Charts from TME. Is there a relationship between the Japanese long end and gold? Maybe. If so, YCC would create a divorce.

Gold volatility says there’s no panic yet.

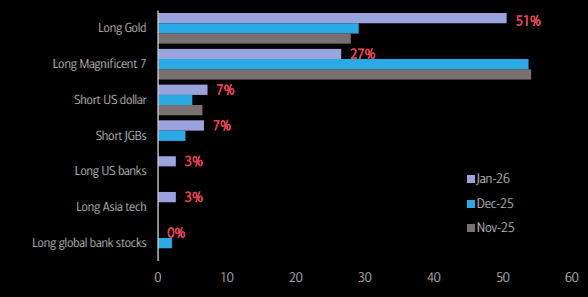

Same regarding speculators.

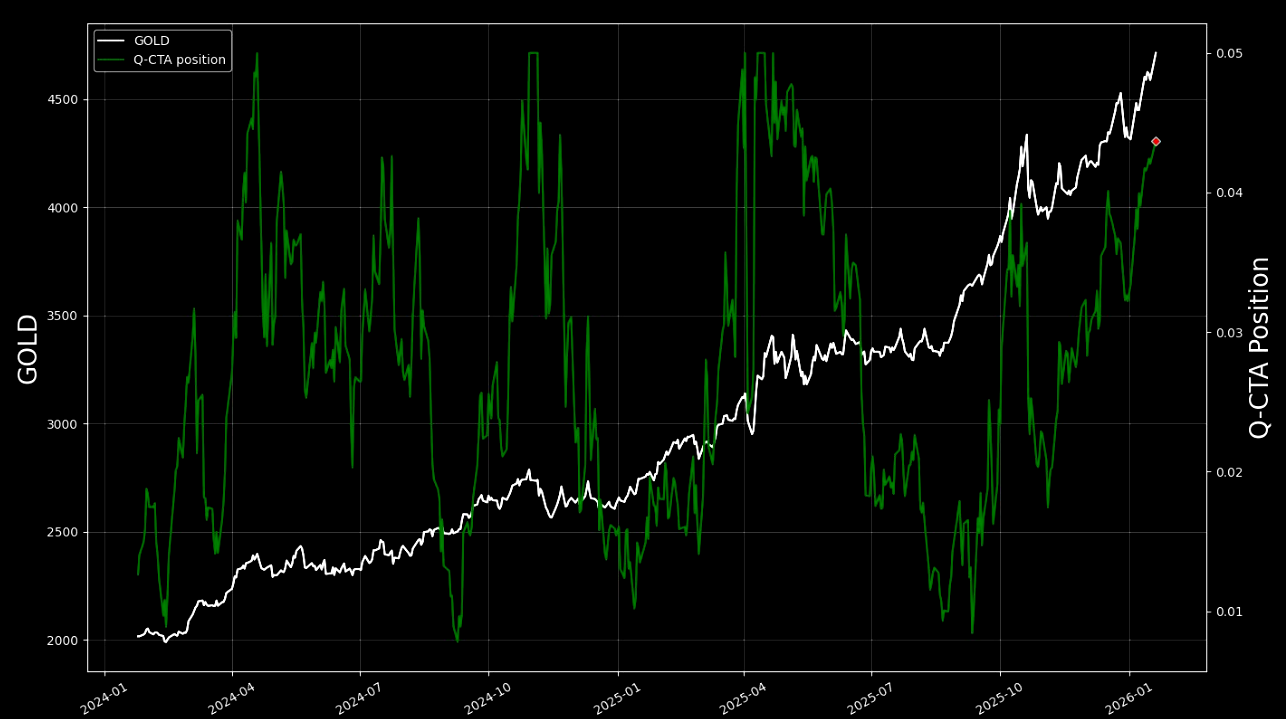

CTAs are more fully invested.

The miner’s leverage to prices is normal.

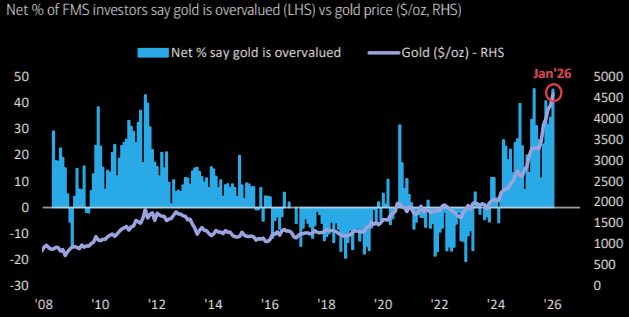

A few overheated signs.

My own view is that gold is the Trump metal more than Japanese metal. It benefits from everything he does:

- instability in fiscal policy

- instability in monetary policy

- instability in treasuries

- instability in DXY

- instability in American society

- instability in geopolitics.

Gold is the Trump hedge.

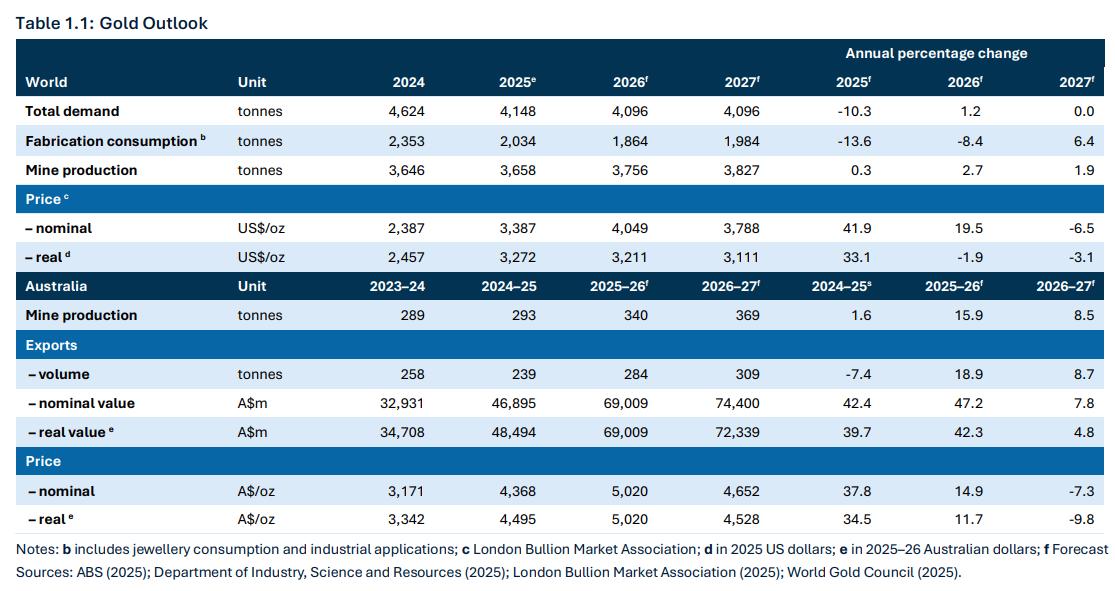

Meanwhile, Australia benefits. Via the Office of the Chief Economist.

If gold reaches $6000, it will overtake iron ore as the top national earner. The budget has forecast the opposite.

Bulk commodity prices are assumed to decline from elevated levels over four quarters to the end of the December quarter of 2026: the iron ore spot price is assumed to decline to US$60/tonne; the metallurgical coal spot price declines to US$140/tonne; the thermal coal spot price declines to US$70/tonne; and the LNG spot price converges to US$10/mmBtu. The gold price is assumed to decline over eight quarters to a long-run anchor. All bulk prices are in free on board (FOB) terms.

A literal river of gold is flowing towards the federal budget.