By Lucinda Jerogin, Associate Economist at CBA

- The RBA left the cash rate on hold in a unanimous decision that was widely expected. The Statement took a step in the hawkish direction, but it was the Governor’s post meeting press conference that cemented the end of the easing cycle and warned of potential hikes.

- The unemployment rate held steady at 4.3% in November.

- Offshore, the FOMC cut the funds rate by 25bp to 3.50-3.75%. The Bank of Canada kept rates on hold.

- The week ahead brings the release of the Australian Government’s Mid-Year Economic and Fiscal Outlook. Consumer sentiment data is also due.

- Abroad, three central banks meet. In Europe, the ECB is expected to keep rates on hold while the Bank of England is likely to cut. Closer to home the Bank of Japan is expected lift rates.

The race up to Christmas continued this week in global financial markets with a steady flow of data and central bank meetings. But if an RBA rate cut was on your Christmas wish list, the December Board Meeting shut down any prospect of that.

On Tuesday, the RBA left the cash rate on hold in a unanimous decision that was widely expected. The Decision Statement took a step in the hawkish direction recognising upside risks to inflation and recent strong activity data.

However, it was the post meeting press conference that leaped forward with the Governor effectively ruling out rate cuts in 2026 and flagging potential rate hikes next year.

We continue to expect the cash rate to remain on hold from here. But as we have flagged in recent weeks, the risks clearly sit to higher rates in 2026. The next Board meeting on 2-3February is ‘live’ and Q4 CPI data (due 28/01) will be critical.

Another important aspect of the data to watch is the labour market. On Thursday, the labour force lottery struck again with a strange set of numbers. In November, seasonally adjusted employment fell 21.3k and the participation rate declined to 66.7%, keeping the unemployment rate steady at 4.3%.

This appears soft, however in trend terms employment rose 21k and the unemployment fell from 4.4% to 4.3%. We place more weight on the trend figures as the seasonally adjusted numbers can swing sharply.

Looking through the noisy release, the focus for us was a fall in the trend unemployment rate to 4.3%. This along with our internal data signals a labour market still on a very solid footing and too tight for comfort for the RBA.

Offshore this week news was dominated by central bank meetings. On Wednesday the FOMC cut the Fed Funds rate by 25bp to 3.50–3.75%, as widely anticipated. However, the decision was not unanimous, with two regional Fed presidents voting to remain on hold, and Stephen Miran voting for a larger 50bp cut.

The dot plot points to one further rate cut in 2026, but a key consideration for the path of monetary policy is the election of the new FOMC Chair. Kevin Hassett, who is dovish on monetary policy, is widely expected to be President Trump’s nominee.

In light of this, our international economics team expect the FOMC to cut rates three more times by 25bp in 2026 to 2.75%-3.00%.

North of the border the Bank of Canada held interest rates steady at 2.25%. The BoC was cautiously optimistic about prospects for the Canadian economy, however, remained alert to the ongoing weakness in trade-sensitive sectors. Our international economics team continue to expect the BoC to keep rates on hold for the foreseeable future.

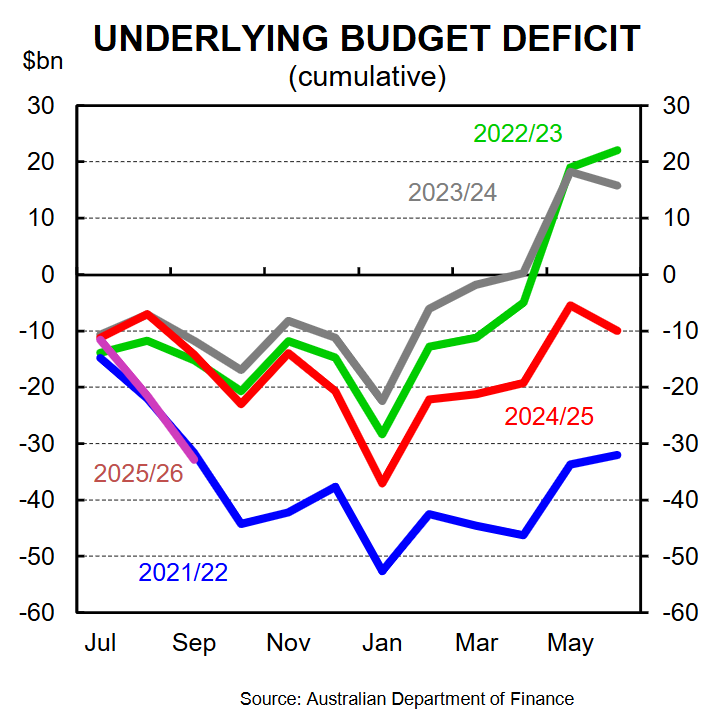

Turning our attention to the week ahead and locally the MYEFO is scheduled. We anticipate a stronger Australian economy and higher iron ore prices have supported revenue to date in 2025-26. We estimate the underlying budget deficit will print at $32bn, a $10bn improvement from the forecast $42bn deficit in March. The risks lie with a smaller deficit.

Also in Australia next week, consumer sentiment data is due. It will be interesting to examine the effect of a more hawkish RBA board on consumers’ outlook, particularly given the surge in sentiment last month (+12.8%/mth). A sharp fall may suggest hawkish signalling will sway activity in the economy.

Abroad, three central banks meet. In Europe, the ECB is expected to leave the deposit rate unchanged while the Bank of England is likely to cut. Closer to home we expect the Bank of Japan to lift its policy rate by 25bp.

In economic data, Canadian, UK, Japanese and US CPI are due. In New Zealand, the Half Year Economic and Fiscal update and Q3 GDP will be released.