My latest podcast with Martin North at Digital Finance Analytics (DFA) explained why now is a particularly risky time to be utilising the federal government’s 5% deposit scheme for first home buyers, given that the market is so expensive and risks following Canada and New Zealand with a severe housing correction.

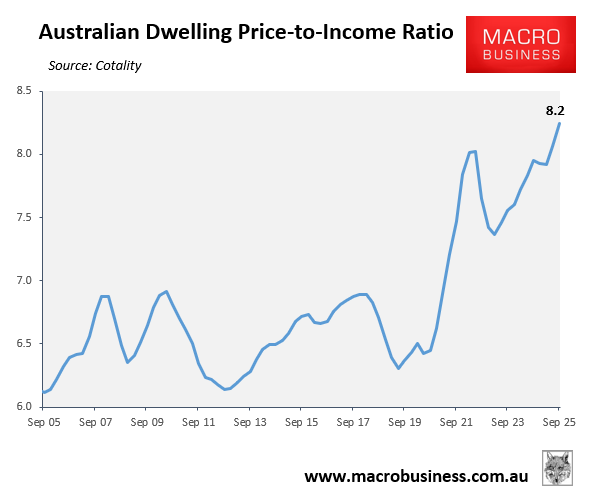

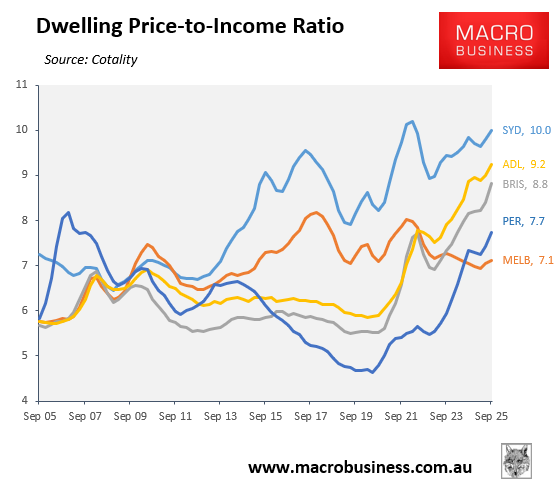

The long and short of it is that Australia’s dwelling value-to-income ratio was tracking at a record high of 8.2 in the September quarter of 2025, according to Cotality.

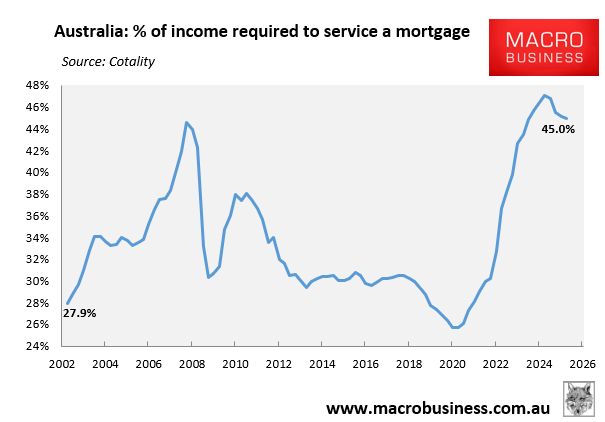

The percentage of median household income required to service a new mortgage on the median-priced home was also historically high, at 45.0%, despite three 25-bp rate cuts from the RBA.

