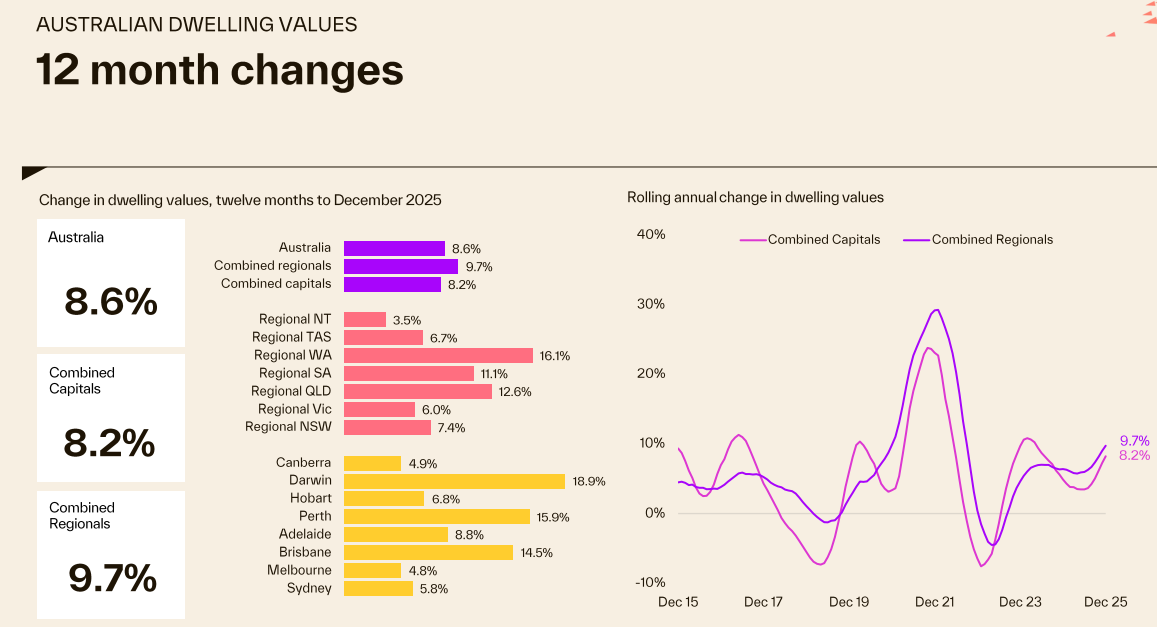

Cotality has released its Chart Pack for December, which shows that dwelling values nationally increased by 8.6% in 2025, with the regions (9.7%) outpacing the capital cities (8.2%):

Source: Cotality

Cotality also reported that Australia’s dwelling stock was valued at $12.3 trillion at the end of 2025, spread across 11.4 million homes.

This means that the average home in Australia was valued at an extraordinary $1,079,000 as of 31 December 2025.

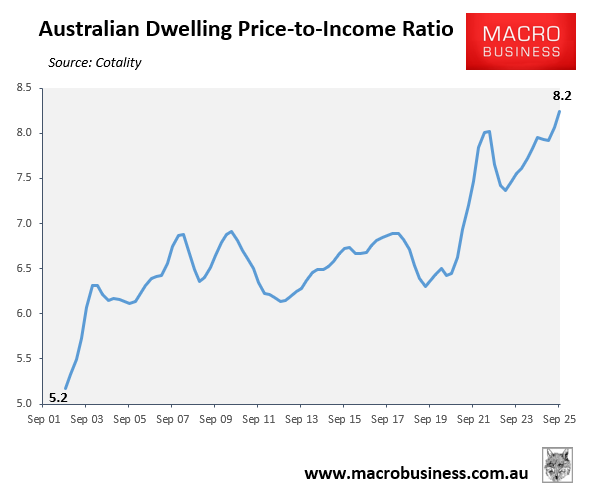

It is no surprise, therefore, that Cotality’s latest housing affordability report posted a record high dwelling value to income ratio of 8.2 as of September 2025, up from 5.2 in September 2002:

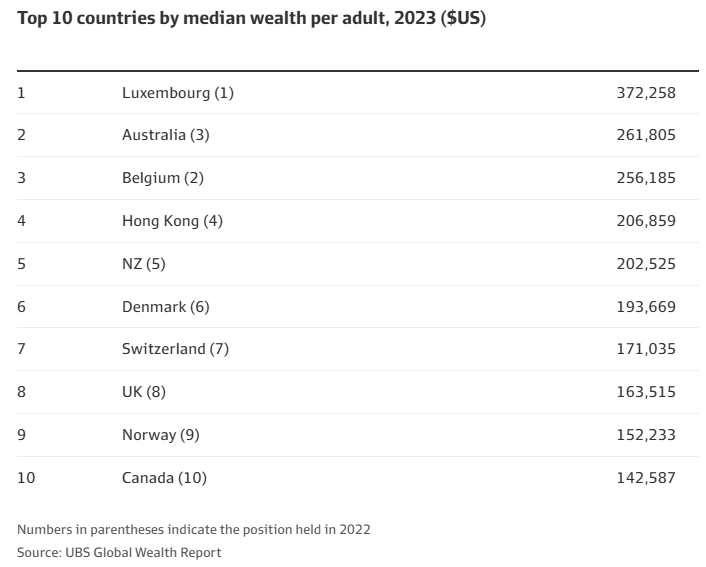

With Australia’s home ownership rate tracking at around 66%, the obscene value of housing is the primary reason why the UBS Global Wealth Report consistently reports Australians as having the second wealthiest households on the planet:

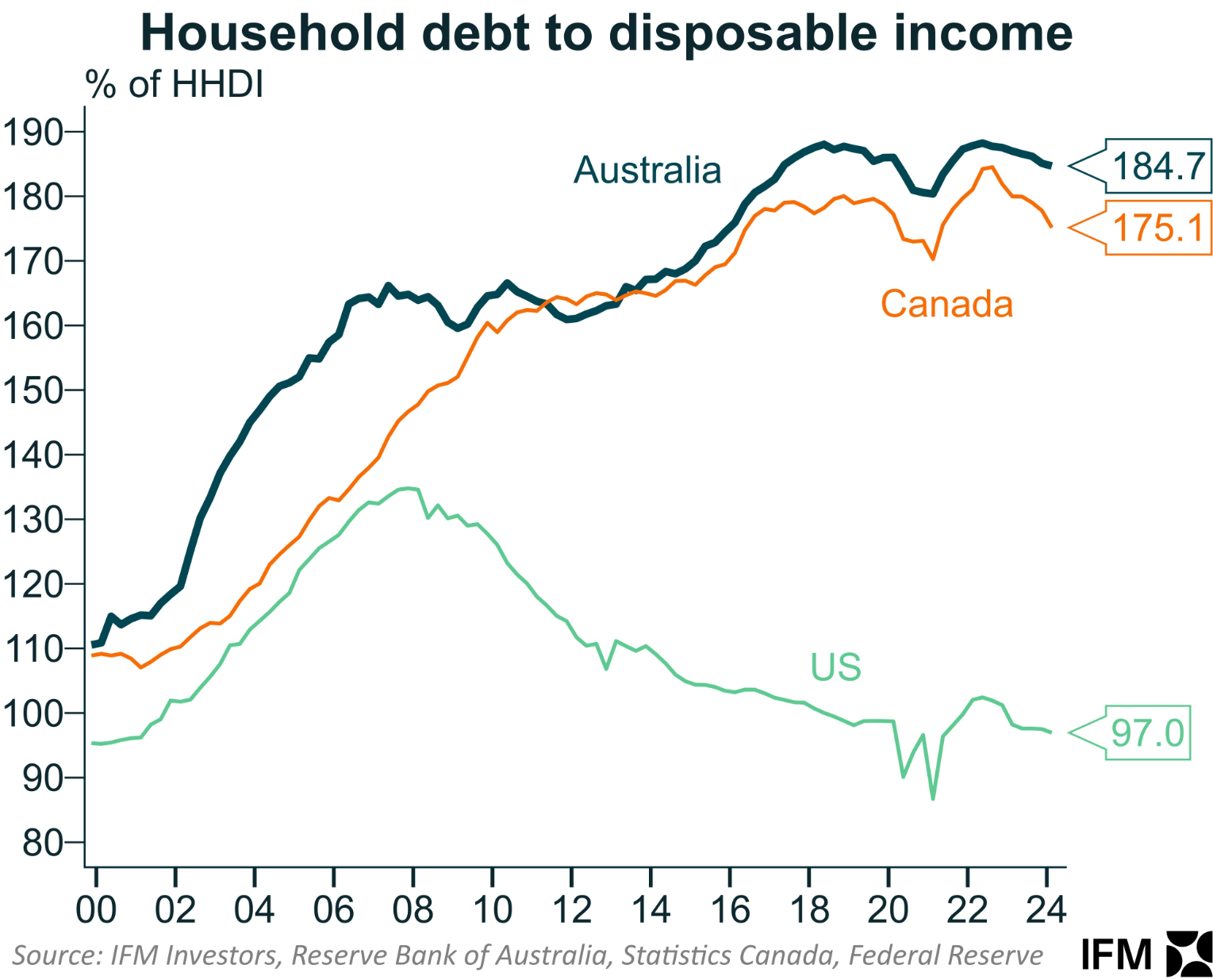

Meanwhile, Australians have buried themselves in mortgage debt, with the inexorable rise in the average loan size driving prices higher:

As a result, Australian households carry some of the world’s highest debt loads:

Are Australians truly “wealthy” when housing affordability is at an all-time low, and the nation’s younger generations cannot purchase a home without parental financial assistance and drowning themselves in debt?

Australians would be “richer” if property values had not risen so far, the average dwelling price was $550,000 rather than $1,079,000, and household debt was 95% rather than 185% of income.

Australia would be a far more equal society, and Australians would be financially better off if our homes were half the price they are now and we did not carry so much debt.

The surge in Australian home prices has had a detrimental impact on our children, grandkids, and future generations, who will be required to pay significantly more for housing than they should, leaving them poorer.

A home’s practical purpose remains the same whether it costs $500,000 or $1 million.

Higher “wealth” derived from having more expensive housing is meaningless to the majority of Australians who simply live in their homes and do not own investment properties.

The Takeaway:

Most of Australia’s world-beating household wealth is fictitious since it is locked up in overpriced homes that cannot be realised.

Future Australians must endure a lifetime of mortgage debt servitude or risk becoming trapped in the insecure rental market.

Australians would be significantly better off if we had avoided the 25-year property boom and a top spot in the world’s wealth rankings.