Australia’s November CPI release from the Australian Bureau of Statistics (ABS) reported that housing inflation rose by 5.2% over the year to November 2025. This made housing the single largest contributor to annual inflation in that release.

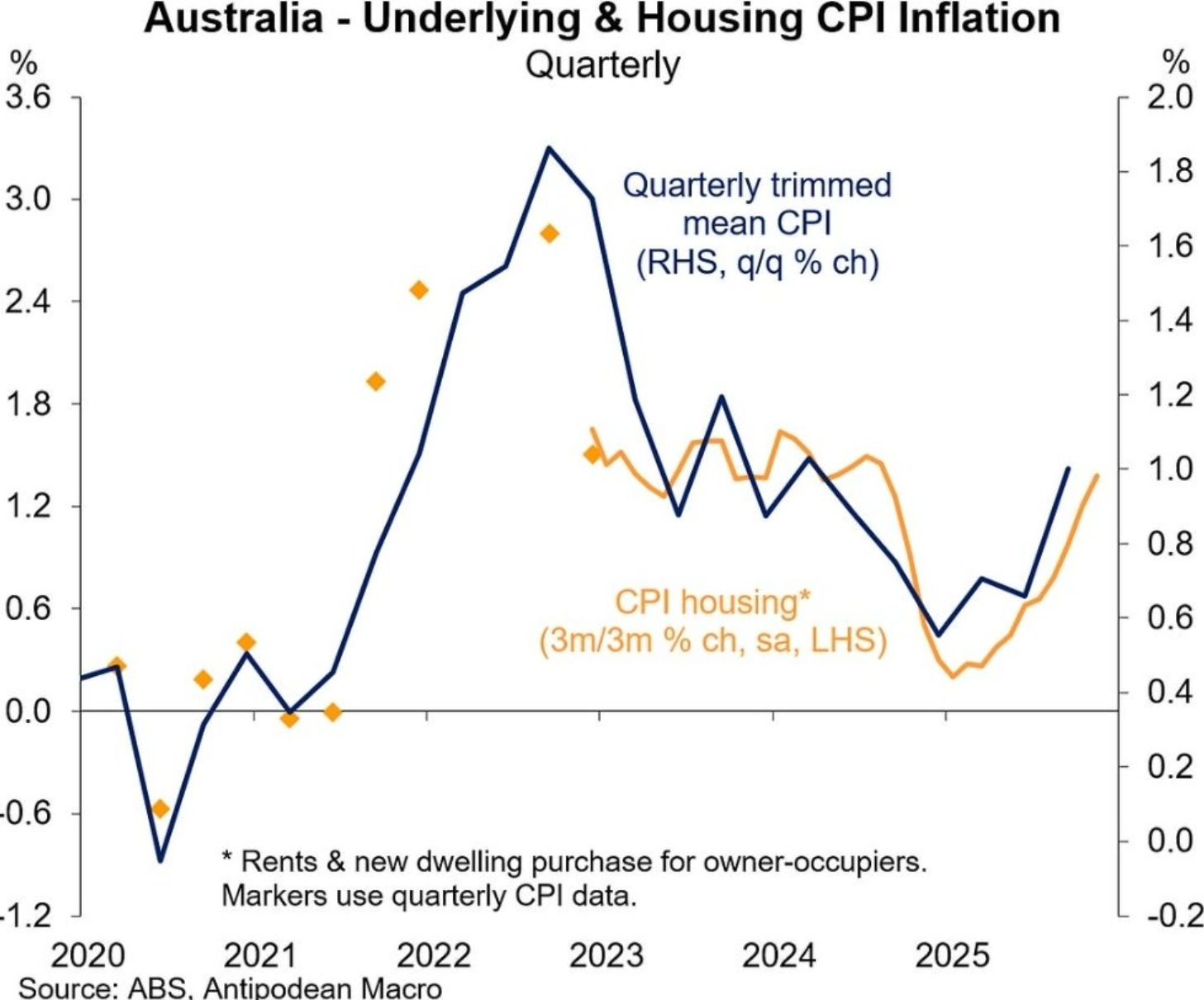

The following chart from Justin Fabo at Antipodean Macro illustrates the quarterly acceleration in housing inflation, which has rebounded alongside underlying (trimmed) mean inflation:

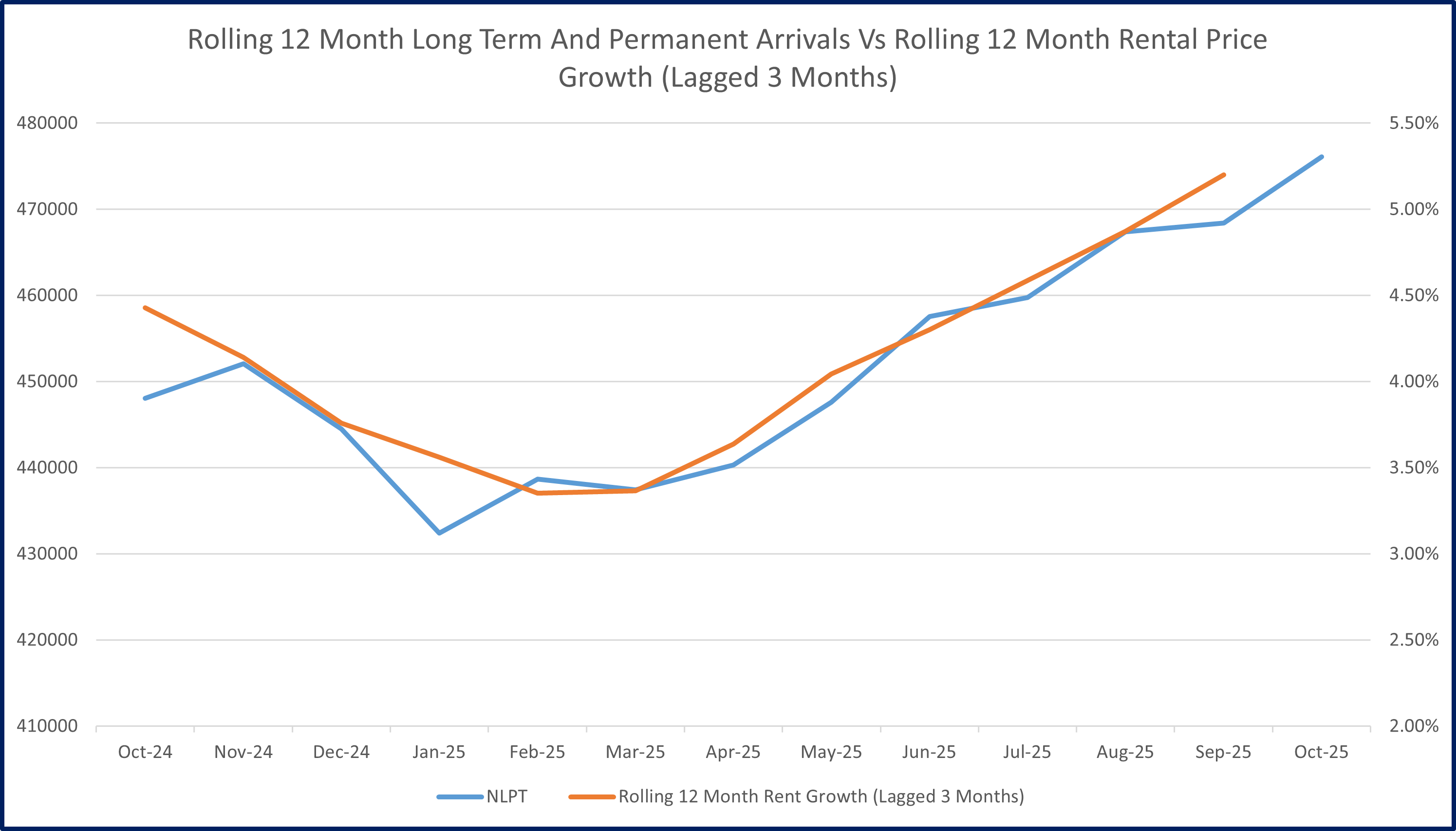

Australian housing inflation is facing upward pressure on multiple fronts.

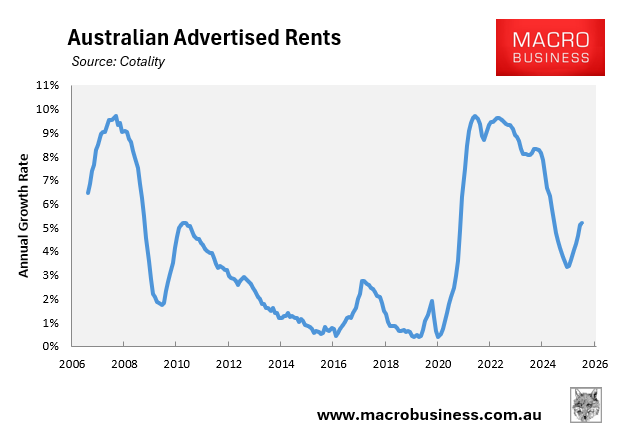

First, advertised rents have reaccelerated, which are typically a leading indicator of CPI rents.

As illustrated below, Cotality reported that advertised rents rose by 5.2% in the year to December 2025, up from a low of 3.4% recorded in the year to June 2025:

The resurgence in advertised rents points to higher CPI rents in the period ahead, which will place upward pressure on overall CPI inflation.

