The new prudential standard announced last month by the Australian Prudential Regulatory Authority (APRA) caps high-risk mortgages (i.e., with a debt-to-income ratio greater than 6x) at 20% of new lending, effective from February 2026.

In line with government objectives to increase affordability through supply incentives, APRA’s policy does not apply to newly constructed homes. It also applies portfolio-wide, giving banks flexibility.

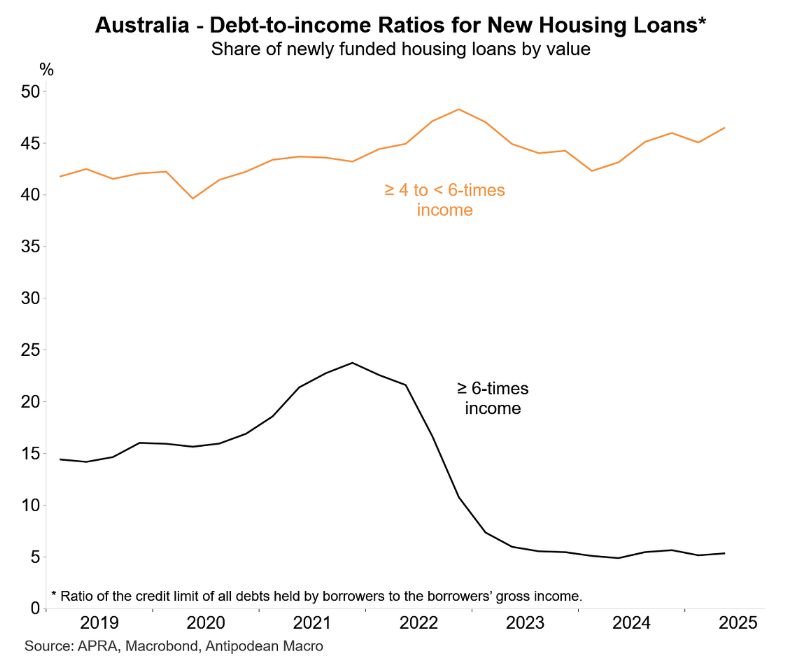

Just over 6% of existing loans surpass this level, as Justin Fabo from Antipodean Macro shows below. Therefore, high DTI exposures could triple before exceeding the 20% cap.

As a result, critics have labelled APRA’s action a symbolic move that has essentially approved over three times as many high DTI loans as the market now has.

This strategy, therefore, seems aimed at making it appear like APRA is “doing something” about rising mortgage risks, even though it is only doing the bare minimum.

