Westpac is unmoved by the good jobs report.

The December LFS clearly landed on the firmer side and the wash-up for the last few months suggests that the ‘gradual softening’ narrative, which characterised the bulk of last year, paused or completely halted. This leaves us with the question of whether further gradual softening is still on the cards in 2026. As we noted last year, now that jobs growth in the ‘care economy’ has largely normalised and there are early signs of a pick-up in market sector employment, we could be near or at the trough for jobs growth.

Looking forward, the trend for labour force participation will be key. Our baseline forecast is for growth in the labour force to outpace employment, leading to an incremental build-up of slack over this year. It may well be that this comes along in ‘fits and starts’, with the starting point for 2026 looking firmer than we had initially anticipated. The next couple of months of data will be crucial in confirming whether this is the case.

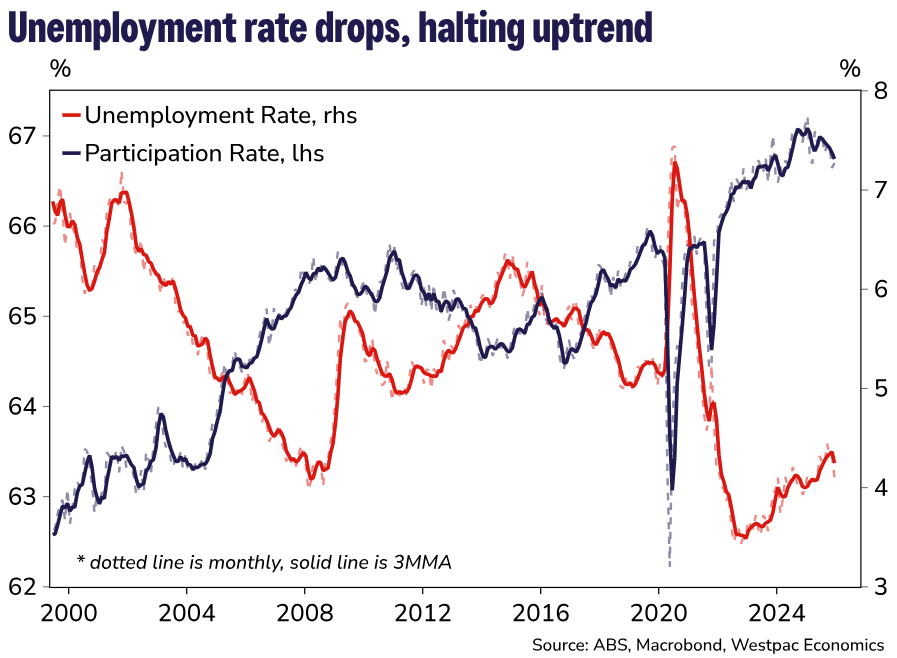

In short, recent falls in participation, rather than job creation, are more responsible for the decline in the unemployment rate.

Mass immigration should reverse this.

The more hawkish ANZ agrees.

The unemployment rate unexpectedly dropped to 4.1% in December, versus our and market expectations that it would remain at 4.3%. Employment rose by a strong 65.2k, well above expectations with hours worked up 0.4% m/m.

While there appears to be some noise in the December labour force survey (namely the increase in employment of 15–24-year-olds, a part of the data that has been volatile recently), the decline in the unemployment rate does make a February rate hike more likely at the margin.

Should the Q4 trimmed mean print at 0.8% q/q (our forecast), we still expect the RBA to hold. On a 0.9% q/q outcome a rate hike would now appear a little more likely than not (pending the detail of the CPI).

Goldman is similar.

Overall, today’s data suggests that labour market conditions were slightly more resilient over 4Q2025 than the RBA’s November forecasts had assumed.

That said, these data are volatile, and today’s update is at odds with the softening across several leading indicators of the labour market, including job ads and unemployment expectations.

Looking ahead, we continue to expect the RBA to remain on hold at 3.6% but stress that it is a close call and note that a hike in February remains a material risk.

The consensus is that a 0.8% quarterly trimmed mean will satisfy the RBA. 0.9% may trigger a hike.

To my mind, such minor differences are foolish. Wages are still softening.

And there is likely to be some lift in productivity this year as the market sector climbs off the canvas.

That should take care of the unit labour costs worrying the RBA, even though they are not a big deal.

Much of the inflation is still cost-push and will ebb in H2 anyway.

Hiking would be a mistake.