DXY is breaking out still.

AUD rebounded in its fading trend.

CNY meh.

Gold trying to hold.

AI metals a better day.

The chosen one bounced.

EM too.

Junk held.

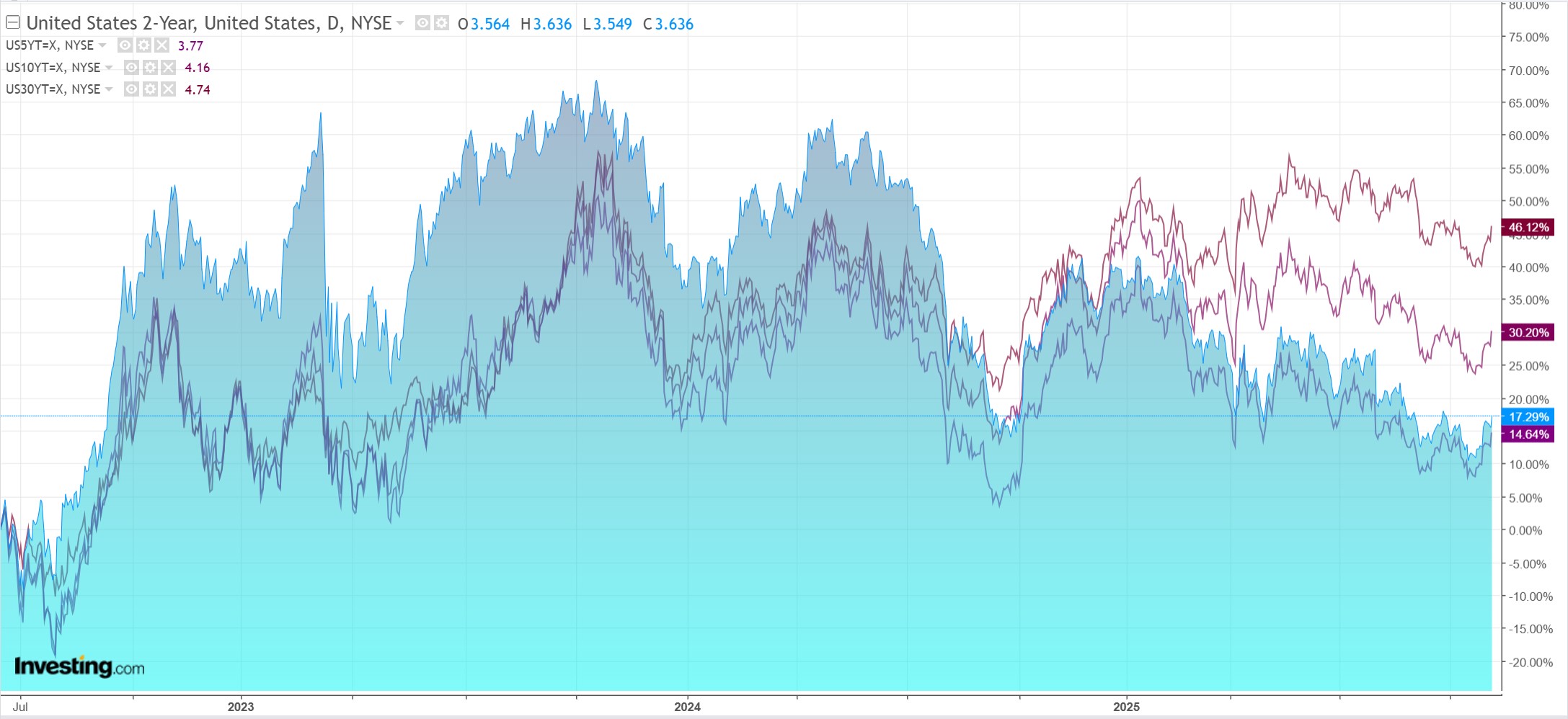

But there’s trouble in them thar yields.

Stocks rose anyway.

I remain cautious on the crap complex—commodities, EM, AUD—while the bond backup and rising DXY run hand-in-hand.

UBS is strident.

The AUDUSD has fallen by 0.6% despite the Reserve Bank of Australia (RBA) holding the cash rate steady (which was widely expected), a press conference revelation that a cut was not even considered, and core inflation forecasts raised so that the mid point of 2-3% band isn’t achieved over the outlook horizon.

RBA Governor Michele Bullock’s comments in the press conference reflected lessons learned about not providing forward guidance.

We retain our view of one more cut in May 2026, but see scope for rates to stay on hold at 3.60% if recent weakness in payrolls data proves temporary (next print on 14 November) or inflation more persistent.

In the end, we “bang the table” to be long the AUDUSD at these levels, reiterating our target of above 0.70 by mid-2026.

It’s never a good idea to bang on the table when it comes to forex. You’re more than likely to accidentally punch yourself in the face.

I remain blandly committed to a higher AUD but see the RBA being mugged by unemployment and Jay Powell being a pest before he is ejected next year.

Moreover, if DXY firms as US growth prospects lift out of the shutdown, the entire crap complex is going to stay under pressure.

UBS needs a new Trump convulsion, which, frankly, is certain, which is why I see AUD higher as well from here.

Just not 70 cents.