By Lucinda Jerogin, Associate Economist at CBA:

- The September quarter headline CPI materially surprised to the upside, jumping 1.3%/qtr to be 3.2% higher annually. The policy-relevant trimmed mean measure accelerated to 1.0%/qtr and 3.0%/yr.

- Offshore this week the FOMC and BoC cut rates by 25bp, as was widely expected. However, a more hawkish tone curtailed expectations of future cuts in the US. Elsewhere, the ECB and BoJ kept policy rates on hold as anticipated.

- President Trump met with Chinese President Xi on the sidelines of the APEC summit in South Korea. The US Government shut down entered its fifth week amid political gridlock.

- The week ahead will see the RBA hand down its November Monetary Policy decision. We expect the RBA to keep the cash rate at 3.60% for a prolonged period. The ABS MHSI, goods trade balance and building approvals are also due.

- Abroad, the BoE meets. Our international economics team expects the BoE to keep the bank rate unchanged at 4.0%.

It was a week full of surprises that kept global financial markets on their toes. Domestically, the September CPI threw a spanner in the works, materially surprising to the upside. Headline CPI jumped 1.3%/qtr to be 3.2% higher annually. The policy-relevant trimmed mean measure accelerated 1.0%/qtr and 3.0%/yr, above ours and the consensus forecast for a 0.8% quarterly upturn.

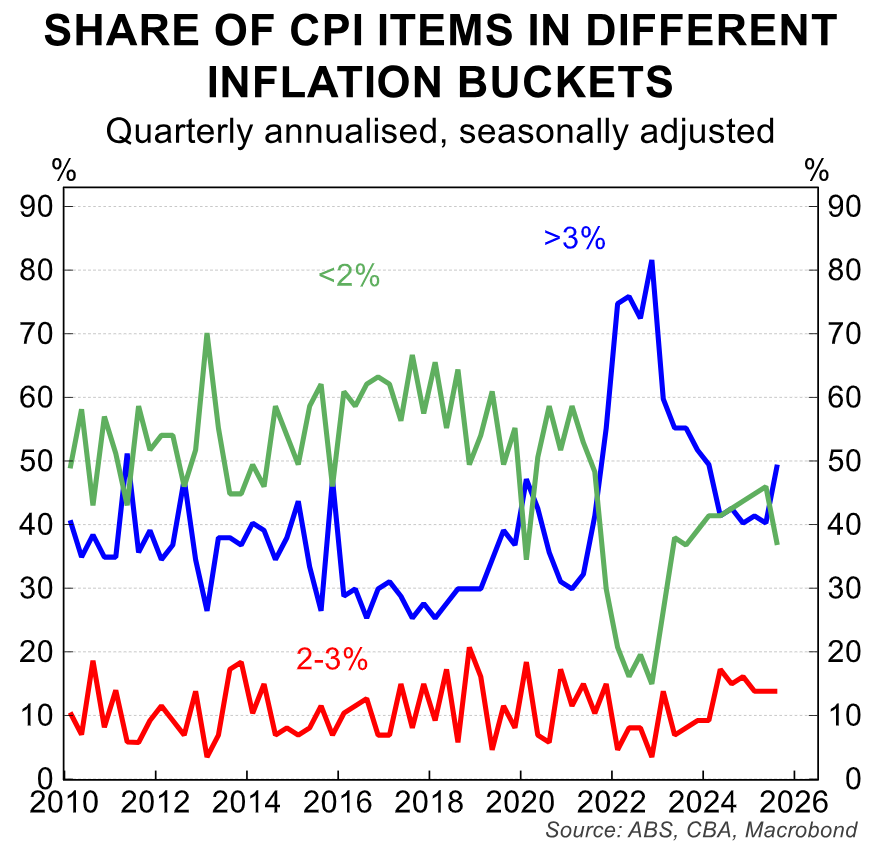

The key shock was how broad-based the acceleration in inflation was across individual CPI components. The share of CPI categories experiencing inflation above the top of the RBA’s target band increased from 37% in Q2 to just under 50% in Q3. This sees the share of prices experiencing higher inflation increase to be well above its pre-pandemic average and reverses its previous downward trend.

Given the material upside surprise to the Q3 CPI, we have updated our RBA call to expect rates to remain on hold from here. Previously, we anticipated one final cut in February 2026 to bring the cash rate back closer to neutral.

However, the economic backdrop shifted over the third quarter. The cyclical upswing has occurred larger and faster than expected. The consumer has been at the heart of this, as we have been flagging based on our internally generated data.

With the stronger inflation data this week, and assuming quarterly trimmed inflation returns to an optimistic 0.6% run rate over coming quarters, trimmed mean CPI could sit at 2.9%/yr through till later in 2026.

