This week saw the release of two important housing affordability reports from Cotality and Proptrack.

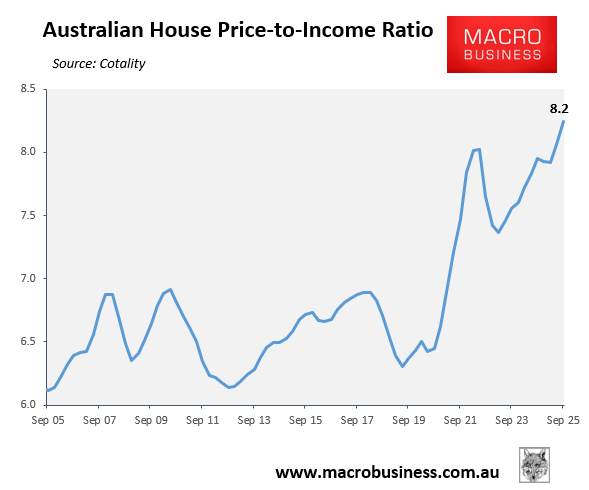

Turning to Cotality’s report first, it showed that the median home price relative to median household income nationally hit a record high of 8.2 in Q3 2025, up from 6.4 five years earlier in Q3 2020.

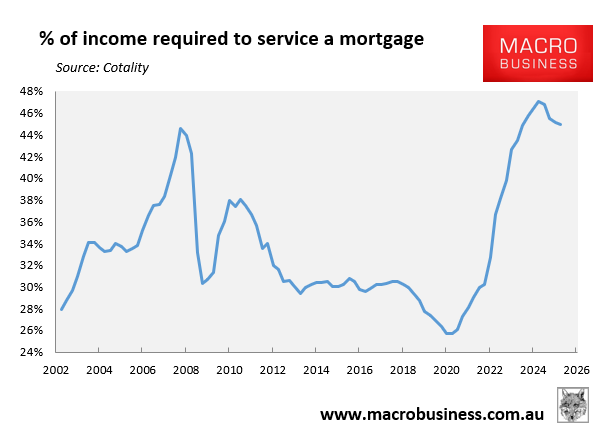

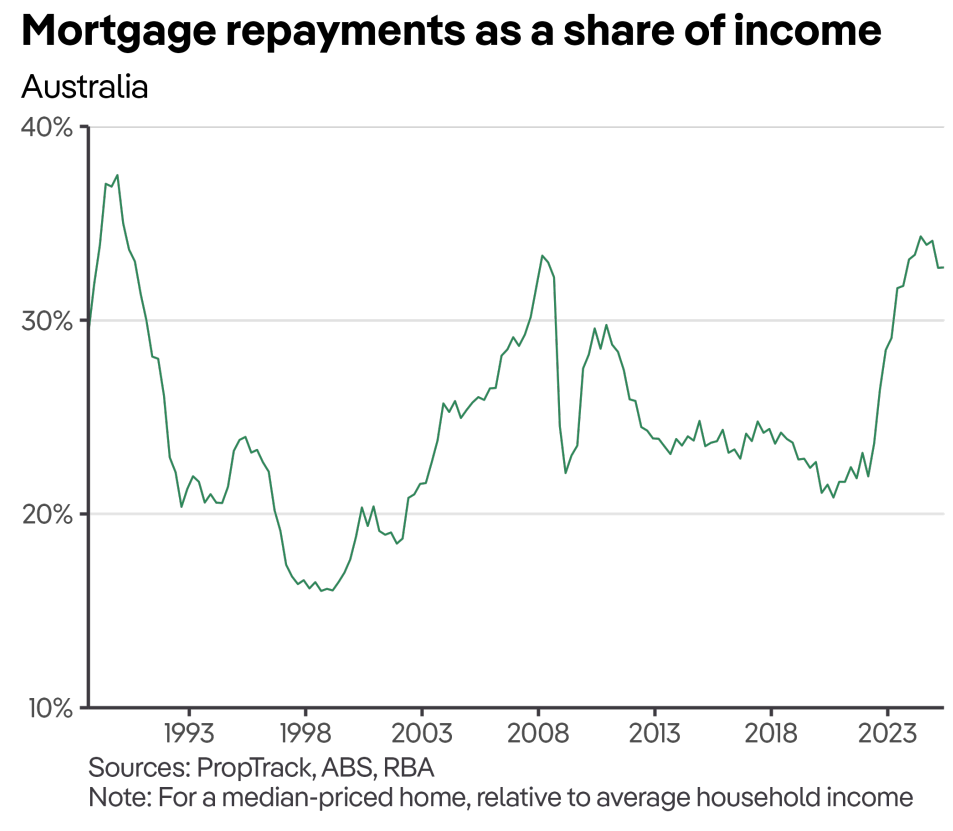

The amount of income that a median household must spend to service a new mortgage on the median-priced home has also surged, reflecting rising prices and interest rates.

