RBA under pressure to hike interest rates

This week’s September quarter national accounts release from the Australian Bureau of Statistics (ABS) was mixed.

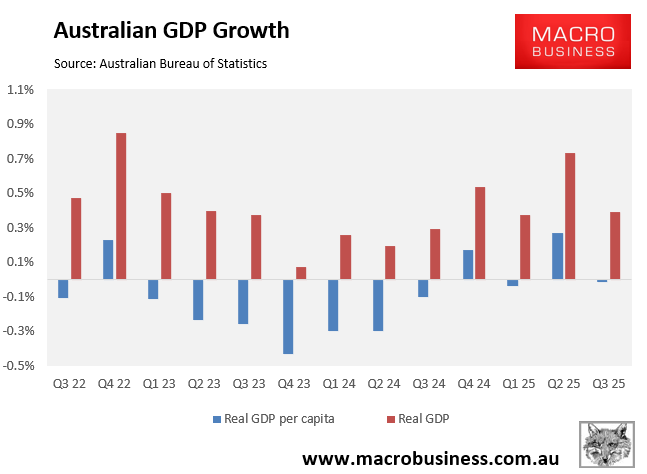

On the one hand, overall GDP growth was soft at 0.4% for the quarter and slightly negative in per capita terms.

On the other hand, annual GDP growth accelerated to 2.1% through the year, in part owing to upward revisions in previous quarters. This meant that annual GDP growth is tracking slightly above the RBA’s expectations.

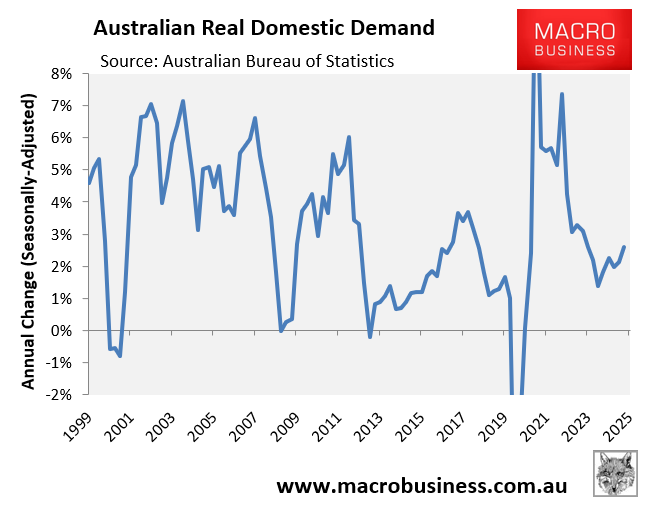

Real domestic demand, which measures the total demand for goods and services within the country (i.e., consumption, investment, and government spending, but excluding net exports), also lifted to 2.6% annually:

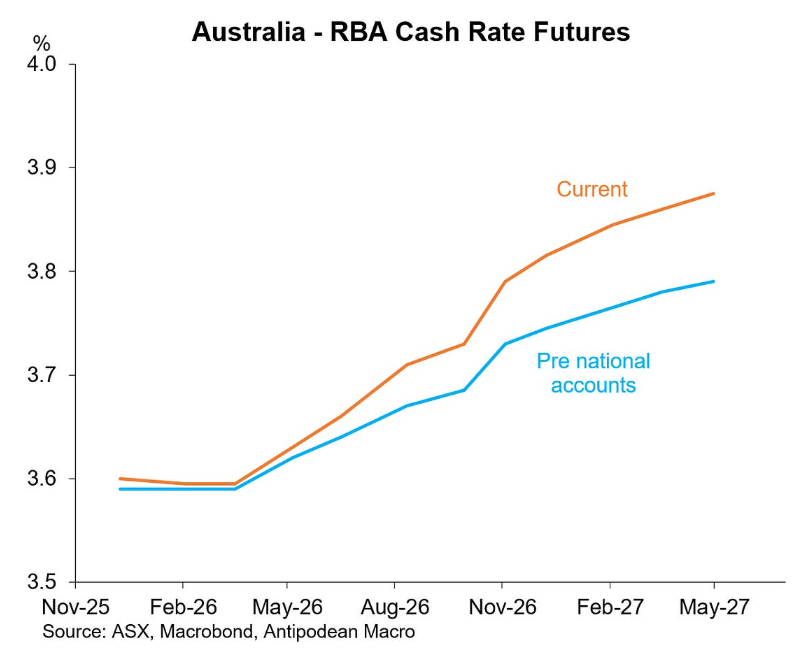

The firming domestic demand was enough to prompt market pricing for the RBA cash rate to shift meaningfully higher, as illustrated below by Justin Fabo from Antipodean Macro:

The financial markets are now firmly tipping the RBA to deliver a 25-bp hike in the cash rate in the first half of 2025.

