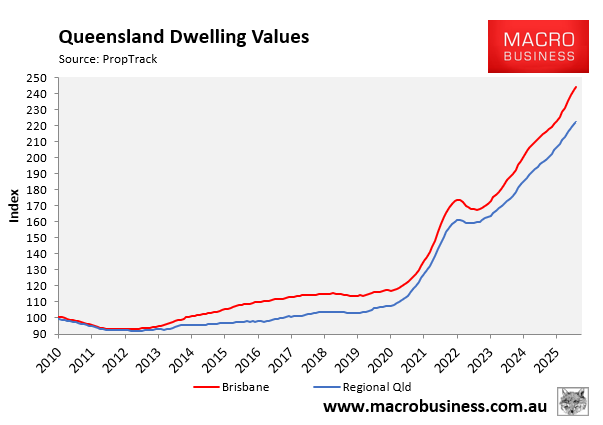

Median dwelling values in Queensland have roughly doubled since the beginning of the Covid-19 pandemic.

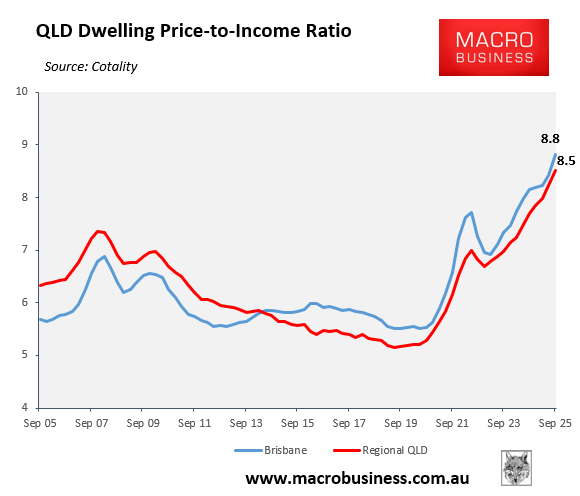

As a result, Queensland’s median dwelling price-to-income ratio soared to 8.8 (Brisbane) and 8.5 (regional Queensland) as of the September quarter of 2025:

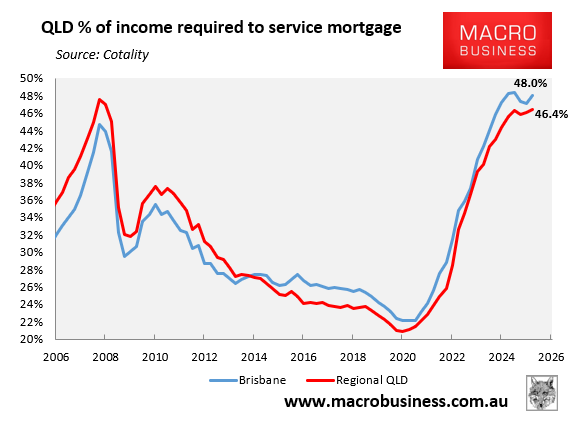

The percentage of median household income required to service a mortgage in Queensland was also tracking at a highly unaffordable 48.0% (Brisbane) and 46.4% (regional Queensland):

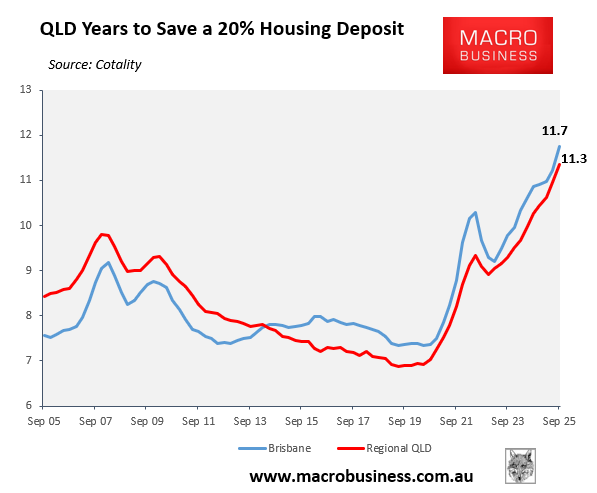

The number of years required for the median-income household to save a 20% housing deposit has risen to 11.7 (Brisbane) and 11.3 (regional Queensland):

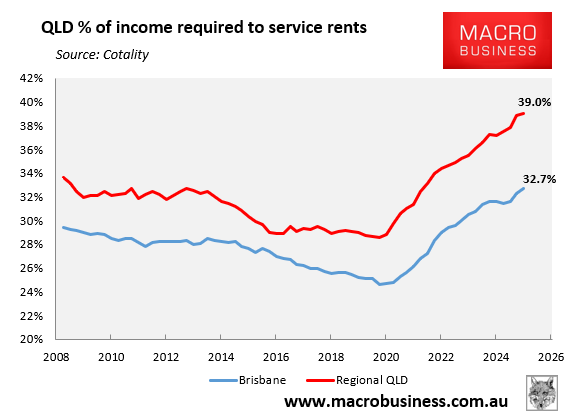

Finally, the percentage of median household income required to service the median advertised rent in Queensland has worsened materially, making it much harder to save up a housing deposit:

The above statistics are obviously terrible news for first home buyers in Queensland, who are facing the worst housing affordability in history.

As a result, state and federal governments have implemented a range of subsidies aimed at making it easier for first home buyers to enter the housing market.

First home buyers in Queensland can access several government assistance programs, including the First Home Owner Grant (up to $30,000), stamp duty concessions and exemptions (full exemption for homes up to $700,000), the federal government’s 5% deposit First Home Guarantee Scheme, the federal government’s Help to Buy shared equity scheme, and the Queensland government’s Boost to Buy shared equity scheme.

These initiatives reduce upfront costs, help with deposits, and make entering the property market easier.

The Queensland state government’s Boost to Buy shared equity scheme was announced in this year’s state budget and is the nation’s most generous shared equity scheme.

Singles earning up to $150,000 and households with two adults earning up to $225,000 were initially eligible for $165 million worth of assistance under the Boost to Buy program, which would see the government invest up to 30% equity in new builds and 25% in existing homes, up to a total of $1 million.

A qualified applicant with a minimum deposit of $15,000 on a $750,000 new property could receive an equity contribution from the state government of up to $225,000.

Over the weekend, the Queensland government announced that it would double the Boost to Buy shared equity scheme to $330 million, meaning up to 2,000 first home buyers can now access the scheme, up from 1,000 previously.

“We are committed to moving Queensland up the home ownership ladder by delivering more Queenslanders a place to call home”, Queensland Treasurer David Janetzkihe said.

“Opening applications for the scheme is a shot of optimism for Queenslanders wanting to purchase their first home, with 50% of places reserved for those wanting to live outside of South East Queensland”.

“Queenslanders shouldn’t be locked-out of buying because they don’t have the bank of mum and dad, so we’re making big changes to deliver a nation-leading Boost to Buy scheme to reduce the deposit gap”, he said.

Like every other demand-side policy, the Queensland government’s Boost to Buy program is self-defeating from a housing affordability perspective.

Ultimately, it will drive values higher, reducing the structural affordability of housing.

Throughout this century we have witnessed the impacts of these policies, with first-home buyer grants, shared equity schemes, and other subsidies capitalised into higher home values and larger mortgages.

Introducing more demand-side “affordability” measures and expecting a different result is the definition of policy insanity.

Welcome to 21st-century Australia, where inflating home prices and mortgage debt is the national sport.