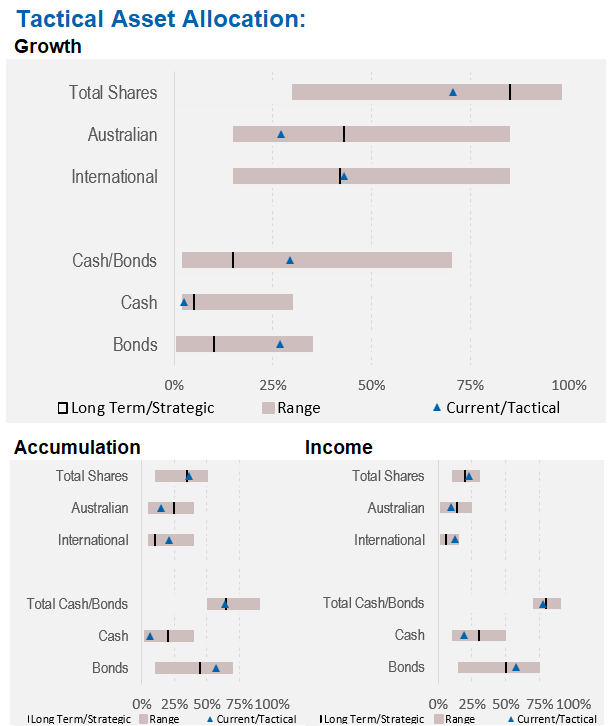

Asset allocation

We are a little underweight in shares overall, significantly underweight in Australian shares. We are market-weight bonds, with a little foreign cash:

Performance Detail

Core International Performance

The year ended on a downward beat as US stocks pulled back, while Europe had a good month. Currency was an overall detractor as $A strengthened.

Core Australia Performance

In December, the financial stocks recovered as the growth stocks lagged.

Damien Klassen is Chief Investment Officer at the Macrobusiness Fund, which is powered by Nucleus Wealth.

Follow @DamienKlassen on X(Twitter) or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an Authorised Representative of Nucleus Advice Pty Limited, Australian Financial Services Licensee 515796. And Nucleus Wealth is a Corporate Authorised Representative of Nucleus Advice Pty Ltd.