At the national level, a median household purchasing a new median-priced home needed to spend 45.0% of its income on mortgage repayments in Q3 2025, up from 25.7% in Q3 2020.

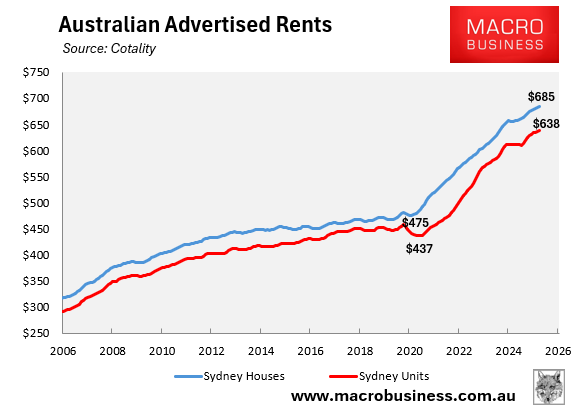

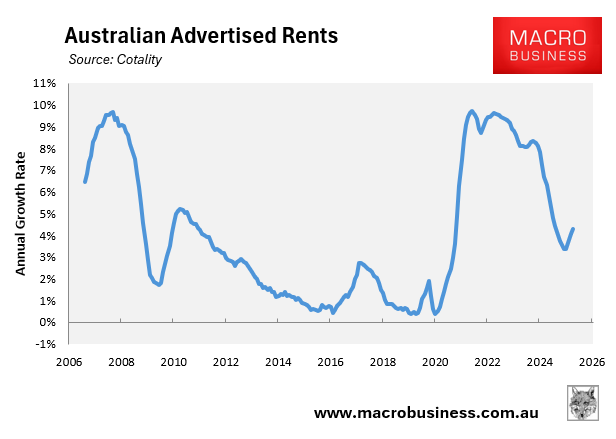

Rental affordability in Australia has also collapsed to its worst level on record.

At the national level, advertised rents surged by 44% in the five years to Q3 2025.

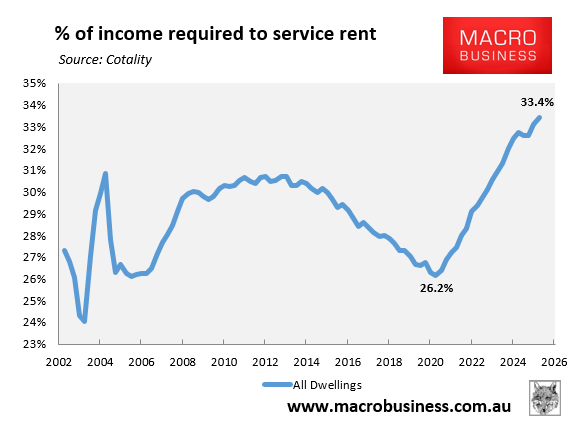

As a result, the percentage of income required to meet rental payments on the median home has surged to 33.4% as of Q3 2025, up from 26.2% five years earlier.

PropTrack’s housing affordability report tells a similar story.

