Aborted house price boom eases RBA pressure

Last week’s Cotality’s daily dwelling values index, which tracks home values across Australia’s five major capital city markets, ended 2025 with momentum stalling.

At the aggregate 5-city level, Cotality’s daily dwelling values index rose 0.5%, down significantly from the 1.0% growth recorded in November.

Today, we get the release of PropTrak’s competing series, which shows similar patterns of slowing growth and putative falls in prices.

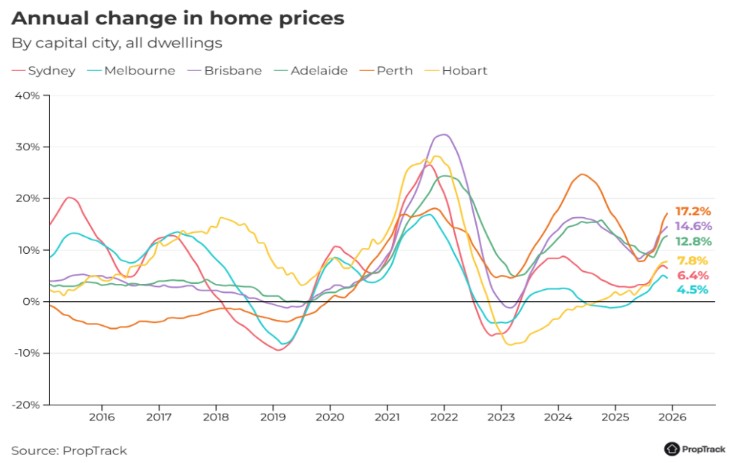

In December, national home prices rose a meager 0.1% over the previous month to reach a new high. As a result, the median home value increased to $880,000, an 8.8% annual increase.

However, home prices fell in December in Sydney (-0.3%), Melbourne (-0.3%), and Canberra (-0.2%).

Among the capitals, Adelaide (+0.8%), Brisbane (+0.5%), and Perth (+0.5%) saw the most monthly price rises.

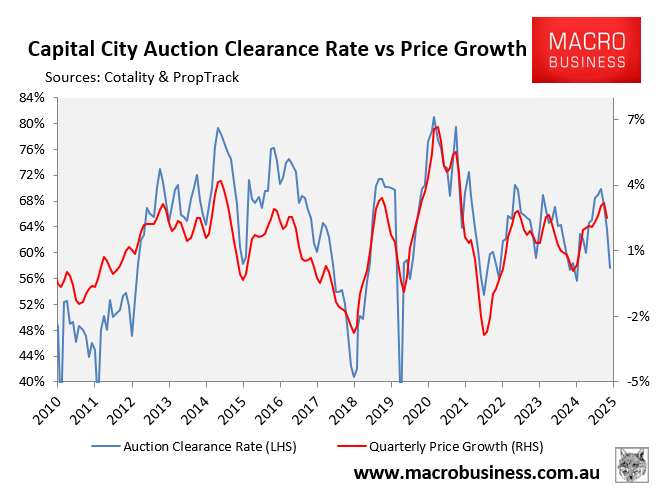

Auction clearance rates suggest a further stall ahead for prices.

The varying supply-demand dynamics in those markets are reflected in the relative strength elsewhere and the weakness in Sydney and Melbourne.

Listings in Sydney and Melbourne are tracking above the five-year norm. In contrast, listings in the other major markets are tracking significantly below the five-year average, as shown below by CBA:

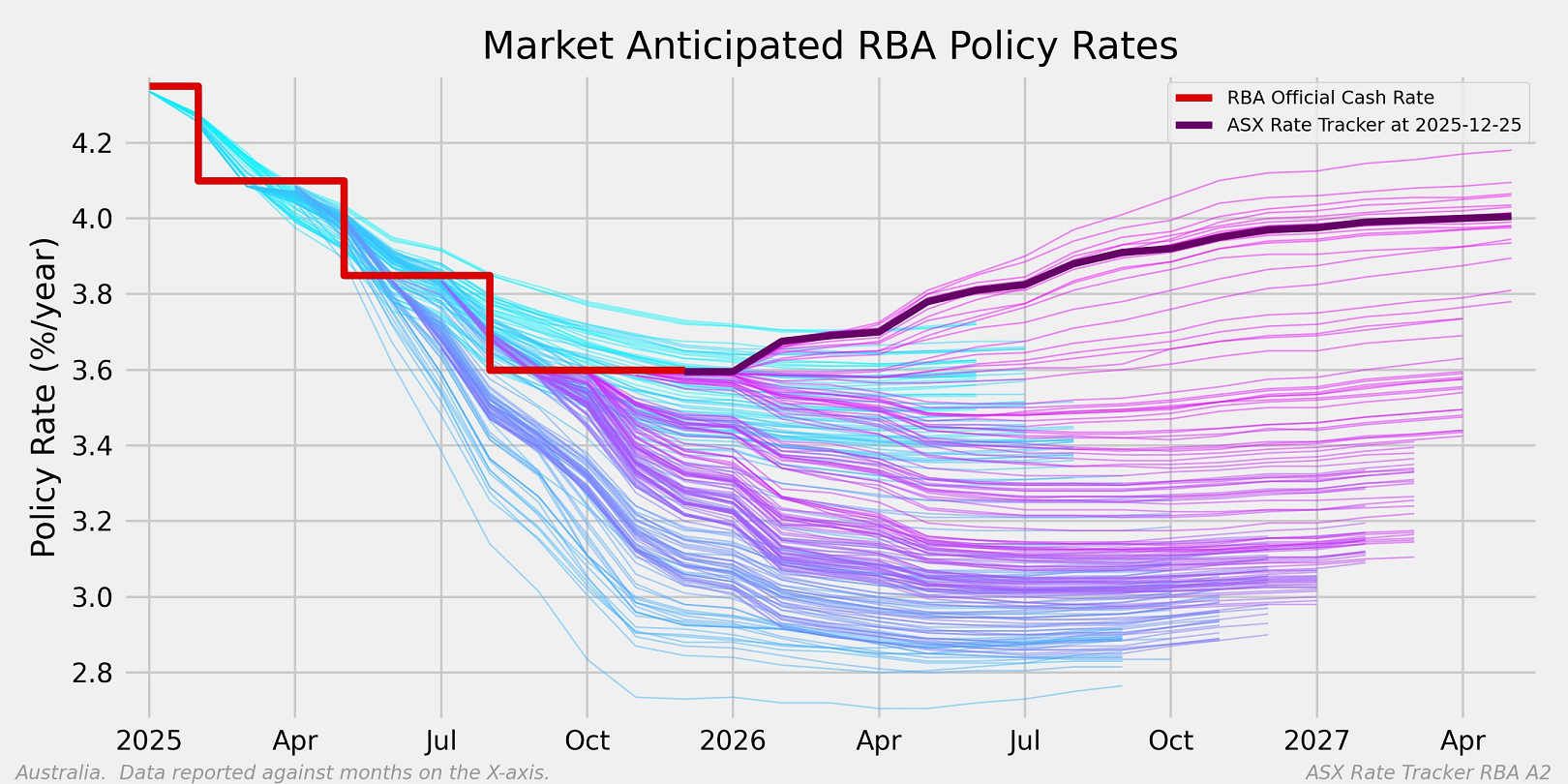

Sydney and Melbourne led the overall slowdown in home value rise toward the end of 2025, which is indicative of changing interest rate expectations.

Source: Mark Graph

Three months ago, economists and financial markets predicted two more rate reductions; today, they predict two rate increases in 2026.

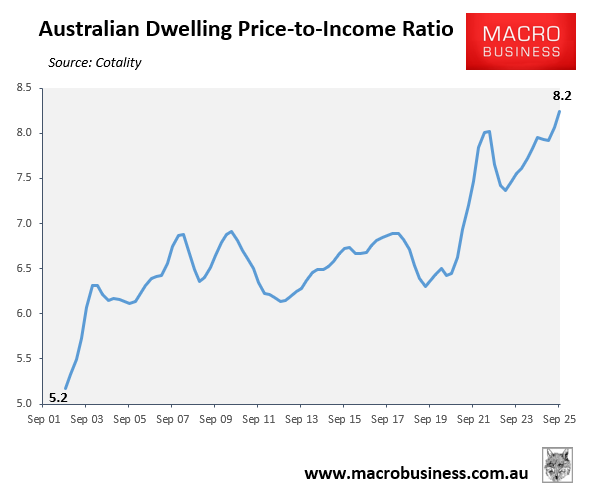

Due to the historically low cost of housing in Australia, purchasers need more rate reductions to boost borrowing capacity, make mortgages more affordable, and raise prices.

The pace at which prices are slowing and falling in major markets suggests a broader impact on consumption growth is coming and less pressure on the RBA to deliver rate hikes.