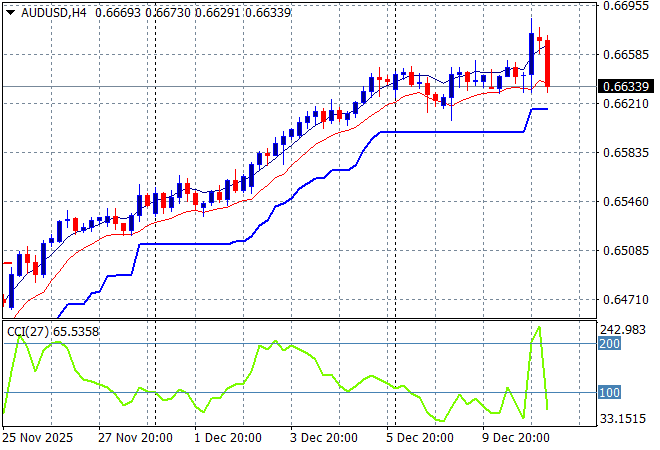

Its not been all roses and sunshine following last night’s rate cut by the Fed with Asian share markets mixed at best while commodity and currency markets are moving into risk off mode on the escalation in the Caribbean by the Trump regime’s seizure of an oil tanker and some questioning around AI spending via Oracle’s post close earnings. The Australian dollar gave up all its recent gains on the very mixed jobs report locally with the potential for a rate hike in February dwindling as it flops down to the low 66 cent level.

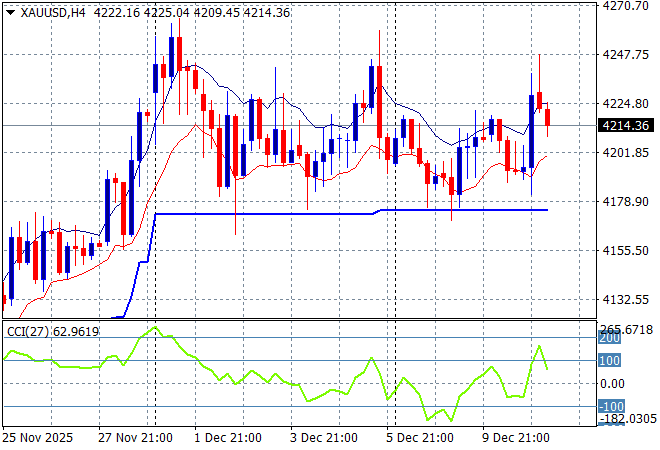

Oil markets remain unstable with Brent crude drifting down to the $62USD per barrel level while gold is still hanging around the $4200USD per ounce level but still has little upside momentum:

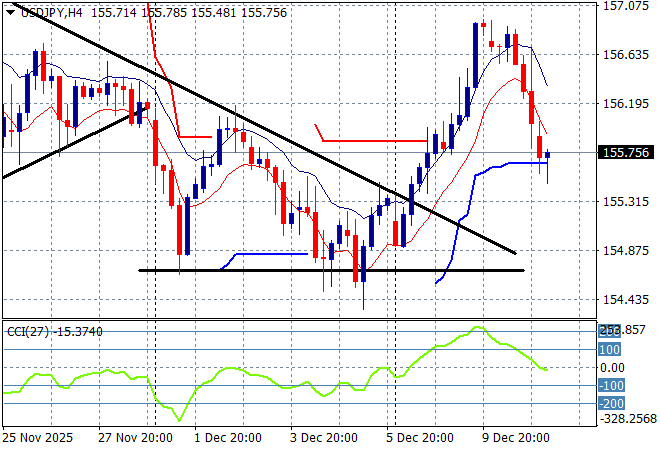

Mainland Chinese share markets are seeing sharp selling with the Shanghai Composite down more than 0.5% to stay below the 3900 point level while the Hang Seng Index has stabilised a little more with a small lift up to 25563 points. Japanese stock markets are also seeing a solid selloff with the Nikkei 225 losing 0.8% at 50170 points with the USDPY pair stalling out at the mid 155 level after a big post rate cut decline overnight:

Australian stocks are still processing the RBA positioning and the latest jobs print with the ASX200 gaining 0.1% or so at 8595 points while the Australian dollar has returned to its pre Fed meeting level at just above the 66 cent level against USD:

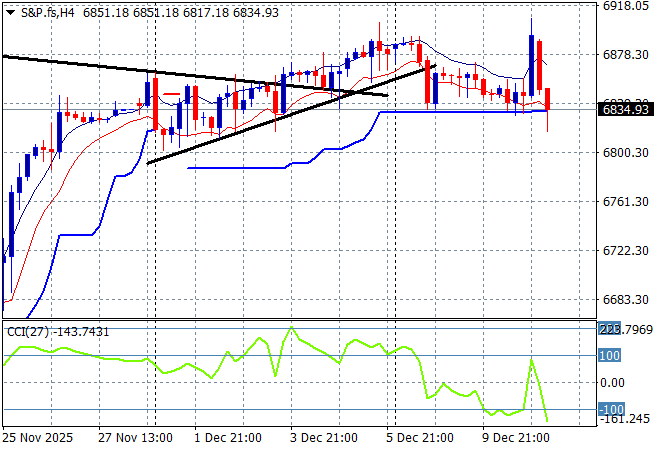

S&P and Eurostoxx futures are pulling back sharply with the S&P500 four hourly chart showing how last night’s breakout on the Fed rate cut might be wiped out already in tonight’s session due to the Trump piracy actions:

The economic calendar includes the latest US initial jobless claims then quite a few Treasury auctions.