We have warned repeatedly that the state of Victoria is on the path to financial ruin.

Victoria has the highest per capita debt in the nation and the lowest credit rating.

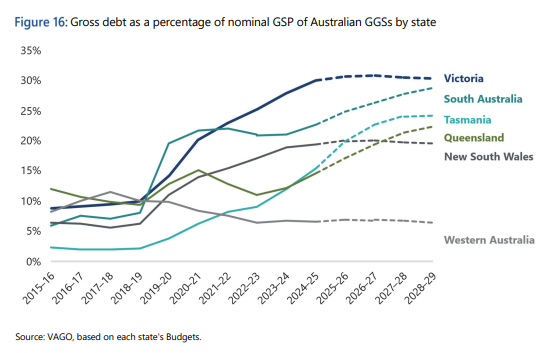

The Victorian Auditor‑General cautioned last month that debt, deficits, and infrastructure blowouts pose serious long‑term risks to the state’s financial sustainability.

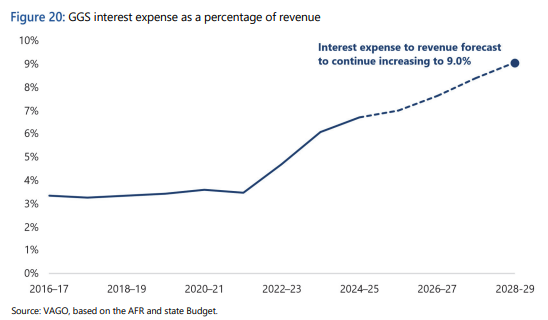

Victoria’s liabilities now exceed $150 billion, with debt servicing costs becoming a major budget challenge.

The world’s two largest credit rating agencies, S&P and Moody’s, have also warned that Victoria risks further rating downgrades if it does not bring its debt situation under control.

Further downgrades seem inevitable given that the Allan Labor government has signed major contracts for the $216 billion Suburban Rail Loop against the explicit advice of experts.

The increase in Victoria’s debt is especially problematic in light of the state’s poor growth, which makes servicing that debt more difficult.

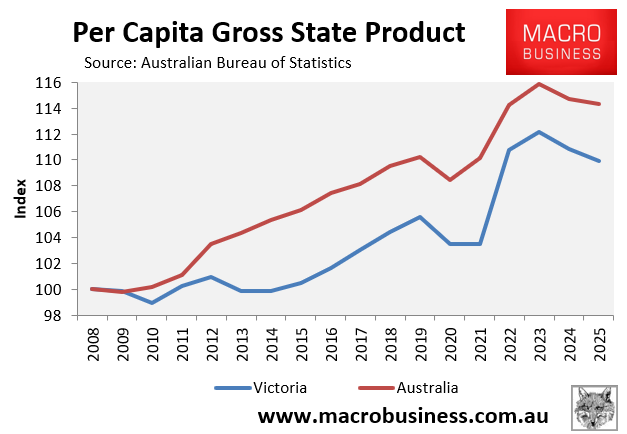

Last week, the Australian Bureau of Statistics (ABS) released the annual state accounts, which showed that Victoria’s per capita gross state product (GSP) fell by 0.8% in 2024-25 and has only risen by 10.0% since the Global Financial Crisis (GFC) hit in 2008.

This compares to a 0.3% national decline in per capita GDP in 2024-25 and a 14.3% increase since 2008.

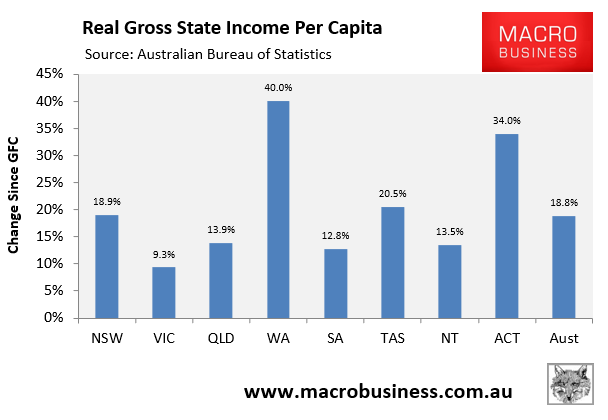

Victoria has also experienced the nation’s weakest growth in gross state income per capita since the GFC:

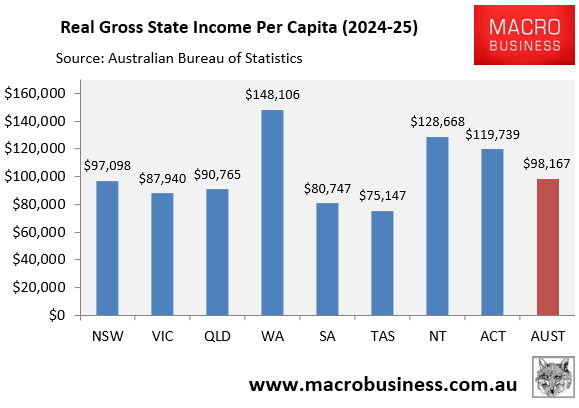

Victoria’s real gross state income was the third lowest in the nation in 2024-25, ahead of only Tasmania and South Australia:

