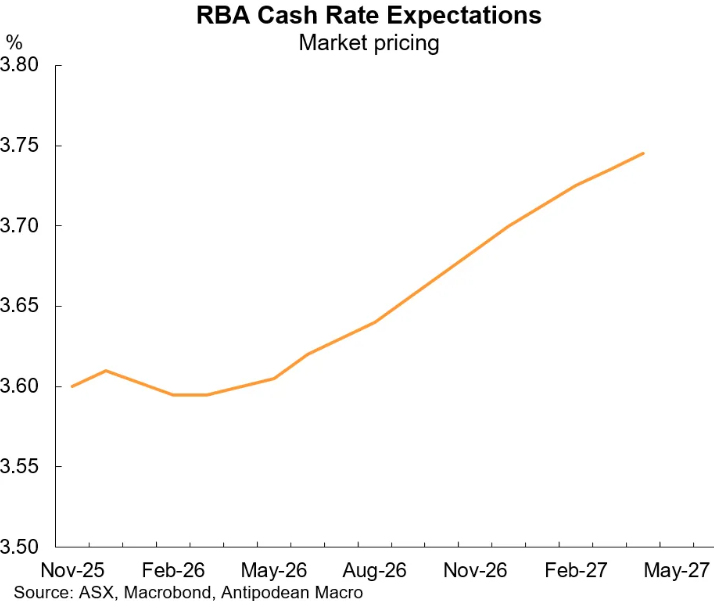

The weather vane of financial market interest rate forecasts has swung hawkish following stronger-than-expected CPI inflation prints.

As illustrated below by Justin Fabo from Antipodean Macro, financial markets are now pricing a potential 25 bp hike in the cash rate in 2026:

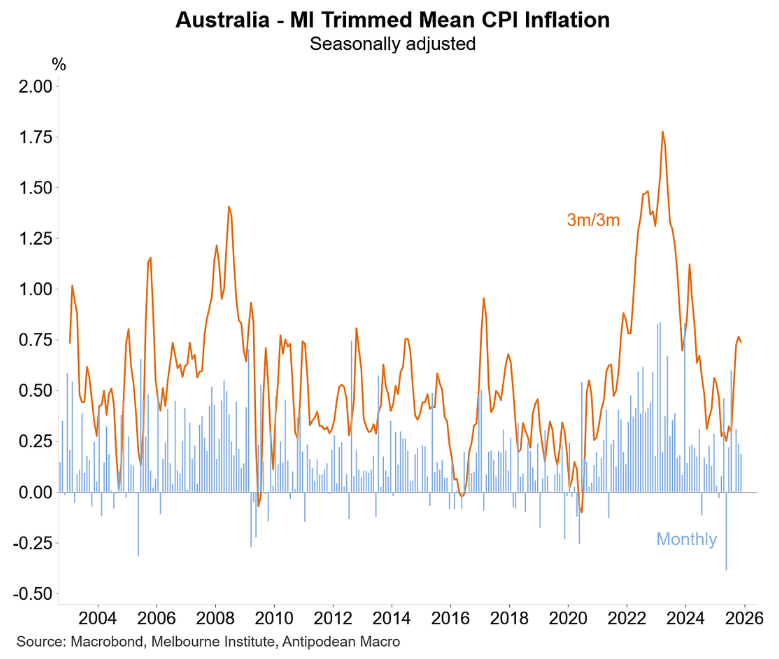

The Melbourne Institute’s trimmed mean inflation gauge, which rose solidly again in November, didn’t help the cause:

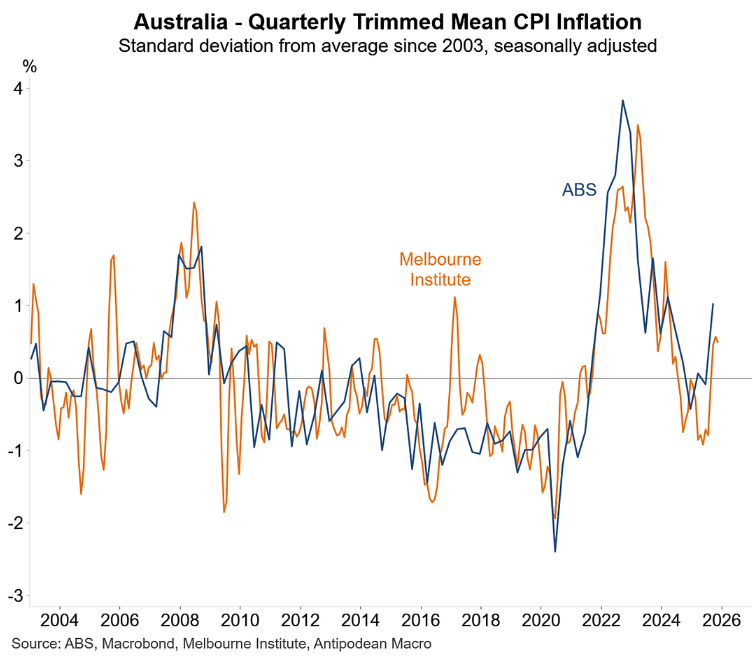

As illustrated by Fabo below, the MI trimmed mean inflation gauge remained above the long-run average in quarterly terms and, alongside the official ABS measure, paints a worrying picture for inflation:

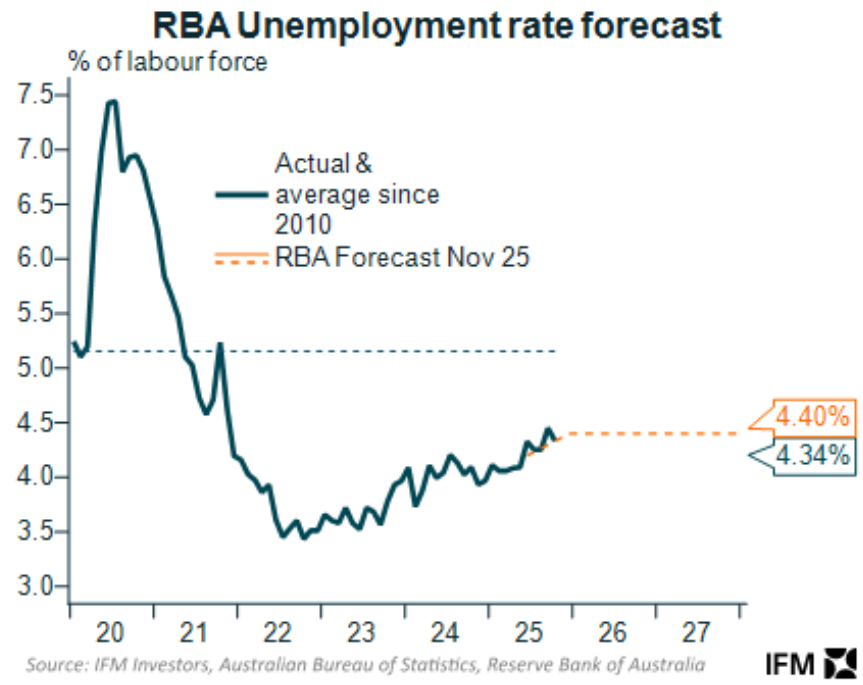

My money remains on interest rates staying on hold for an extended period. I also still believe that the next move in rates is more likely to be down, driven by an increase in the unemployment rate significantly above the RBA’s optimistic forecasts, alongside a moderation of inflation.

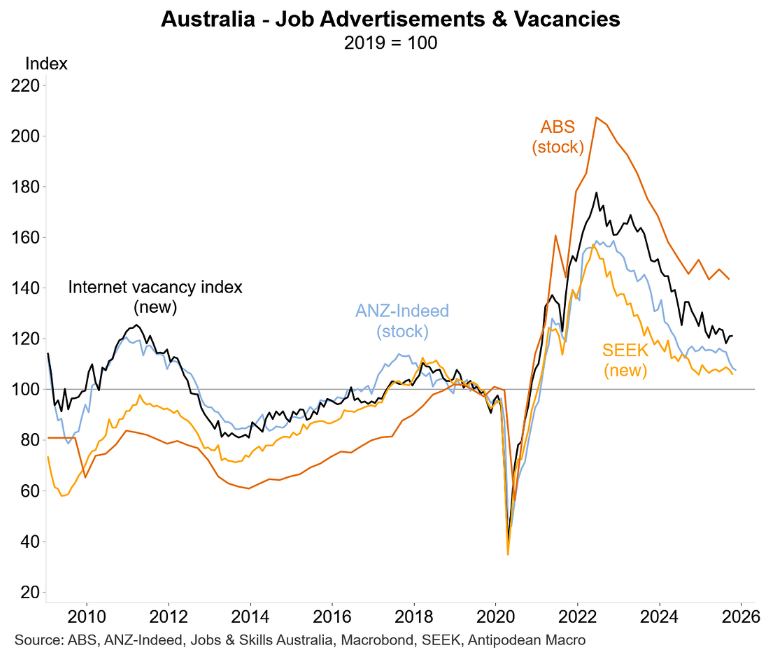

Regarding unemployment, the ANZ-Indeed stock of job ads fell another 0.8% in November, which follows weakness in other job ad/job vacancy indicators:

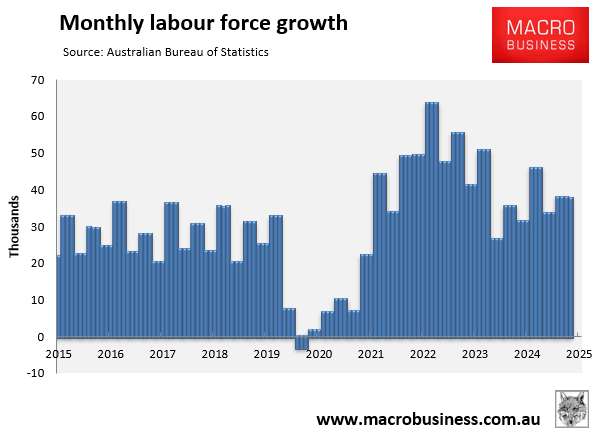

Falling job ads at the same time as the labour force is growing at an elevated pace of nearly 40,000 per month points to rising unemployment.

The RBA is stuck in the unenviable position of being caught between rising unemployment and rising inflation.

As it carefully balances its dual mandate of price stability and full employment, the RBA is facing conflicting pressures on interest rates.