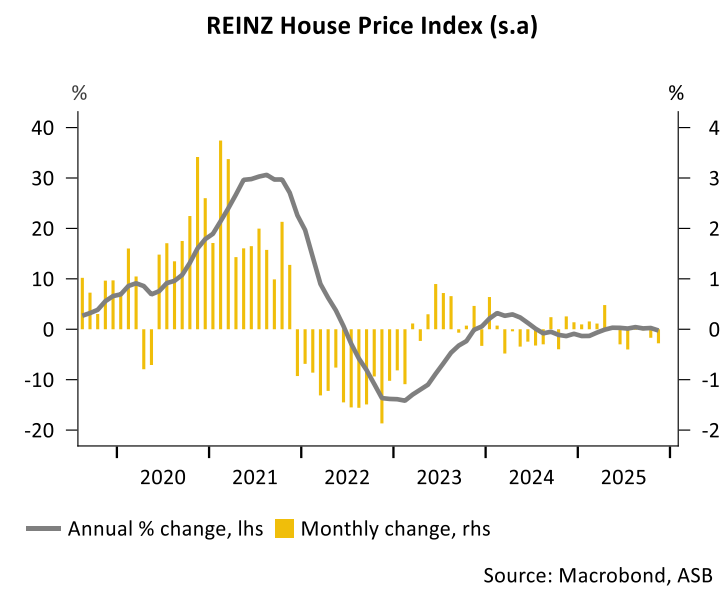

New Zealand house prices continue to fall.

The REINZ House Price Index fell 0.3% over the past two months (seasonally adjusted), with economists describing the result as “renewed weakness” after a brief stabilisation earlier in the year.

Compared to May, house prices are down by more than 1.2%.

Home sales were weak in November, declining by 4.8%. November also marked the first notable annual decrease in sales volumes since June 2024, falling 5.7% from a year ago.

ANZ economists noted that sales volumes have slipped below long‑run seasonal averages and that the usual spring rebound failed to materialise.

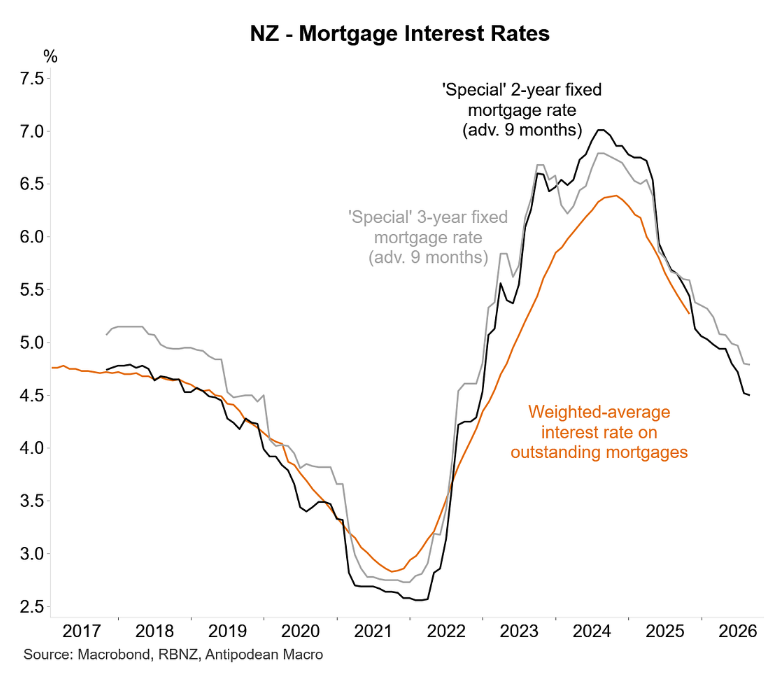

The ongoing weakness in housing demand has come despite lower mortgage rates, illustrated below by Justin Fabo from Antipodean Macro, following 325 basis points of official cash rate (OCR) cuts from the Reserve Bank.

Meanwhile, the supply side of the market continues to strengthen, with new listings creeping up for the third consecutive month and the stock overhang remaining at a decade high.

Thus, the weak labour market and slow population growth remain the key factors constraining any improvement in demand, whereas the supply of housing remains high and continues to exceed demand.

In pure dollar terms (i.e., not inflation‑adjusted), home prices are tracking 15% below the 2021 peak.

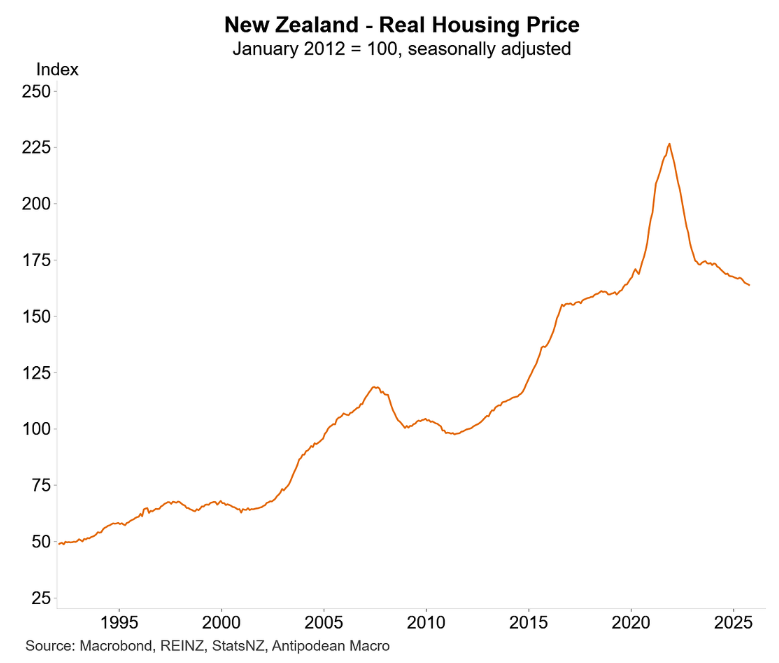

However, home prices have fallen dramatically when adjusted for inflation, with real values now down 31.3% from their late‑2021 peak. This decline marks the deepest real‑terms corrections in modern New Zealand housing history.

Despite 325 basis points of OCR cuts, both home prices and sales turnover remain lower than a year ago.

Economists warned of further downside risks as interest rates potentially rise in 2026 and sales volumes fall.

Wholesale interest rates have risen following the November Monetary Policy Statement, while confidence has fallen alongside sales volumes.