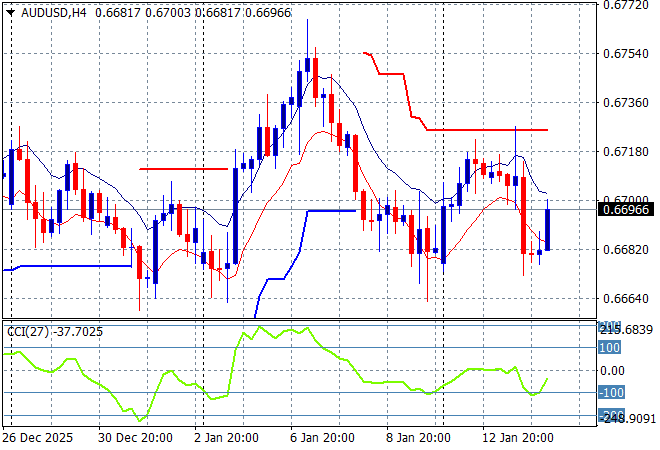

Asian share markets are still lifting across the board, performing better than transatlantic shares at least despite some mixed economic news from Japan and China. The rising tensions in Iran with the Trump regime standing by with itchy trigger fingers is keeping oil elevated while the USD remains somewhat firm despite a softer than expected inflation print overnight. The Australian dollar is trying to get back above the 67 cent level.

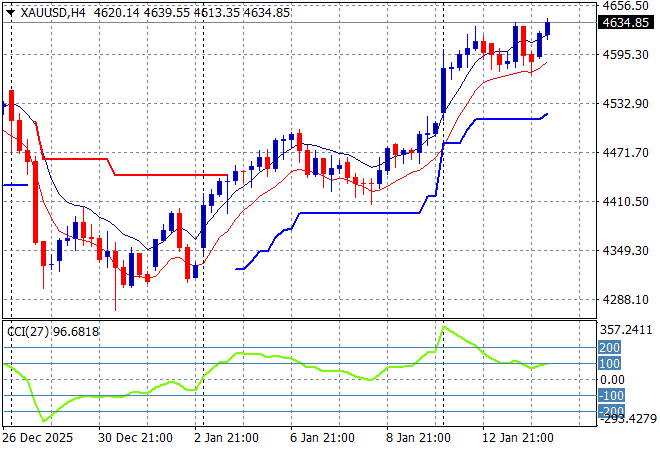

Oil markets are seeing another lift again with Brent crude pushing above the $65USD per barrel level while gold continues to move ever higher with another lift above the $4600USD per ounce level (and silver above $91!):

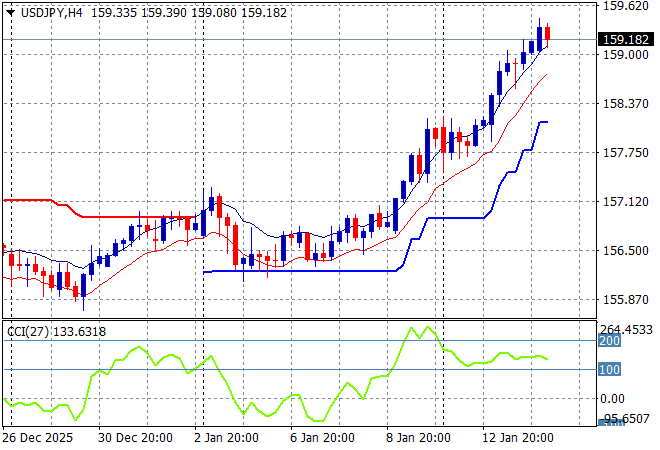

Mainland Chinese share markets are stalling again in the afternoon session with the Shanghai Composite up just a handful of points while the Hang Seng Index has lifted some 0.5% to 26984 points. Japanese stock markets continue to be bid strongly with the Nikkei 225 putting on another 1% to crack the 54000 point level while the weakening Yen is taking the USDPY pair through the 159 level:

Australian stocks managed to only just finish in the green as the ASX200 lifted a smidge over 0.1% higher to 8820 points while the Australian dollar is trying to bounce back but still faces short term resistance at the 67 cent level:

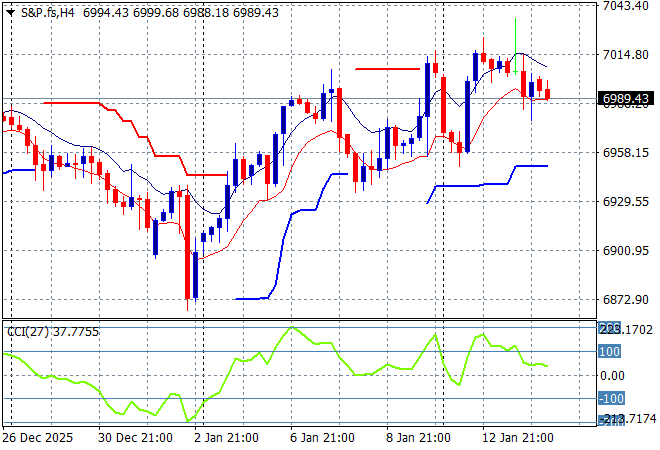

S&P futures are failing to make headway given the unsettled finish overnight with the S&P500 four hourly chart wanting to get up towards the 7000 point level but it’s still a bridge too far:

The economic calendar will focus on the latest US PPI print plus retail sales for November plus quite a few Fed speeches – I wonder if these members will toe the Trump line?