It was MB that led APRA to adopt macroprudential tools designed to lean against the cycle and aid monetary policy.

Alas, like everything else in the Australian political economy these days, APRA’s latest round of macroprudential tightening is purely performative, or fake, achieving the opposite.

Back in the 2015 lending bubble, MB forced AHPRA to apply a 10% speed limit on investor mortgages, leading to good results as it plummeted.

After a brief rebound, the Banking Royal Commission then thumped it again.

Let’s compare that with APRA fake effort today.

Investor lending is now at 7.25% year-on-year but is accelerating rapidly, with the quarterly annualised rate at 10%.

Now is an ideal time to apply more speed limits, but instead, we got not just the wet lettuce but the green light.

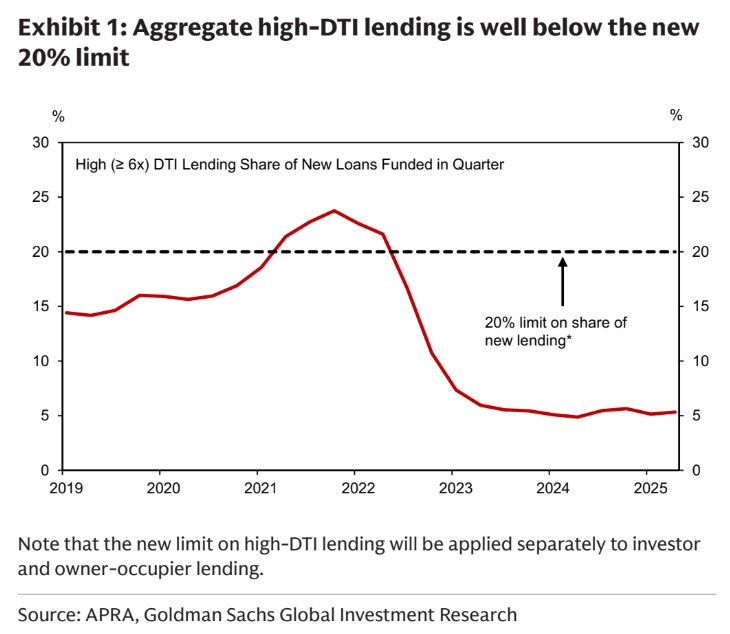

From 1 February next year, the limit on home loans will allow authorised deposit-taking institutions (ADIs) to lend up to 20 per cent of their new mortgage lending at debt of six times income or more. The limit will apply separately to ADIs’ owner-occupier and investor lending.

At an aggregate level the limit is not currently binding, so it is not expected to have a near-term impact on borrowers’ access to credit. Only a small number of ADIs are expected to be near the limit for high DTI investor lending at this stage. Should levels of high DTI lending rise towards the 20 per cent limit over the coming period, this limit will act as a guardrail and is expected to have a greater impact on investors, who typically borrow at higher DTI ratios than owner-occupiers.

So, it is not a speed limit at all. But a future speed limit. That is, permission to go nuts. Goldman assesses it thus.

We do not expect the new limits to have a material impact on new residential lending, given the currently very low share (5%) of high-DTI lending.

Only in Straya.