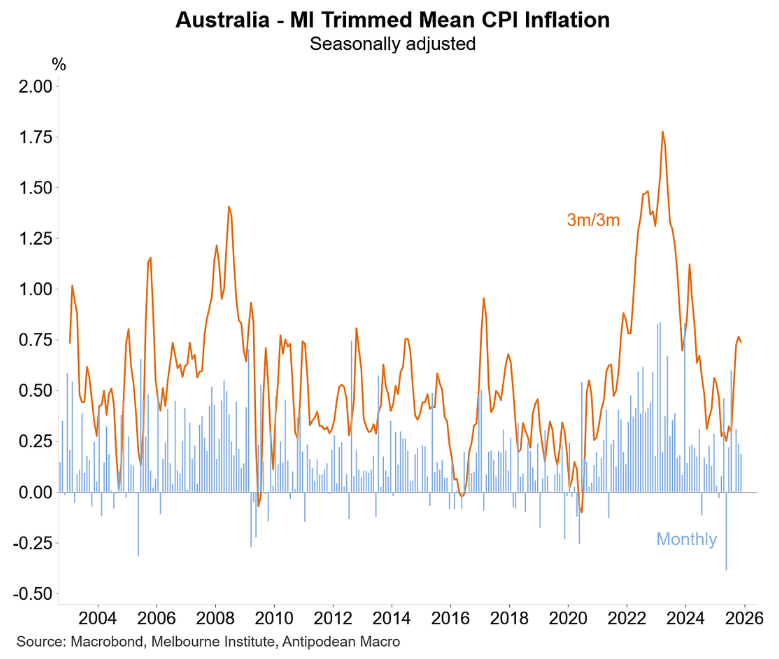

The latest Melbourne Institute trimmed mean inflation gauge supports their view after posting a solid rise in November:

I still believe that RBA is most likely to keep the cash rate on hold for the foreseeable future owing to a likely drift higher in the unemployment rate.

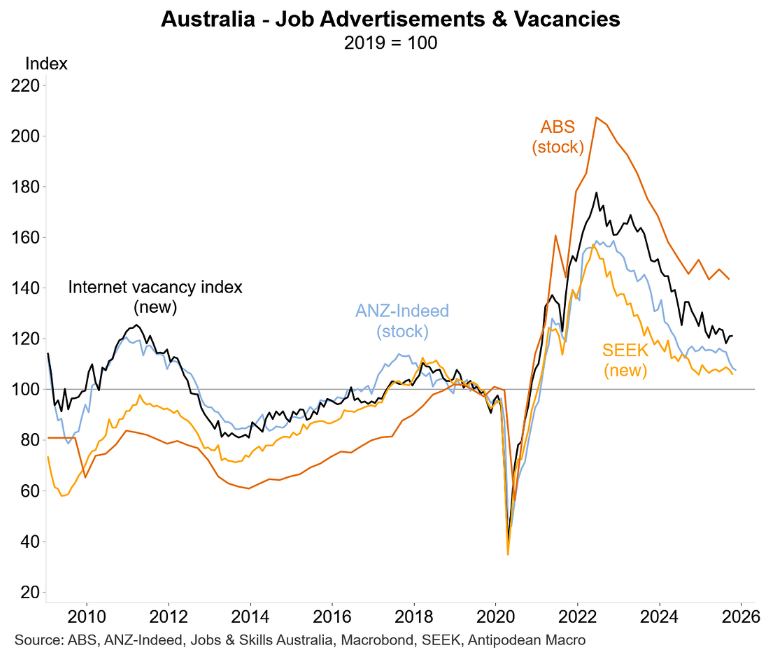

The various measures of job ads/job vacancies have softened:

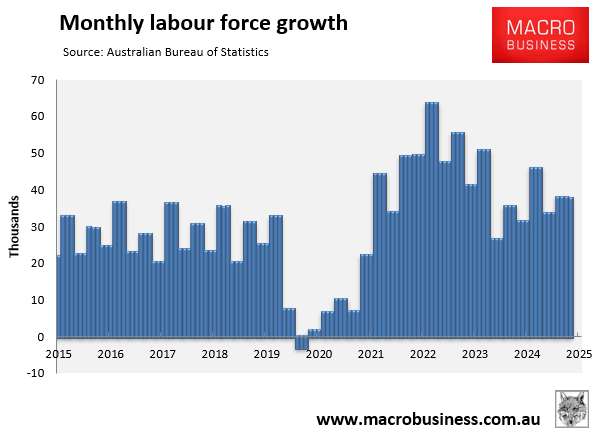

Meanwhile, the labour force is growing at an elevated pace of nearly 40,000 per month, pointing to rising unemployment.

