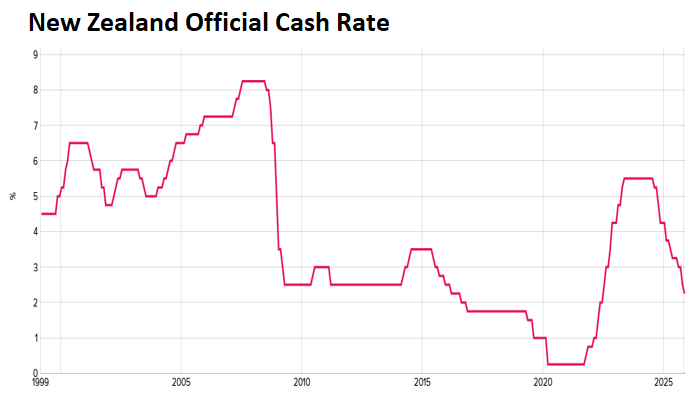

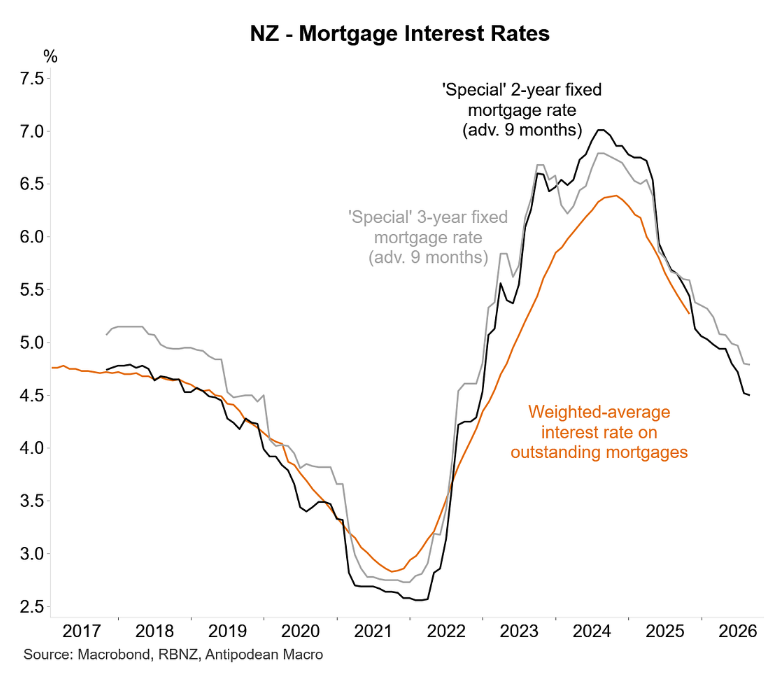

The Reserve Bank of New Zealand has delivered 3.25% of interest rate cuts since July 2024.

This reduction in the OCR has delivered a corresponding decline in new mortgage rates to pre-pandemic norms:

