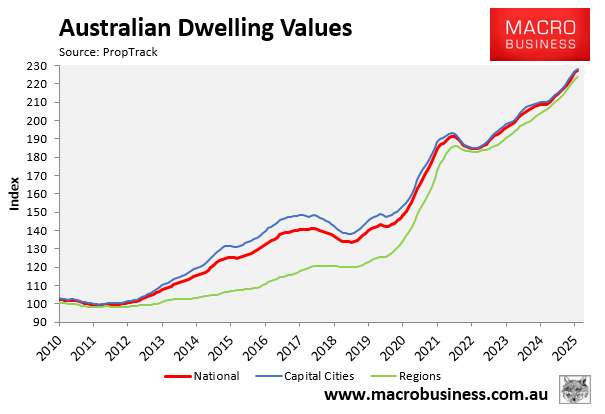

Australian dwelling values marched higher in October, hitting a record high $979,000 median value across the combined capital cities, according to PropTrack.

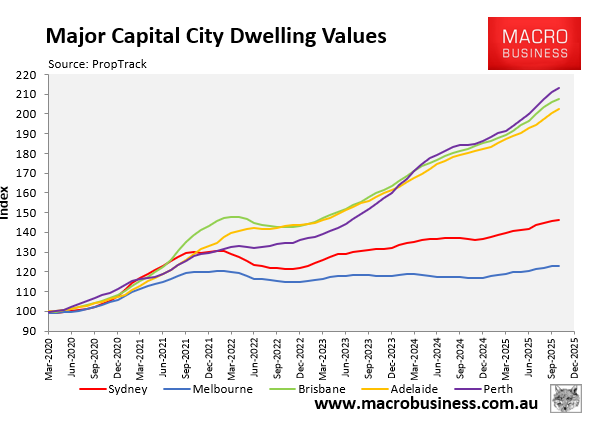

Since the beginning of the Covid-19 pandemic in March 2020, Australian dwelling values have surged in value by 59%, led by explosive growth across Brisbane, Perth, and Adelaide where prices have roughly doubled.

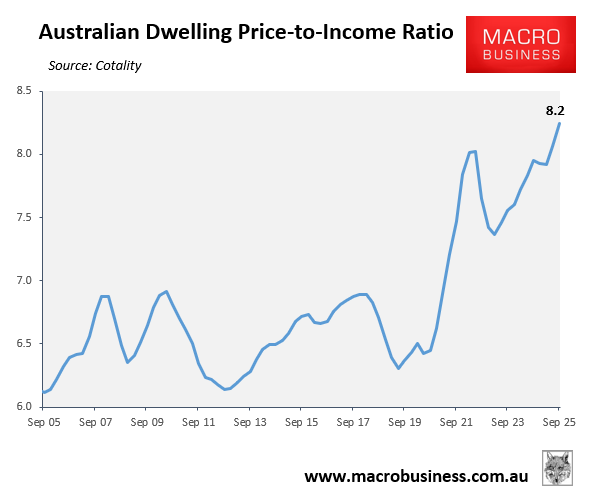

Cotality’s latest housing affordability report showed that the explosive price growth since the pandemic has driven the national dwelling price-to-income rate to a record high of 8.2 as of Q3 2025, up from 6.5 at the beginning of the pandemic:

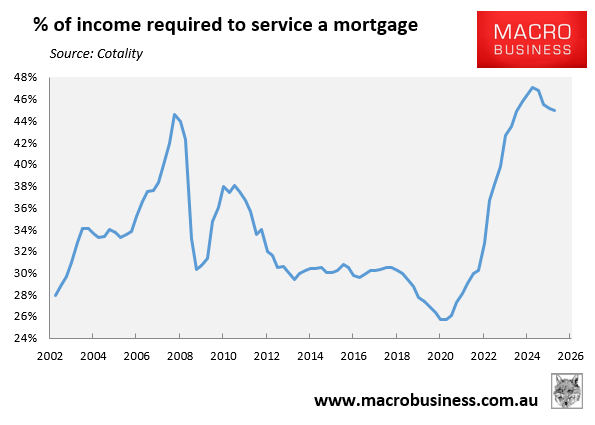

Despite the three 0.25% interest rate cuts from the Reserve Bank of Australia (RBA), the percentage of household income required to service a new mortgage on the median-priced home remained at an historically high 45% in Q3 2025, still above the Q1 2008 GFC peak:

Consequently, the affordability of Australian housing remains stretched. And with the RBA now expected to keep interest rates on hold for the foreseeable future, this stretched affordability should put a ceiling on the house price upswing.

Indeed, REA Group Senior Economist Eleanor Creagh made this exact argument in the media release accompanying PropTrack’s October house price results:

“Population inflows, a lift in investor activity, and the expanded Home Guarantee Scheme have reinforced demand, alongside this year’s series of interest rate cuts”, Creagh noted. “At the same time, total stock on market has been tight, and the delivery of new housing remains constrained, tilting conditions toward sellers. These factors point to further price gains through summer”.

“However, monthly growth eased across the capitals from October’s stronger pace, and with interest rates now expected to remain on hold for an extended period, affordability constraints are likely to see price growth moderate throughout 2026”.

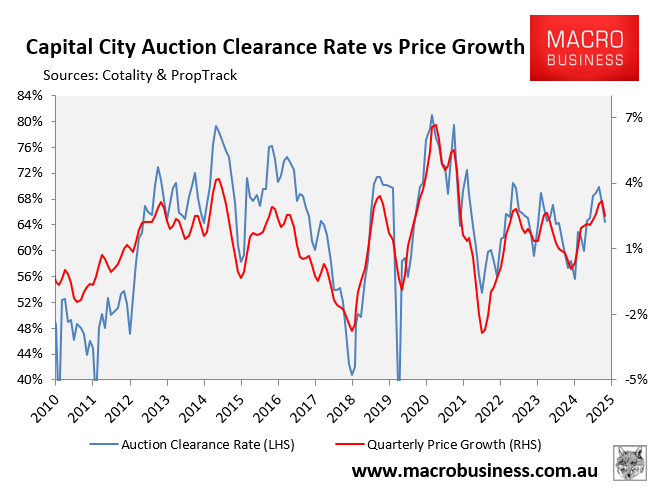

Already, we are beginning to see the impact of the affordability ceiling on demand and price growth.

As illustrated below, the final national auction clearance rate has trended lower since September, whereas quarterly dwelling value growth softened in November.

While the Albanese government is doing its best to juice prices via its 5% deposit scheme for first home buyers, the Help to Buy shared equity scheme, and mass immigration, ultimately without further interest rate relief from the RBA, mortgage affordability will remain stretched, and the market will stall in 2026.