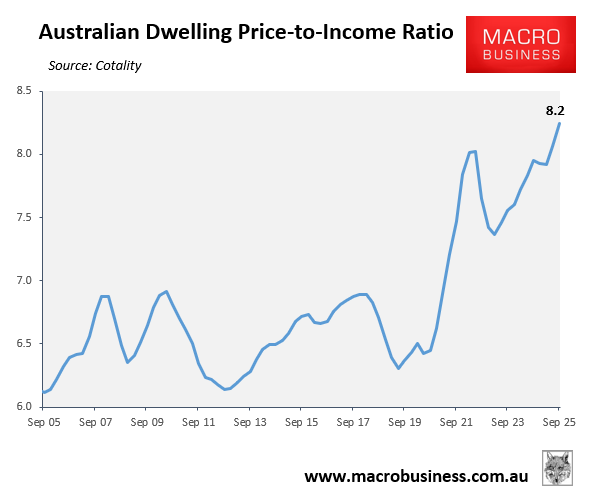

According to Cotality, Australia’s dwelling value-to-income ratio was tracking at a record high of 8.2 in the September quarter of 2025.

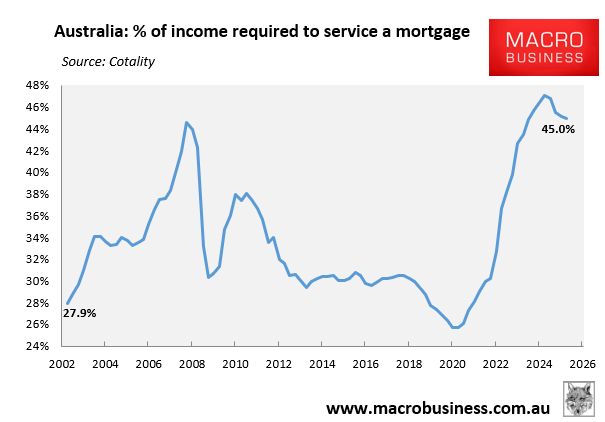

Despite three 25-bp interest rate decreases from the Reserve Bank of Australia (RBA), the percentage of median family income required to service a new mortgage on a median-priced home was still historically high, at 45.0%.

Most economists and financial markets expect the RBA to hike the official cash rate once or twice this year.