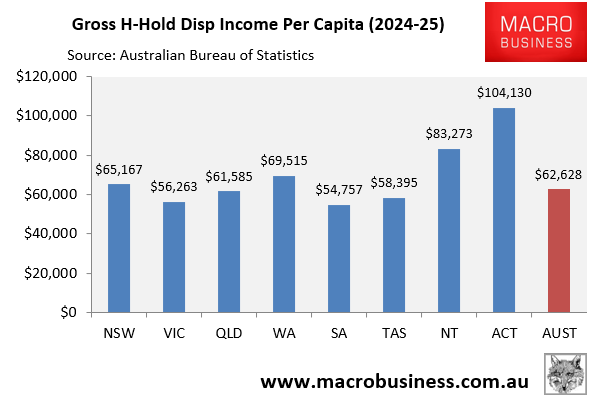

In 2024-25, Victoria’s gross household disposable income per capita ranked second lowest in Australia, only surpassing South Australia.

Victoria’s economic growth based on importing huge numbers of people to help build homes and infrastructure, as well as sell services to.

The state’s population has increased by an astonishing 2.4 million people (51%) this century and is officially forecast to grow by another 4.1 million people over the next 31 years:

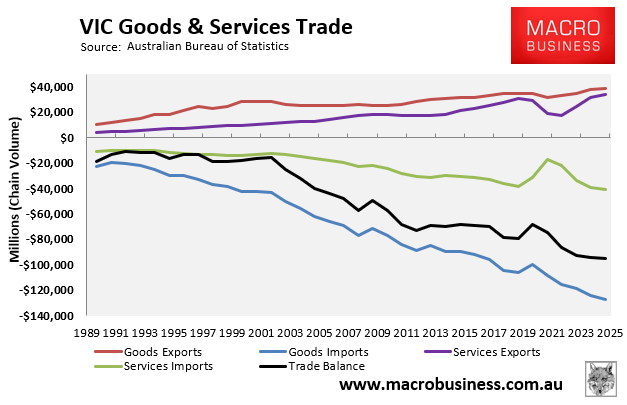

Victoria’s trade performance illustrates its false economy.

Exports have grown slowly during the last 20 years, while imports have more than doubled.

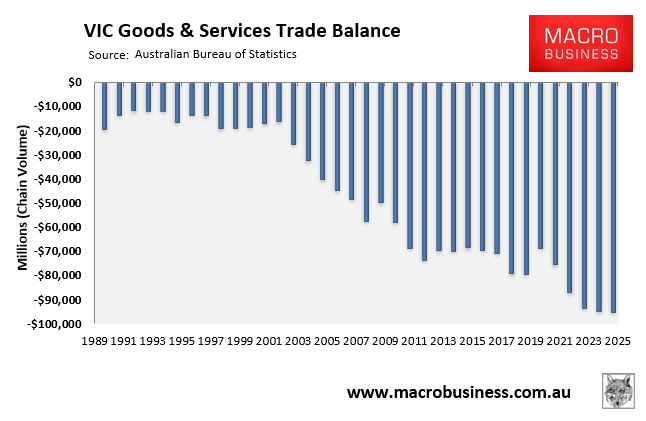

As a result, Victoria’s trade imbalance has ballooned to $94.7 billion in 2024-25.

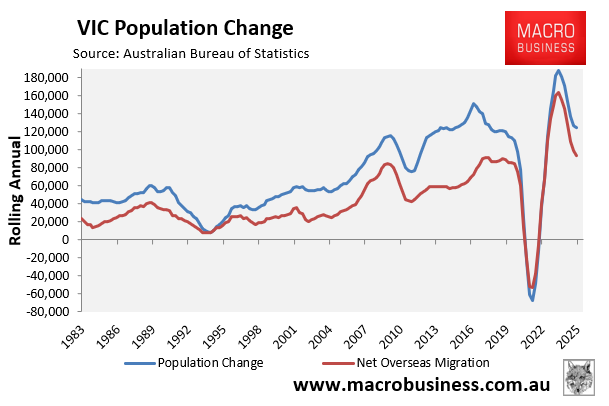

The surge in Victoria’s trade deficit corresponds to the commensurate surge in the state’s population growth, driven by net overseas migration:

Since few of these migrants work in exporting firms, more consumers has meant more net imports of goods and services.

Victoria (read Melbourne) is essentially draining financial resources from mining states to fund its population Ponzi scheme, as well as growing for the sake of growth via mass immigration and debt accumulation.

Meanwhile, the rapid population expansion has resulted in permanent infrastructural bottlenecks, increased congestion, reduced amenity, and declining housing quality (both size and location), which has lowered living standards for existing residents.

Victoria has also been plunged deeper into debt as it tries in vain to build its way out of the never-ending population crush.

How does the Victorian government aim to build an economy based on real and sustainable growth that improves the incumbent population’s standard of living? Because continuing with the same failed Ponzi model will achieve the same results: economic decline, reduced standard of living, and a potential debt crisis.