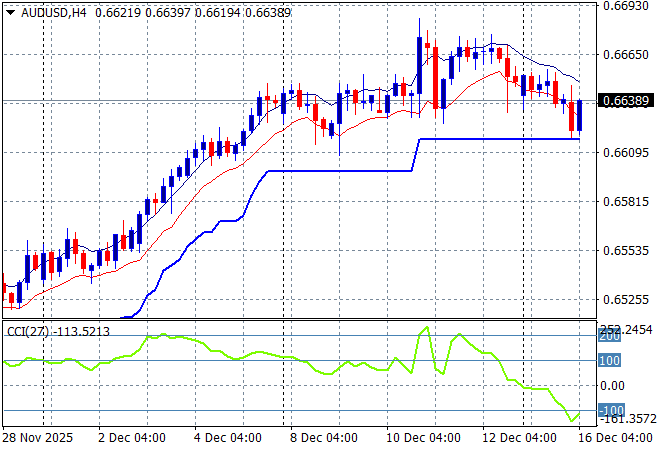

A sea of red across Asian share markets with the rough start to the trading week continuing as a wider risk off tone deepens, all mainly due to tech stock volatility. The absence of bad economic news is not helping as markets start to pivot to the series of central bank meetings and tonight’s double whammy US NFP print with mixed moves across the currency markets, with Yen again strengthening against USD while the while the Australian dollar is slightly weaker but holding its own above the 66 cent level.

Oil markets remain unstable with Brent crude drifting below the $61USD per barrel level while gold was trying to firm above the $4300USD per ounce level but has recently lost upside momentum for small pullback:

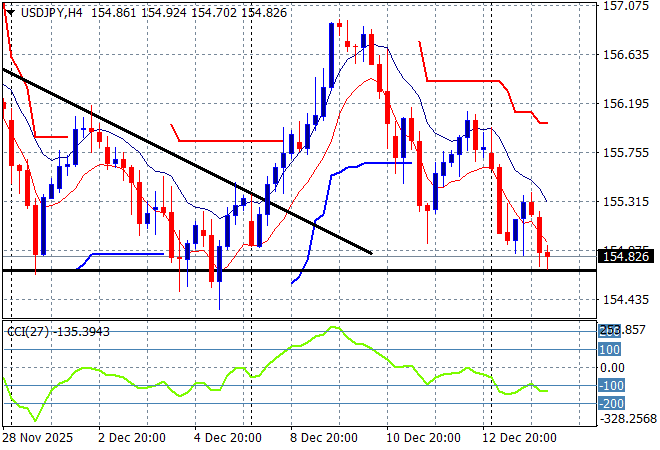

Mainland Chinese share markets are seeing stronger selling in afternoon trade with the Shanghai Composite down more than 1.3% to almost cross the 3800 point level while the Hang Seng Index has also accelerated its recent falls with a near 2% drop to well below the 26000 point level. Japanese stock markets are also seeing a solid selloff with the Nikkei 225 down more than 1.3% at 49515 points with the USDPY pair now crossing below the 155 level:

Australian stocks fell back in afternoon trade as the Santa Rally was stopped in its tracks with the ASX200 losing 0.4% to 8598 points while the Australian dollar has stabilised after a small pullback overnight to remain above short term support but just below the mid 66 cent level against USD:

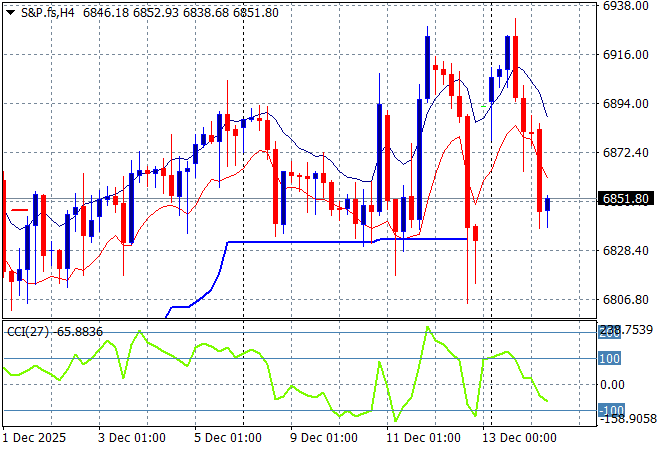

S&P and Eurostoxx futures are struggling to find a bottom here after recent volatility with the S&P500 four hourly chart showing support at the 6800 key level the area to watch in coming sessions:

The economic calendar includes the October and November non farm payrolls data from the US and a slew of flash PMI prints on both sides of the Atlantic.