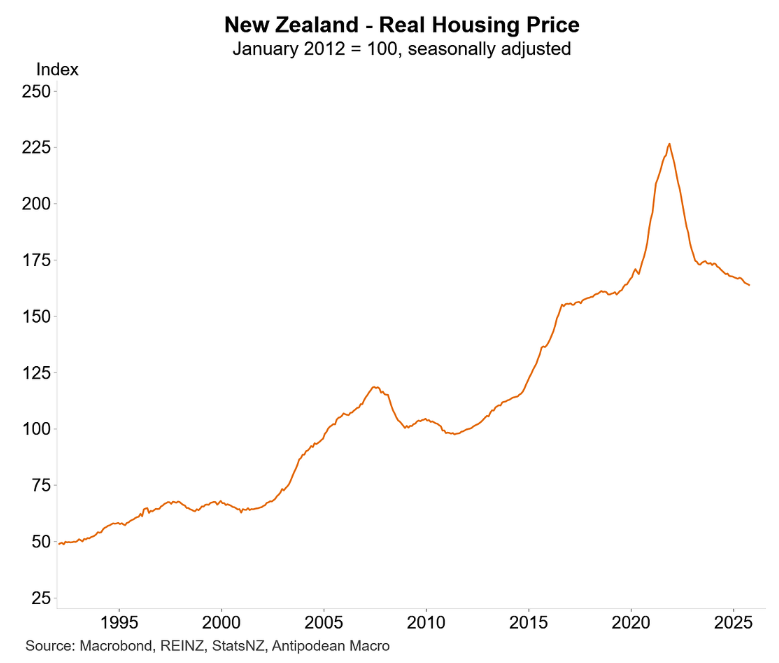

Normally, such a sharp reduction in mortgage rates would result in a lift in homebuyer demand and prices. However, as illustrated below by Justin Fabo from Antipodean Macro, the REINZ house price index has crashed to 2019 levels in real inflation-adjusted terms:

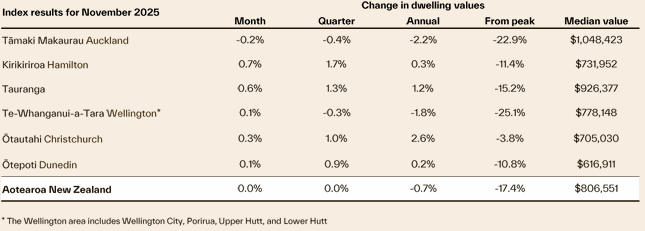

The latest dwelling value results from Cotality have been released, which show that home values in nominal terms were flat in the month of November and the quarter and were down 0.7% over the year.

Source: Cotality

New Zealand home values have now declined by 17.4% from the peak, led by 25.1% and 22.9% falls across Wellington and Auckland:

Source: Cotality

“Clearly, the falls in mortgage rates we’ve seen lately would point to a bit more upside for property values as we get into 2026, not least because a range of housing affordability measures have also improved back closer to their long-term averages”, noted Cotality NZ Chief Property Economist Kelvin Davidson.

“But the subdued November property value data suggests that this process continues to take a bit of time to get started”.

“On that point, it’s also worth keeping in mind that the stock of listings on the market remains higher than its normal level for the time of year, and many buyers will still be feeling that they’re in the box-seat when it comes to price negotiations”.

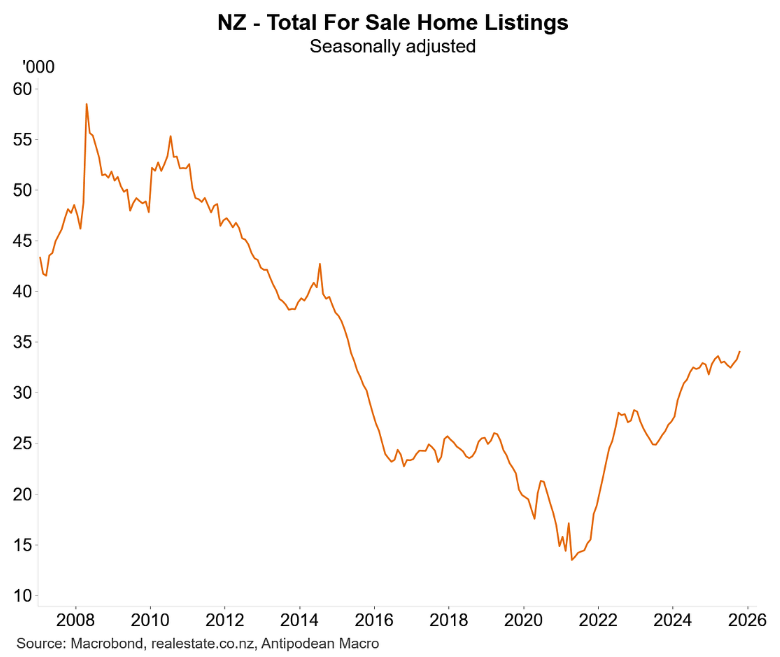

Indeed, as Justin Fabo shows below, for-sale listings in New Zealand are tracking at their highest level in around a decade:

As a result, buyers in New Zealand are spoiled for choice and the ‘fear of missing out’ (FOMO) that traditionally drives price appreciation is nonexistent.

Improving mortgage affordability, stagnating prices, and decade-high for-sale listings are a beautiful set of numbers if you are a prospective homebuyer in New Zealand.