In addition, Michele Bullock’s remarks on Monday confirmed the Board still views the labour market as ‘slightly tight’. As a result, we expect the RBA will conclude that monetary policy should remain slightly restrictive, keeping the cash rate at 3.60% for a prolonged period.

We expect it would take a material move higher in the unemployment rate, together with more moderate inflation prints, to bring the RBA to cut.

Other data releases this week came in the form of trade prices and private sector credit.

In Q3, goods import, and export prices fell by 0.4%/qtr and 0.9%/qtr, respectively. The print implies a slight decline in the terms of trade and confirmed the upside surprise to inflation this week was not sourced from offshore.

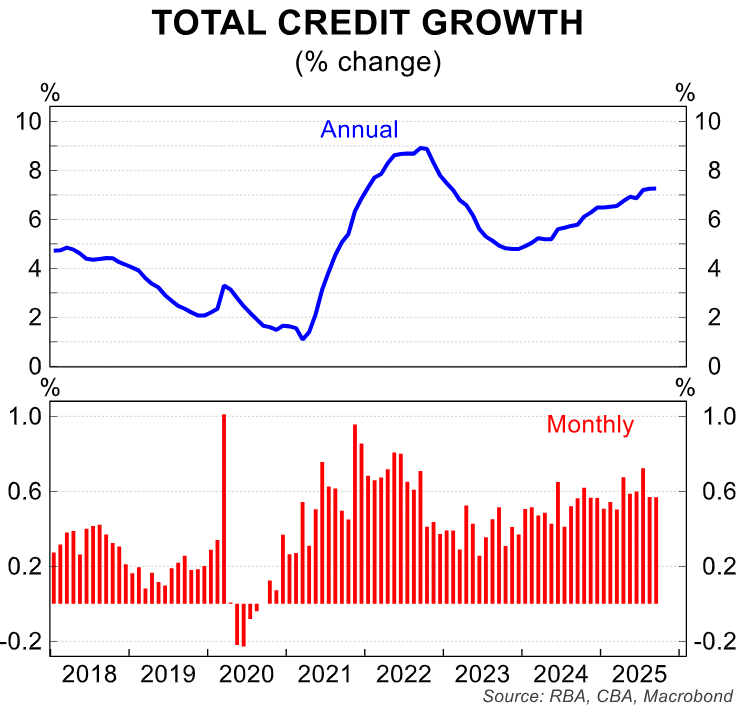

Private sector credit rose 0.6%/mth and 7.3%/yr.

Offshore, news was rich with updates on trade deals, central bank meetings, and economic data.

President Trump continued to make headlines, meeting with many country officials on the sidelines of the APEC summit in South Korea. Most notably, the US President met with Chinese President Xi for the first time since 2019. The two leaders reportedly reached several agreements including a one-year trade truce, a reduction in the US’s fentanyl tariff on imports from China from 20% to 10%, and a pause to China’s rare-earths licensing regime.

However, markets were not ready to jump with joy. Key issues remain unresolved. In our view, the US and China will remain at odds in their struggle for global economic and military dominance.

In the world of central banks, the hawks were in full flight this week. In the US, the FOMC cut the Funds rate by 25bp to 3.75-4%, as expected. However, markets were taken aback by Chair Powell’s hawkish tilt in the post meeting press conference as he hosed down expectations for further policy easing.

December being ‘far from’ a foregone conclusion. These comments pulled back market pricing for December from fully priced to two thirds and pushed up the terminal rate to 3.14%.

Nonetheless our international economics team continues to expect the FOMC to cut the funds rate at their next meeting in December.

North of the border, the BoC reduced its benchmark rate to 2.25%, as expected. However, the BoC also pushed back on expectations for further rate cuts. The benchmark rate now sits at the bottom of the BoC’s estimate range of the neutral cash rate.

Elsewhere the ECB and BoJ kept rates on hold as expected. ECB President Lagarde reiterated the economy is ‘in a good place’, noting the economy has continued to grow despite the challenging global environment.

Closer to home in Japan, the BoJ kept its policy interest rate at 0.5% in a 7-2 decision. The two dissenters voted for a 25bp rate hike; however, the accompanying statement was absent of hawkish signals.

The week ahead will see the RBA November Monetary Policy decision. As mentioned, we expect the RBA to keep the cash rate on hold at 3.60% for a prolonged period and the tone to turn hawkish.

The ABS MHSI, goods trade balance and building approvals data are also due.

Abroad, the Bank of England Meeting will be the global highlight. Our international economics team expects the BoE to keep the bank rate unchanged at 4.0%. In their view, inflation and wages growth remain too high, and the BoE may choose to hold rates steady until there is more fiscal policy uncertainty.