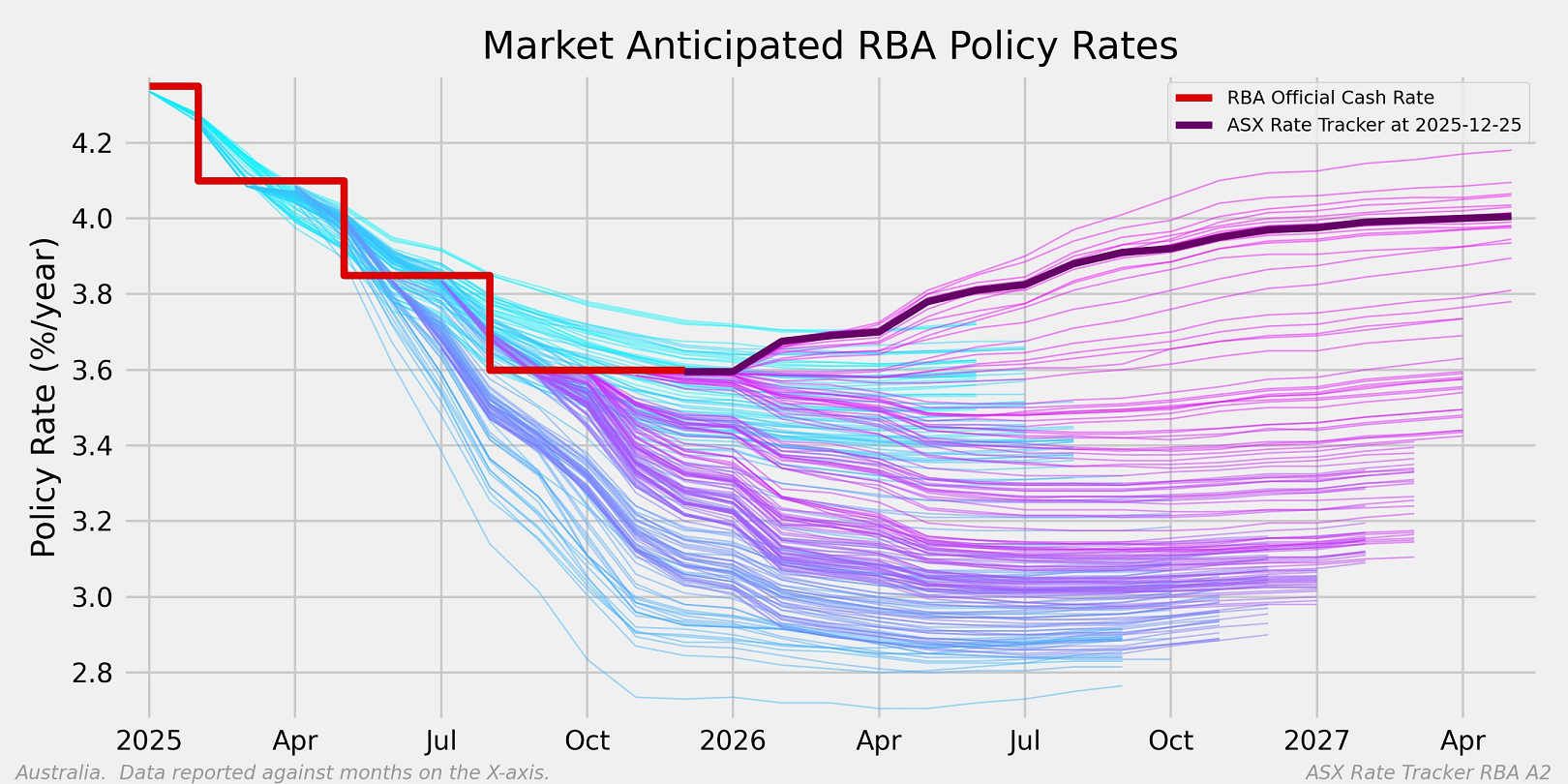

Now most economists and financial markets are tipping two 25-bp rate hikes in 2026.

Chart by Mark Graph

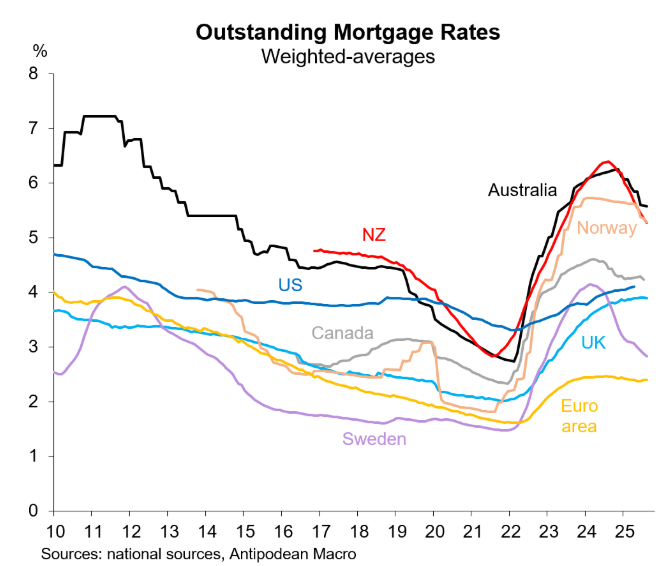

Such an increase would take the official cash rate above 4% and average mortgage rates to near 6%—the highest in the world.

