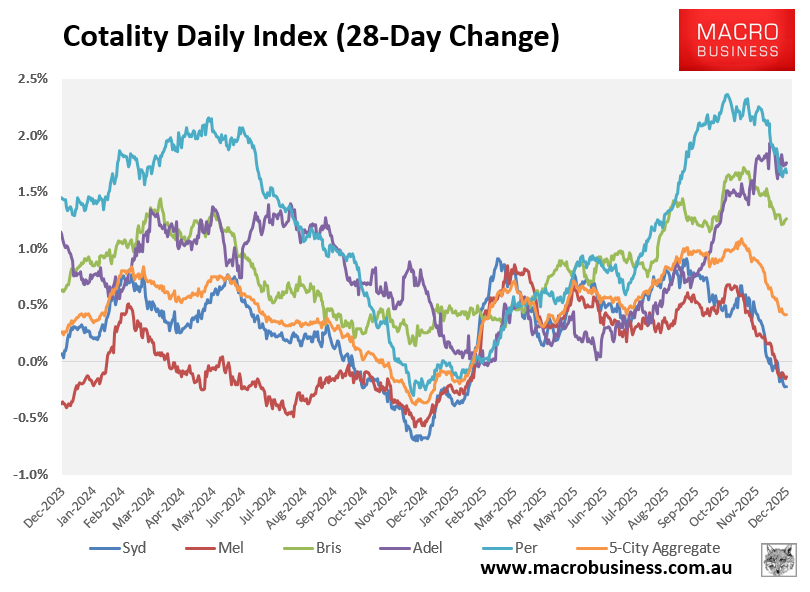

Cotality’s daily dwelling values index, which tracks home values across Australia’s five major capital city markets, has ended 2025 with momentum stalling.

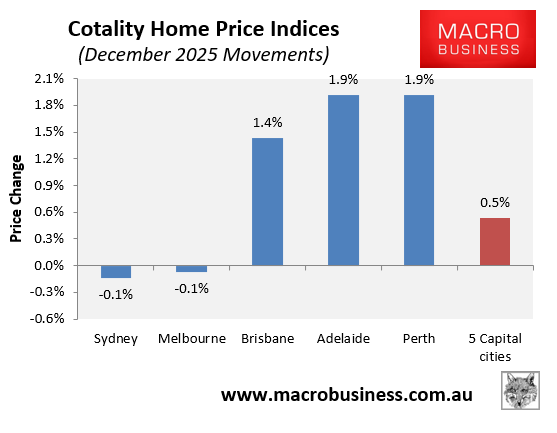

At the aggregate 5-city level, Cotality’s daily dwelling values index rose 0.5%, down significantly from the 1.0% growth recorded in November.

As illustrated above, there was wide divergence between the major capital city markets.

Sydney and Melbourne recorded value declines of 0.1% in December, whereas Brisbane (1.4%), Adelaide (1.9%), and Perth (1.9%) recorded strong growth.

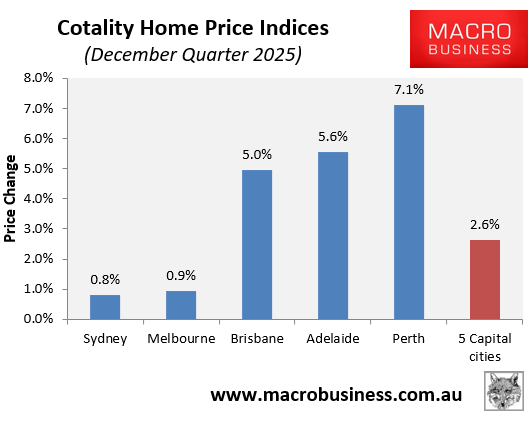

The situation was similar over the December quarter, with Sydney (0.8%) and Melbourne (0.9%) recording soft growth, whereas Brisbane (5.0%), Adelaide (5.6%), and Perth (7.1%) recorded turbo-charged growth:

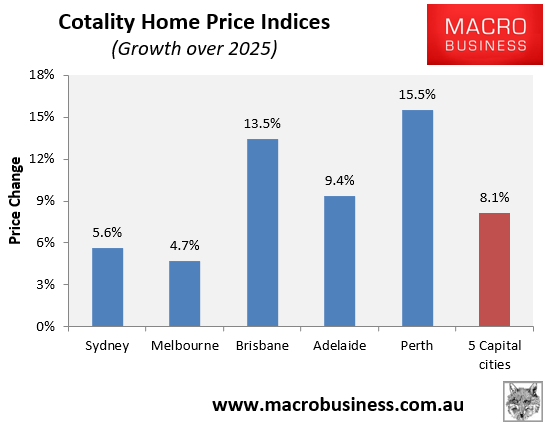

Over the 2025 calendar year, Cotality’s daily dwelling values index increased by 8.1% at the combined 5-city level.

Again, Sydney (5.6%) and Melbourne (4.7%) underperformed, whereas Brisbane (13.5%), Adelaide (9.4%), and Perth (15.5%) recorded strong growth:

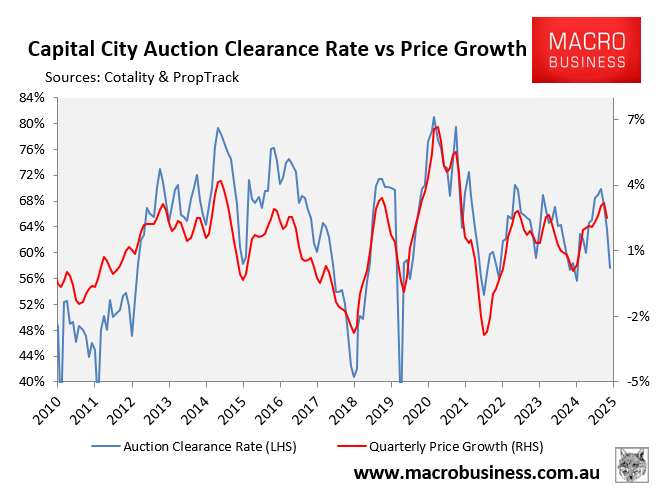

The softness has also been reflected in the auction market, which is heavily dominated by Melbourne and Sydney, where clearance rates collapsed during the final months of 2025.

The weakness shown across Sydney and Melbourne, and the relative strength elsewhere, reflects the differing supply-demand dynamics across those markets.

As illustrated below by CBA, listings across Sydney and Melbourne are tracking above the five-year average, whereas they are tracking well below the five-year average across the other major markets:

That said, all major markets aside from Adelaide have experienced a deceleration of price growth in recent months:

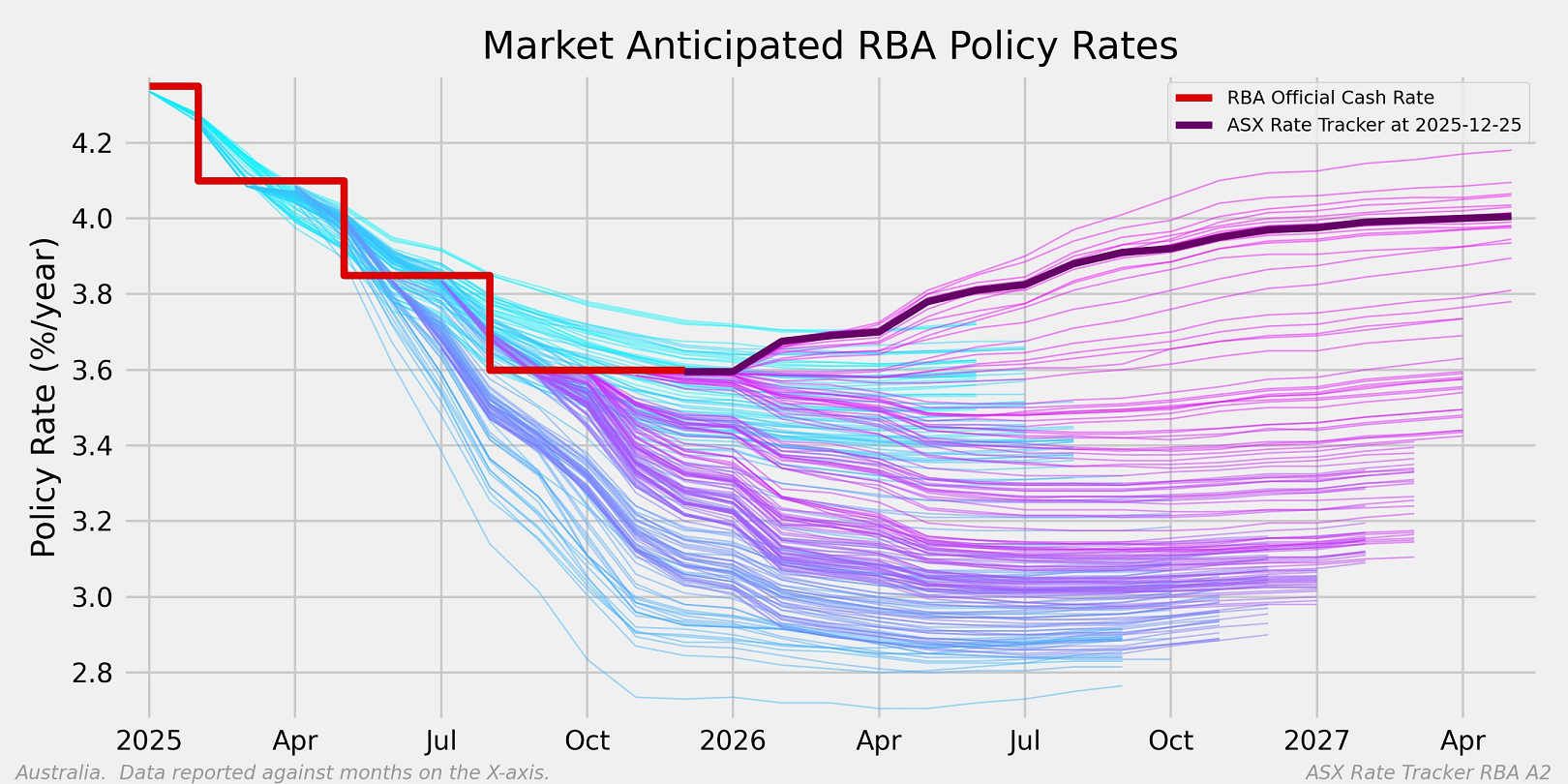

The broader deceleration in dwelling value growth at the end of 2025, driven by Sydney and Melbourne, reflects shifting expectations about interest rates.

Source: Mark Graph

Economists and financial markets have gone from expecting two further rate cuts three months ago to anticipating two rate hikes in 2026.

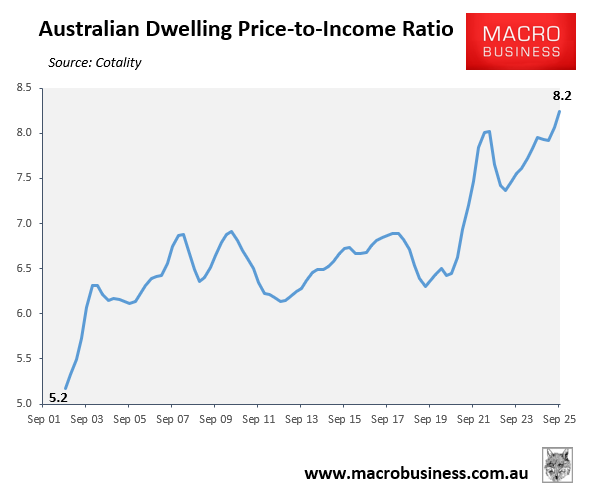

Given the record-low affordability of Australian housing, buyers require further rate cuts to increase borrowing capacity, improve mortgage affordability, and lift prices.

Ultimately, without further Reserve Bank rate cuts, dwelling value growth is likely to slow in 2026.