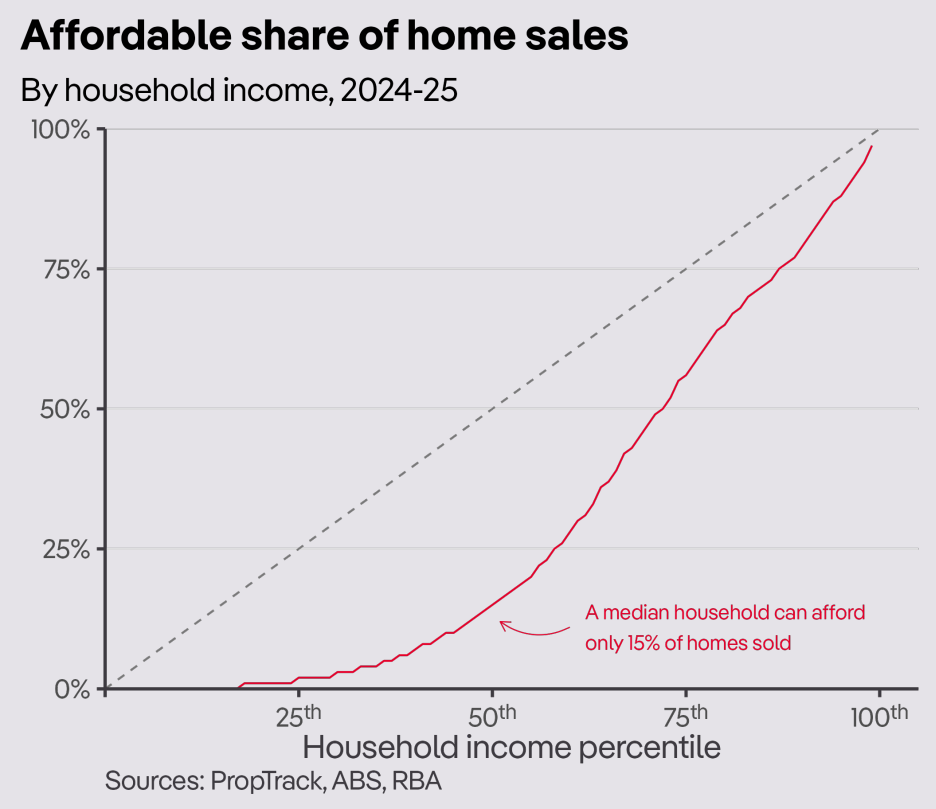

PropTrack estimates that a median household could only afford 15% of homes sold in 2024-25, based on a household spending 30% of their gross income on mortgage repayments, and a 2.5% buffer for assessment above the most-recent average new mortgage rate, and assuming they have access to a 20% deposit and the costs of purchasing (such as stamp duty):

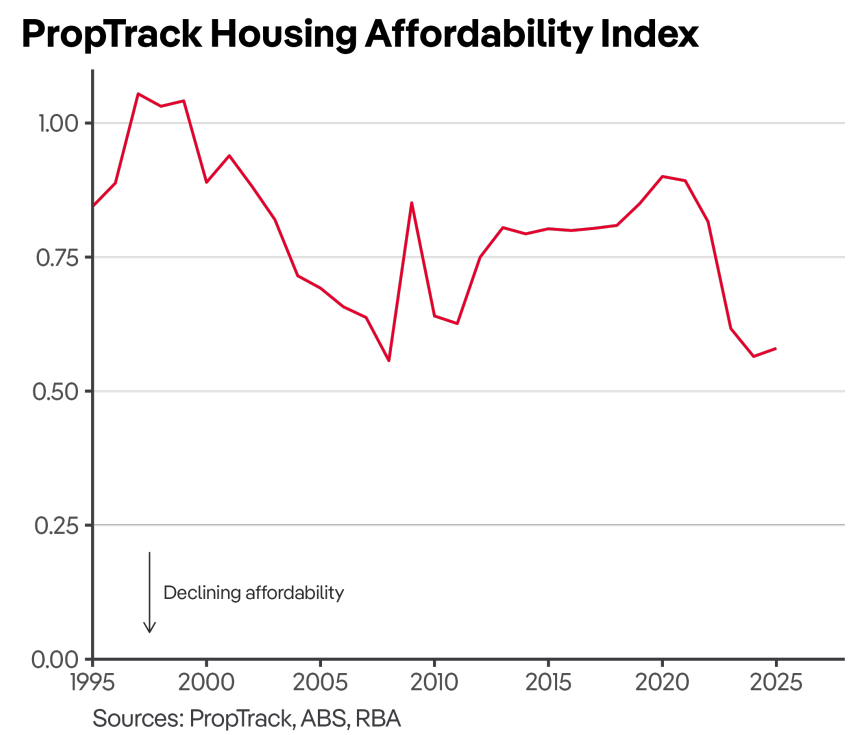

As a result, PropTrack’s housing affordability index is tracking just above record lows:

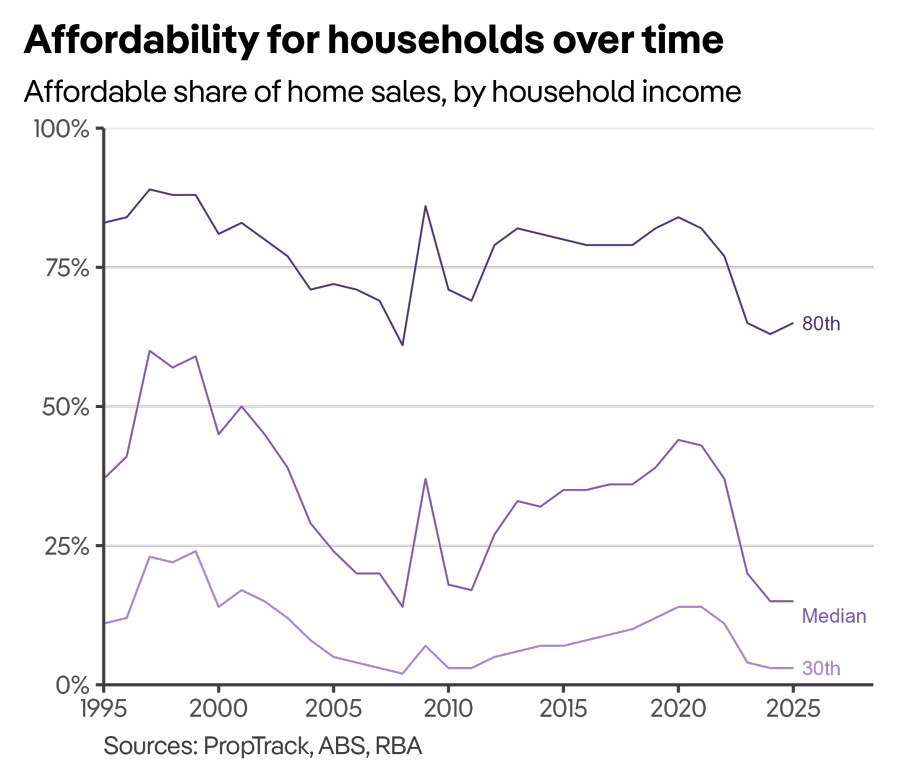

As expected, affordability is most stretched for lower-income households, with a household at the 30th income percentile only able to afford to buy just 3% of homes in 2024-25:

With home values continuing to rise, the slight recent improvement in purchase affordability has been caused by the RBA’s three interest rate cuts:

Affordability outlook remains bleak:

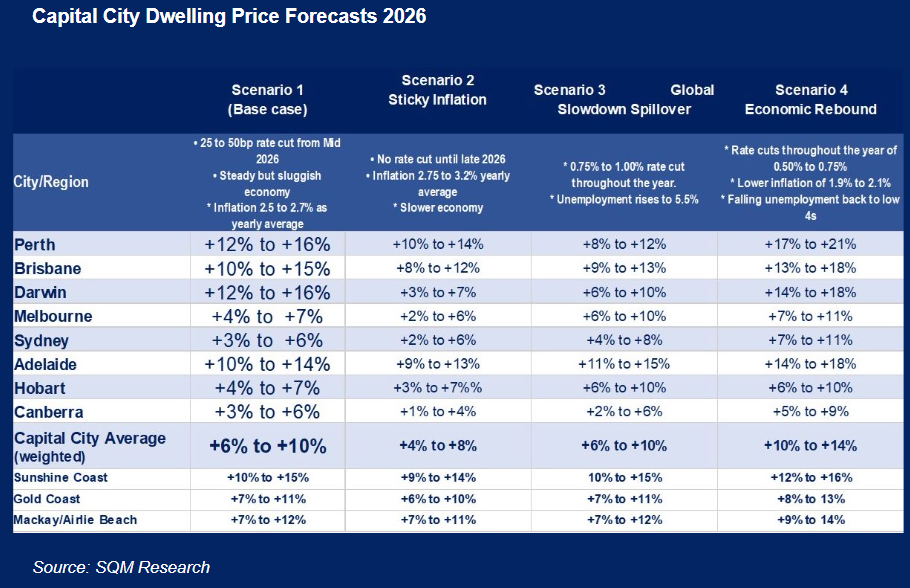

SQM Research forecasts house price growth above income growth in 2026, whereas the RBA is expected to keep interest rates on hold for the foreseeable future.

As a result, purchase affordability will inevitably decline in 2026.

Cotality has also reported record low rental vacancy rates and rising advertised rents, which should worsen rental affordability in 2026.

In summary, the misery machine that is the Australian housing market should worsen in 2026.