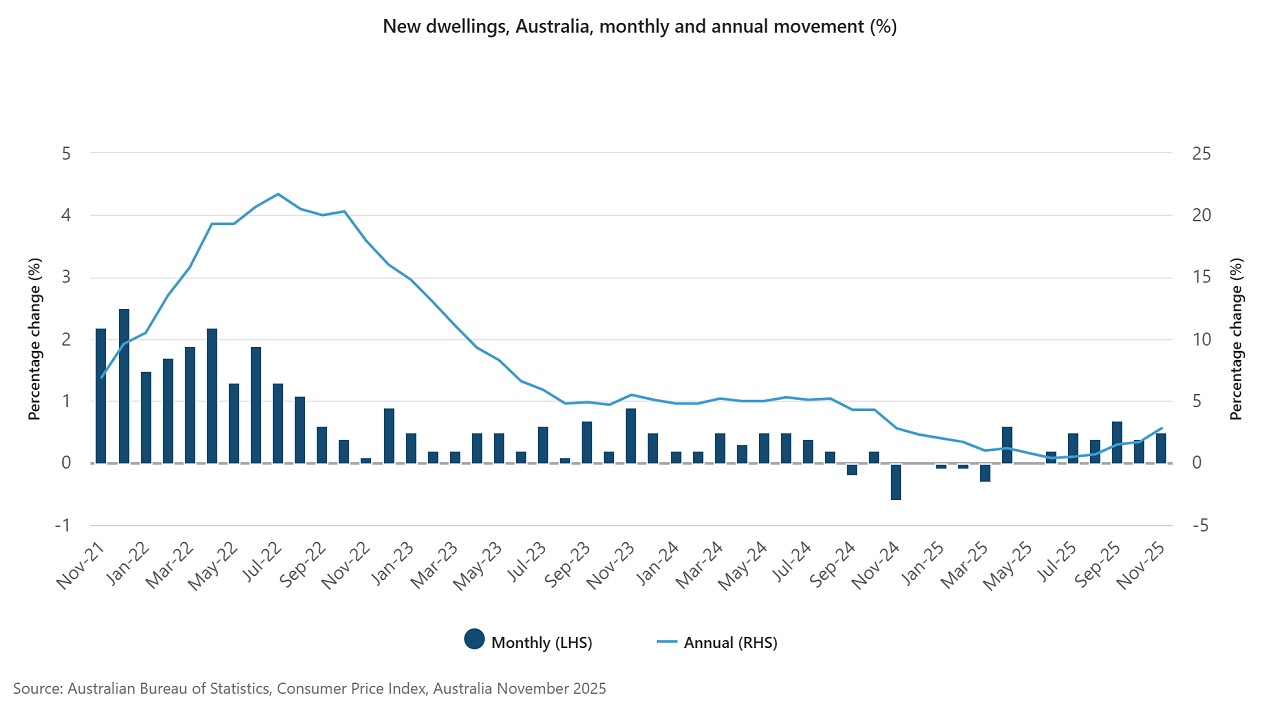

Second, new dwelling prices in Australia’s CPI, which measure the change in the construction cost of building a new home (excluding land), reaccelerated over the second half of 2025, as illustrated below:

Annual new dwelling price inflation strengthened to 2.8% in November 2025, up from the low of 0.4% in June 2025.

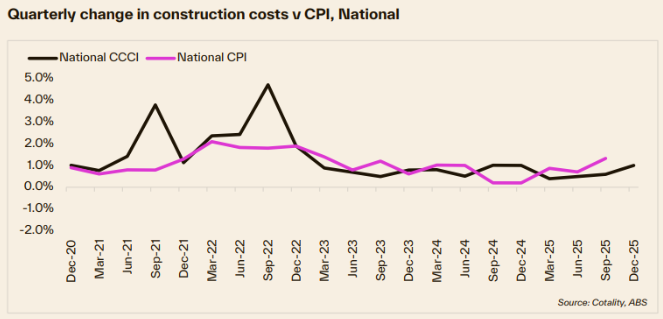

The latest Cotality-Cordell Construction Cost Index (CCCI), released today, also shows that construction costs accelerated in late 2025 to 1.0% in Q4, the fastest quarterly increase of the year.

The result marked a notable acceleration from the modest quarterly increases of 0.4%, 0.5%, and 0.6% recorded earlier throughout 2025.

With housing demand remaining strong amid strong net population arrivals and housing construction remaining sluggish, housing inflation is likely to climb higher in 2026.

Source: Tarric Brooker

Given that housing comprises just over 21% of Australia’s CPI basket, any increase in housing inflation will obviously place upward pressure on overall CPI inflation.