Chart by Justin Fabo at Antipodean Macro

The risk is that the rise in reduced mortgage affordability and borrowing capacity will cut demand, resulting in a house price correction.

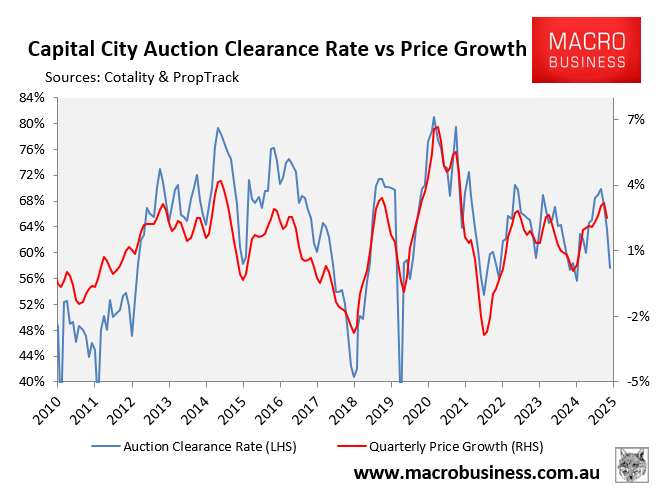

The market appears to be cooling down already, as auction clearance rates are sharply declining and price growth is slowing down.

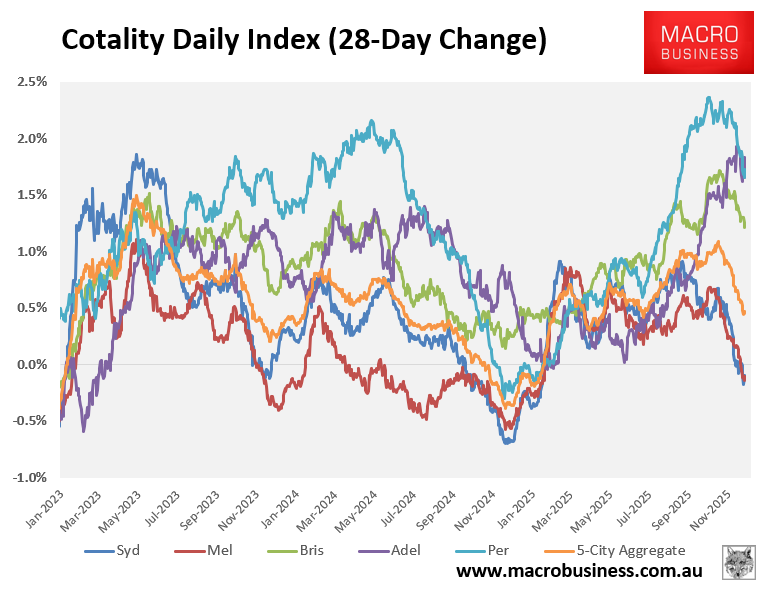

Cotality’s daily dwelling values index has slowed markedly over the past 28 days, led by price declines across Sydney and Melbourne.

While some of this decline in auction clearances and price growth is seasonal, it also reflects a clear deceleration of buyer demand amid expectations of rising future interest rates.