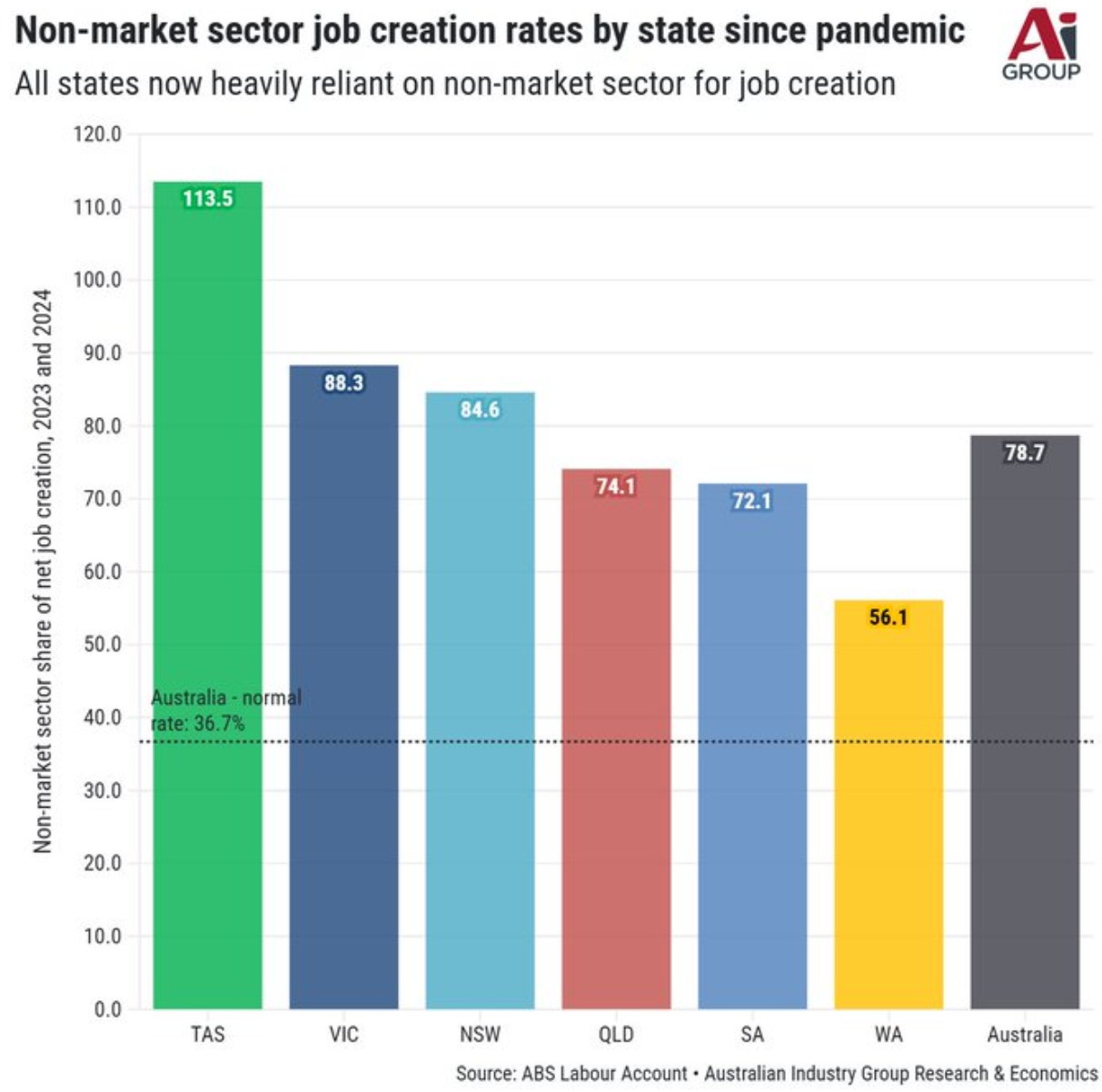

An unsustainable increase in government-funded jobs in the non-market sector, primarily related to the NDIS, has driven the majority of recent job growth in Australia.

The strong tailwind of government-funded job creation could turn into a headwind as the federal and state governments implement cost-cutting measures amid soaring debt.

The RBA has a dual mandate of price stability and full employment. A softening labour market should keep interest rates on hold for the next six months.