Louis Christopher, founder and managing director of SQM Research, posted the following tweet on Twitter (X), warning that large house price falls “can and will” happen in large cities:

Christopher’s tweet was in response to a report on London’s housing market reporting losses of up to 34% for owners of flats, with “hundreds of thousands of pounds wiped from the value of their properties”.

Australia’s two most similar economies—New Zealand and Canada—have also experienced heavy house price losses.

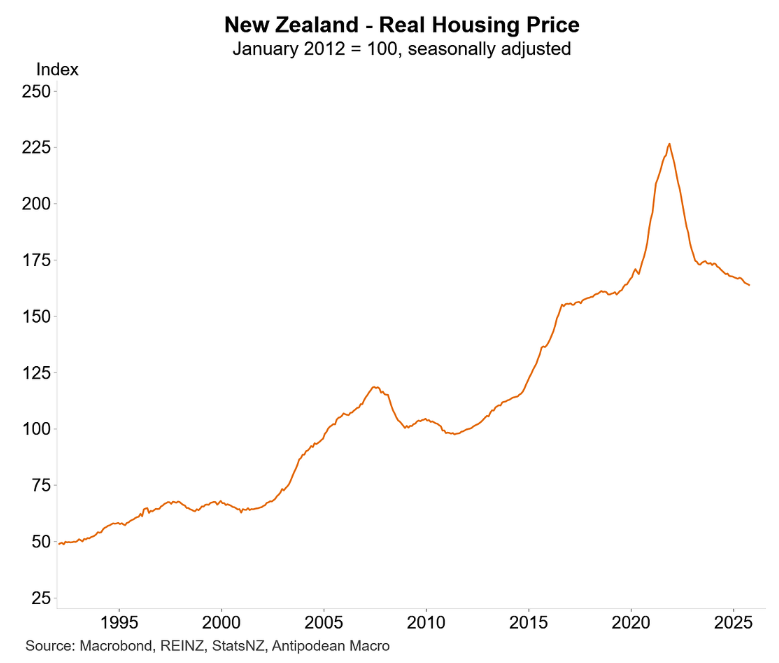

New Zealand has recorded its greatest house price decline in modern history, with values nationwide 15% lower than the 2021 peak in nominal terms and 31.3% lower in real inflation-adjusted terms.

Chart by Justin Fabo at Antipodean Macro

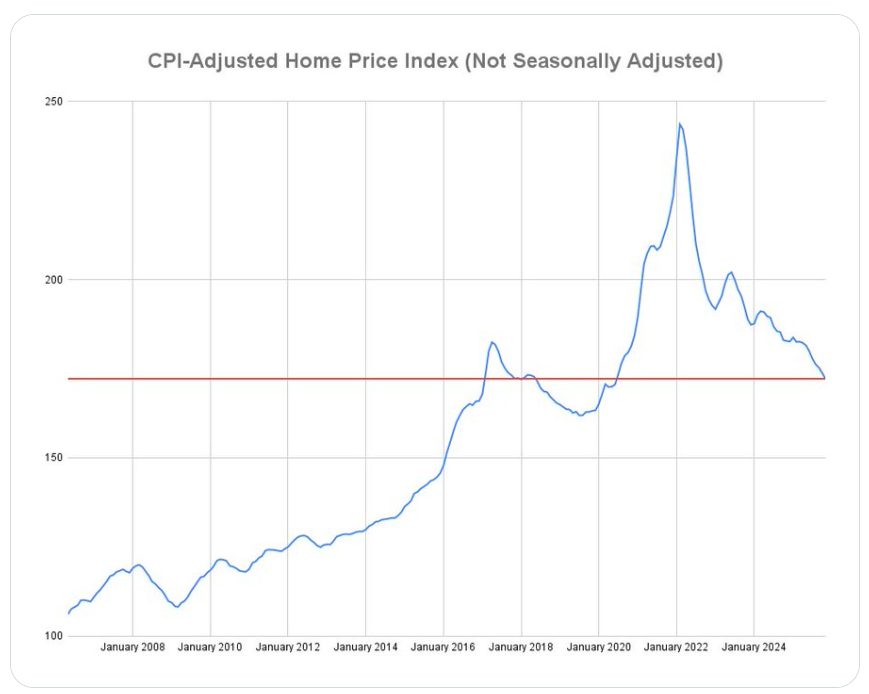

In real inflation-adjusted terms, Canadian home values have fallen back to where they were in February 2017:

Real Canadian home prices

The big question is: If Australia’s two most similar housing markets can experience sharp house price declines, could Australia’s housing market follow?

There are certainly compelling reasons to believe that Australian housing valuations are extreme, making prices vulnerable to a severe correction or crash.