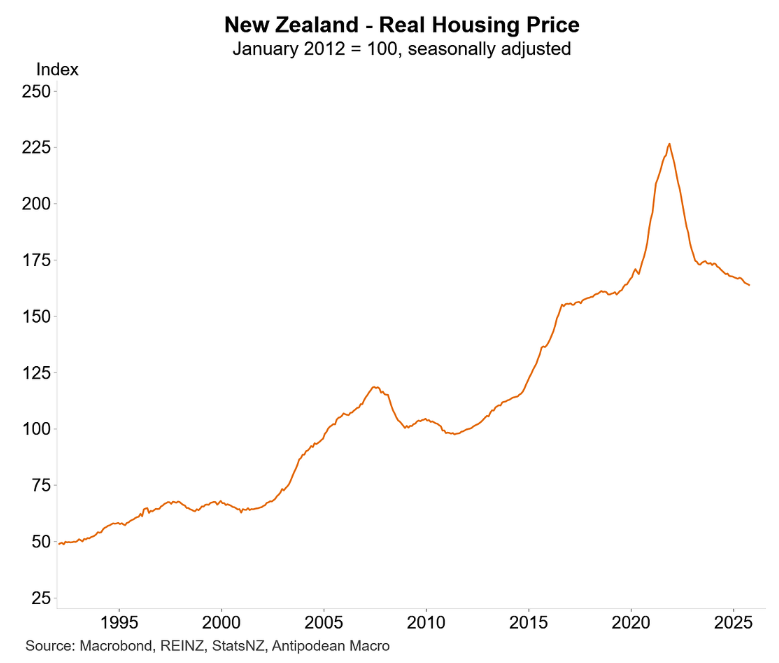

The clear risk for Australian housing is that it could follow New Zealand and Canada—arguably Australia’s most similar economies and housing markets—with a deep housing correction.

New Zealand has experienced its largest house price crash in modern history, with values nationally down 15% below the 2021 peak in nominal terms and down 31.3% from their peak in real inflation-adjusted terms:

Chart by Justin Fabo at Antipodean Macro

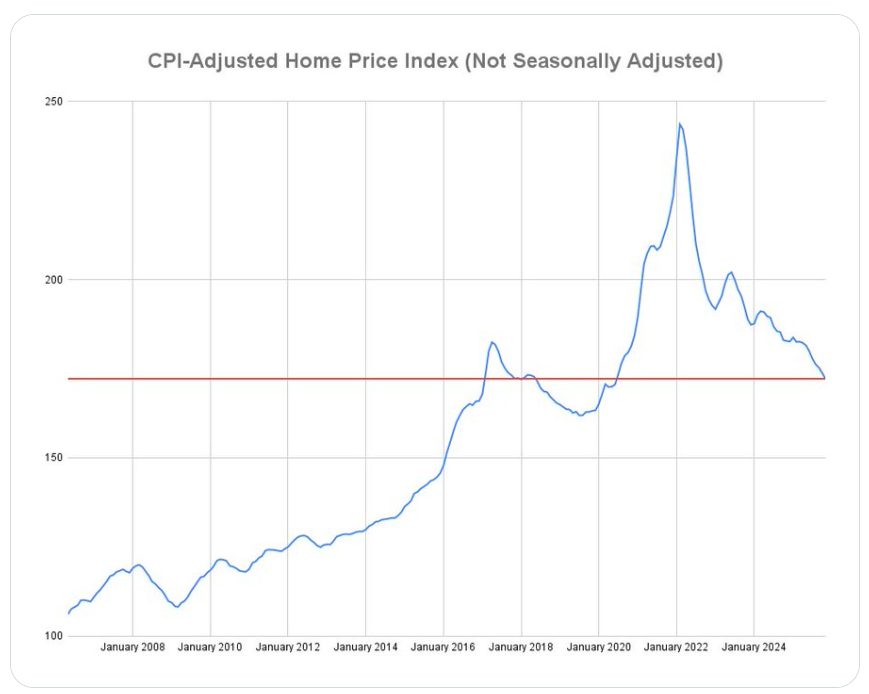

Canada’s home values have fallen back to where they were in February 2017 in real inflation-adjusted terms:

Real Canadian home prices

If Australia’s two most similar housing markets can experience severe house price corrections, why couldn’t Australia?

The bottom line is that it is an incredibly risky time to be leveraging into Australian property with a tiny deposit.

The only caveat to this view is Melbourne, which has experienced minimal price growth since the pandemic and affordability has markedly improved.

Melbourne’s relative affordability makes it far less risky than the other major capital city markets.