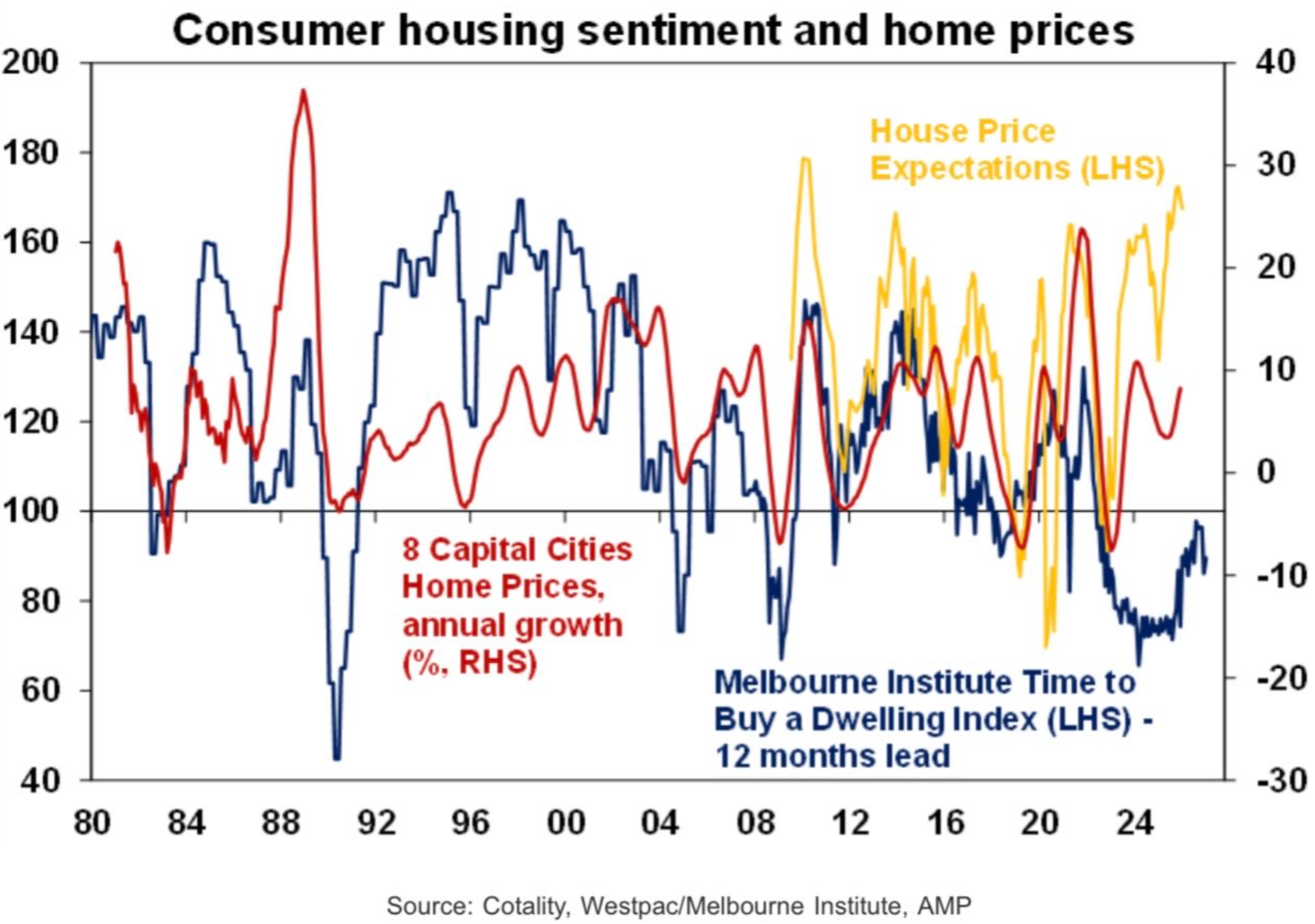

Despite the widespread expectation of rate hikes, the latest Westpac consumer sentiment survey revealed that households remain very bullish on house prices, although perceptions regarding whether it’s a good time to buy a dwelling remain relatively low:

As illustrated above by Shane Oliver at AMP, house price expectations are tracking at close to their highest level in 16 years.

The prospect of further house price increases and rising interest rates is obviously bad news for anybody seeking a more affordable housing market.

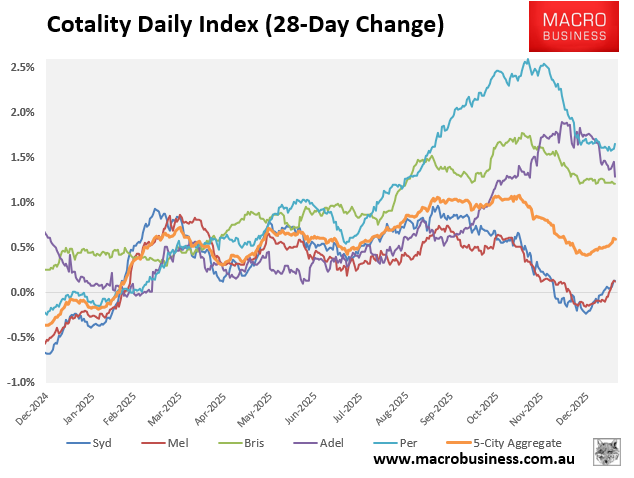

Cotality’s daily dwelling values index has rebounded, driven by Sydney and Melbourne, following seasonal weakness at the end of 2025:

As illustrated above, the 28-day growth rate of dwelling values across the five major capital city markets has accelerated from 0.4% at the end of 2025 to 0.6% currently.

This acceleration in price growth has been led by Sydney and Melbourne, which have rebounded from negative price growth at the end of 2025 (i.e., -0.2% and -0.1%, respectively) to moderate price growth currently (i.e., +0.1% each).

By comparison, Brisbane’s and Adelaide’s value growth has softened slightly so far this year but remains strong (i.e., 1.2% and 1.3%, respectively), whereas Perth’s value growth has remained stable and strong at 1.7%.

The softer conditions in Sydney and Melbourne largely relate to their greater relative supply of homes listed for sale:

As illustrated above by CBA, Sydney and Melbourne for-sale listings are tracking well above the five-year average, whereas they are tracking well below average across the other major capital city markets.

The relative abundance of supply in Sydney and Melbourne means that buyers face less competition to secure a home, which has moderated price growth.

By contrast, the other major capitals resemble the housing ‘Hunger Games’, which is fueling FOMO (‘fear of missing out’) and strong price growth.