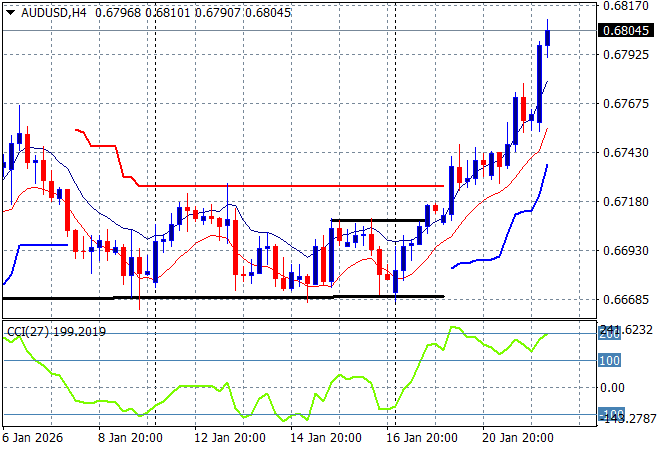

Asian share markets are generally higher across the region with only Chinese shares taking a breather as markets react to YATT (Yet Another Taco Trade) from Trump as all is forgiven over Greenland at Davos. Of course the “America-off” strategy is still in play as a broader trend with more news of Treasuries being sold off while the USD remains under pressure against almost all major undollars. The Australian dollar continues to lift off support and has breached the 68 cent level on a much better than expected unemployment print.

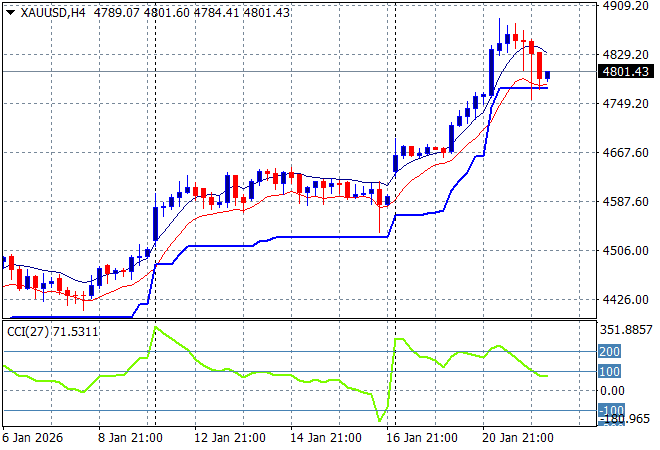

Brent crude is easing higher to just above the $65USD per barrel level while gold has stalled out just above the $4800USD per ounce level with the Minsky Metal the star of 2026 so far:

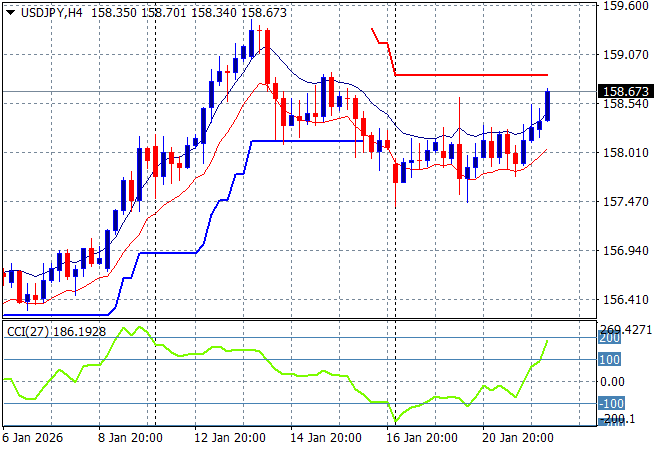

Mainland Chinese share markets are down slightly in the afternoon session with the Shanghai Composite staying just above the 4100 point level while the Hang Seng Index is off a little bit at 26550 points. Japanese stock markets have bounced back sharply with the Nikkei 225 up more than 2% to almost get back above the 54000 point level while Yen is losing ground against USD with the USDPY pair lifting well above the 158 level in what looks like a short term breakout:

Australian stocks are doing well with the ASX200 up nearly 0.8% to 8848 points while the Australian dollar extending above the 67 cent level to actually breach the 68 handle on the very solid jobs number report:

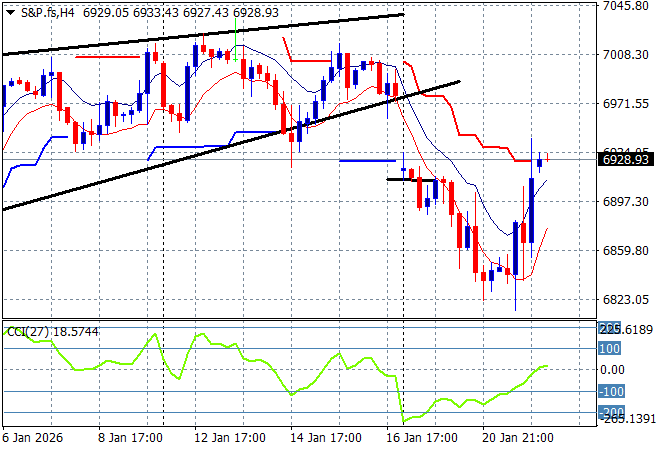

S&P futures are lifting as Wall Street rallies behind another Trump self-own with the S&P500 four hourly chart showing a bounce off support at the 6800 point level but is this a dead cat bounce?

The economic calendar is US centric tonight with weekly initial jobless claims, Q3 GDP data and then PCE income data.