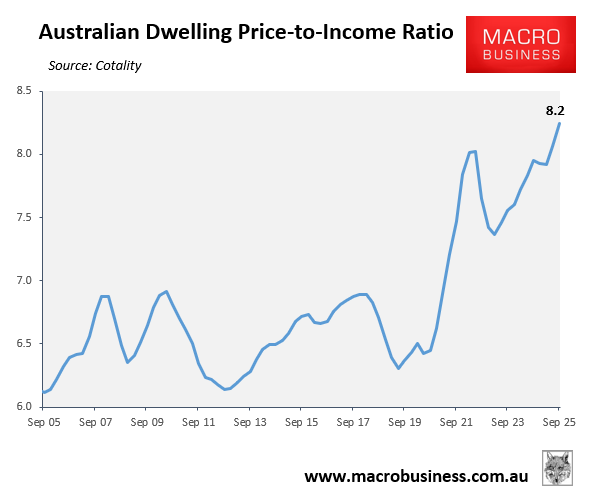

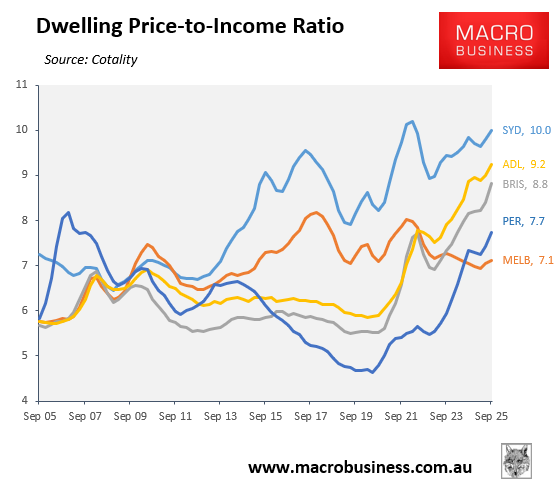

First, Australia’s dwelling value-to-income ratio was tracking at a record high of 8.2 in the September quarter of 2025, according to Cotality:

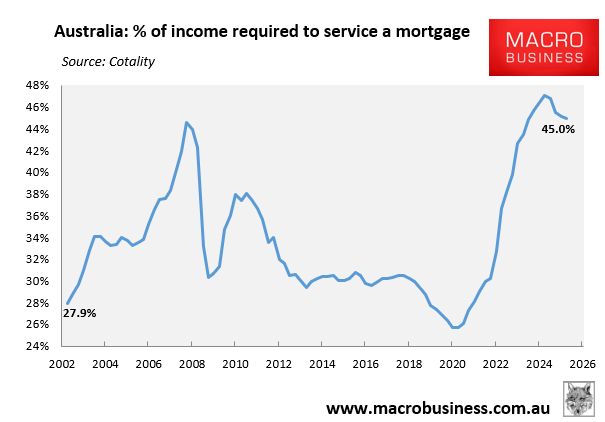

The percentage of median household income required to service a new mortgage on the median-priced home was also tracking at a historically high level of 45.0%, despite three 25-bp rate cuts from the RBA.

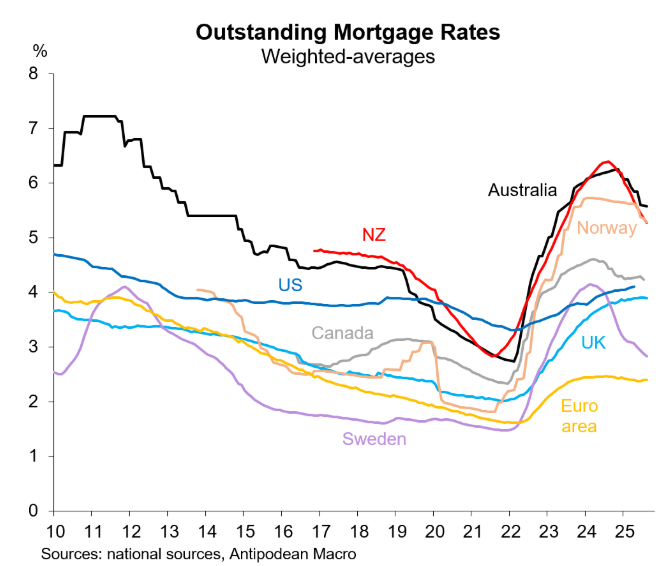

Australian dwelling values continue to grow at a solid clip, despite most economists expecting the RBA to deliver between one or two 25 bp rate hikes this year, which would obviously make the affordability situation even worse.

If two rate hikes were delivered by the RBA, Australia’s official cash rate would rise to 4.1% and average mortgage rates to around 6%—the highest in the world.

Chart by Justin Fabo at Antipodean Macro

At some point, a tipping point could be reached whereby the reduced mortgage affordability and borrowing capacity turns the ‘fear of missing out’ into a ‘fear of overpaying’, slashing demand and delivering a house price correction.

Of course, one major point of difference between Australia and New Zealand and Canada is that immigration remains strong in Australia, whereas it has collapsed in those nations.

As a result, Australia’s housing market remains heavily undersupplied, whereas they are oversupplied in New Zealand and Canada.

Even so, it remains a risky time to leverage into Australian property with a 5% deposit, as many first home buyers are currently doing.

Melbourne is the exception to this view, given it has experienced minimal price growth since 2017 and affordability has improved significantly.

Melbourne housing’s relative affordability makes it less vulnerable to a price correction and less risky than the other major capital cities.