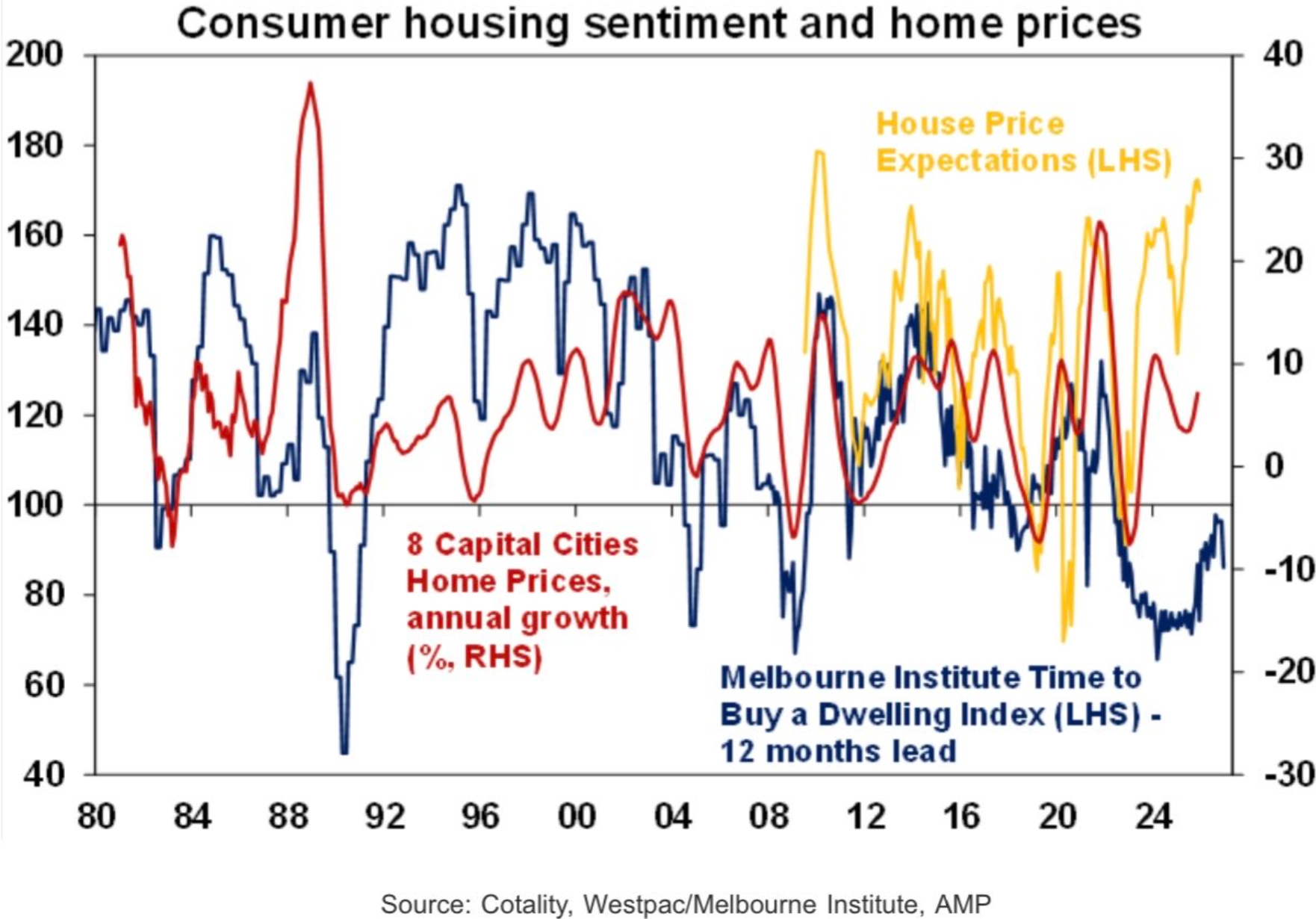

The announcement by APRA came as house price expectations are tracking at historical highs, according to Westpac’s consumer sentiment survey:

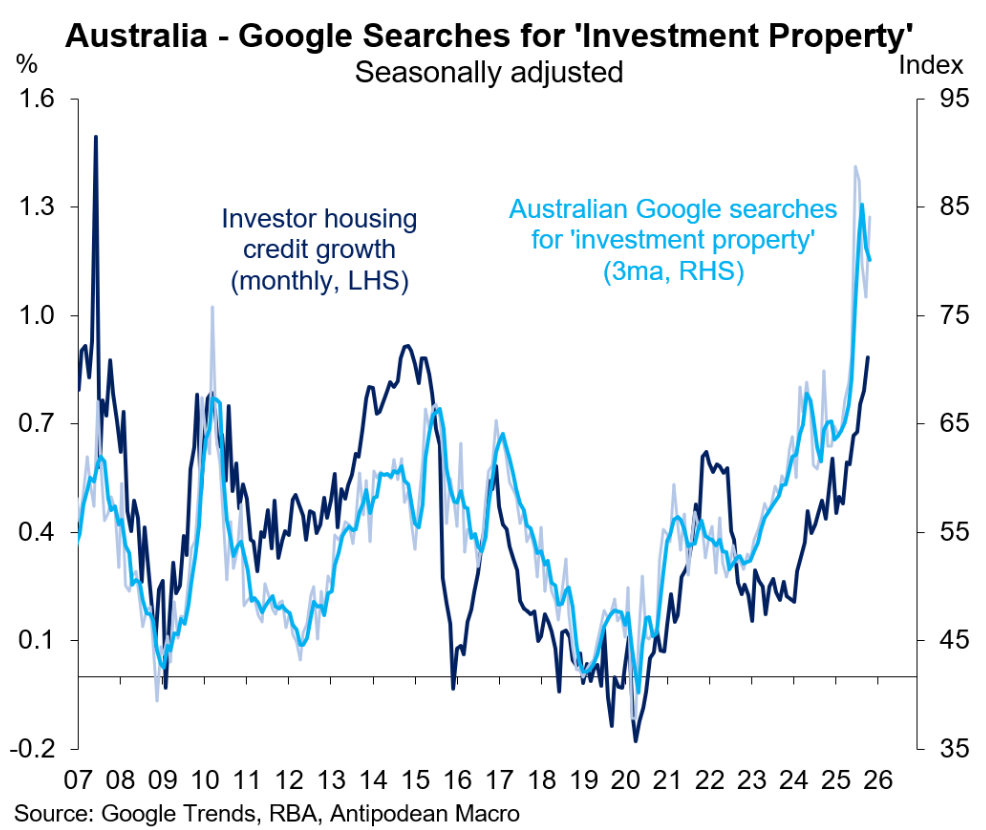

Fabo also showed that Google searches for “investment property” are tracking at historical highs:

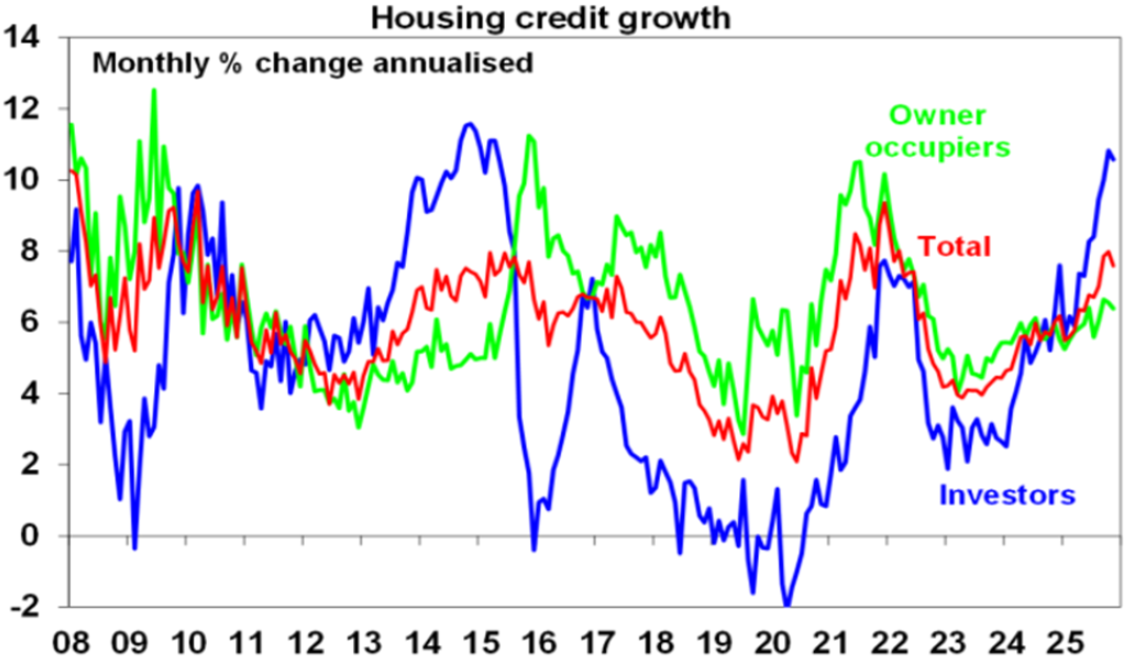

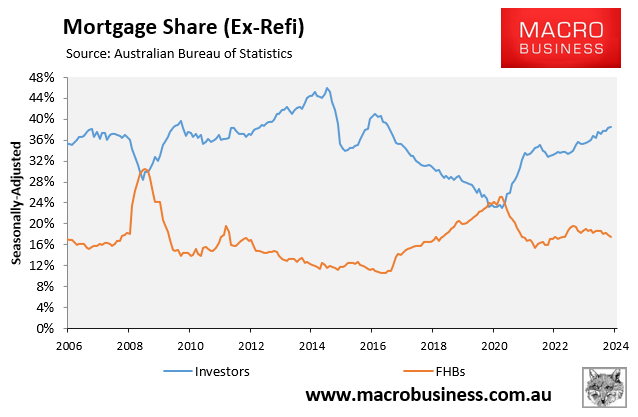

Friday’s mortgage credit data from the Reserve Bank of Australia (RBA) showed that investors are piling into the housing market, tracking at close to its highest level in a decade:

Source: Shane Oliver (AMP)

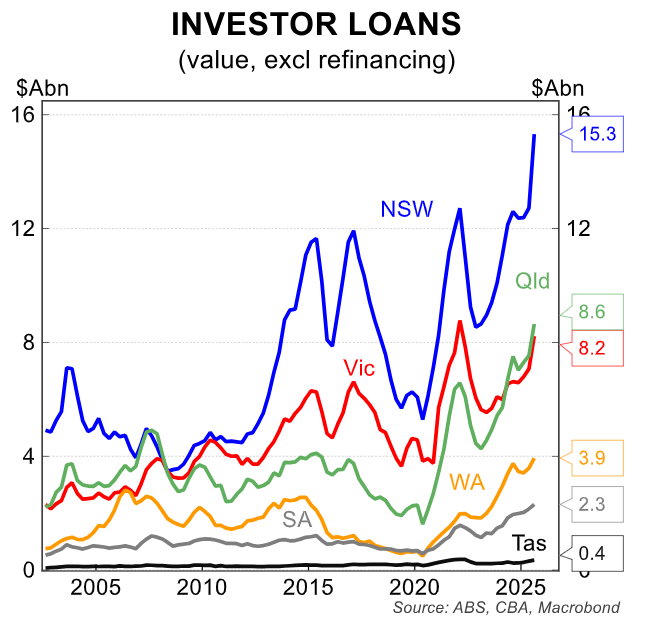

Investor mortgage commitments are also tracking at record highs everywhere except for Victoria:

A decade ago, when investor demand was last this high, Australia’s financial regulators tightened the screws.

Between 2014 and 2018, APRA implemented macroprudential policies to halt the expansion of investor mortgages. These included tougher serviceability requirements to lower risky borrowing, restrictions on interest-only loans, and growth limits on investor lending.

Consequently, after 2015, the growth of investor mortgages slowed considerably. Additionally, the proportion of new loans that were interest-only fell from about 40% in 2015 to less than 20% in 2018.

Why hasn’t APRA acted more forcefully to reduce investor demand this time?

Is the Albanese government keeping APRA on a tight leash to prevent the introduction of regulations that could hinder the housing boom?

The easiest way to increase the number of first home buyers entering the market is to decrease investor demand.

Reducing investor demand is a far superior policy to Labor’s 5% deposit scheme for first home buyers, which merely raises prices and debt.