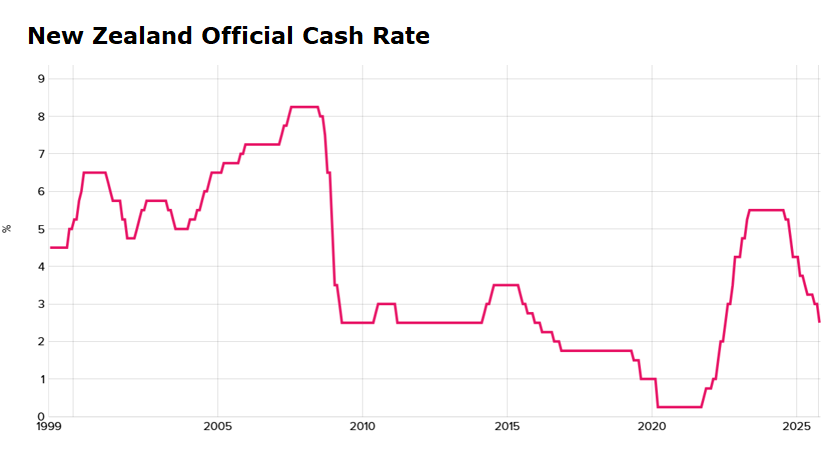

The Reserve Bank of New Zealand has slashed the official cash rate by 300 bps to 2.5%.

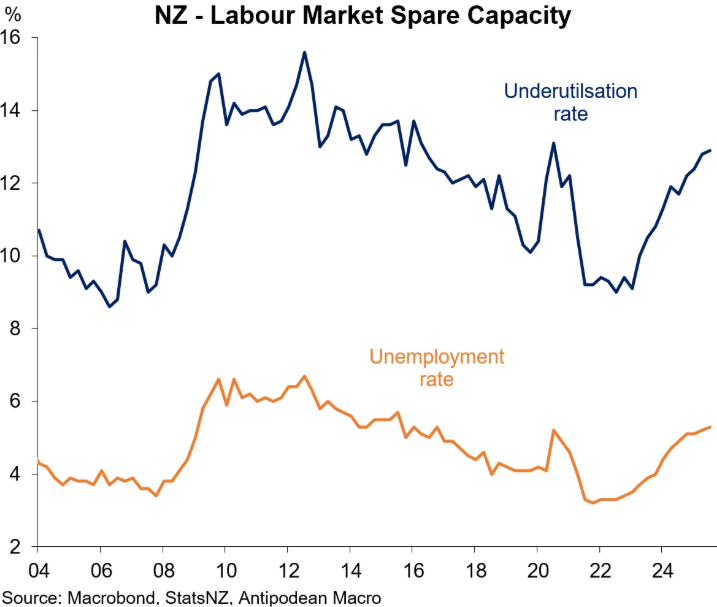

Given New Zealand’s weak economy, which last week saw unemployment and underemployment increase to their highest rate since the pandemic peak, expectations are that the Reserve Bank will deliver additional rate relief heading into 2026.

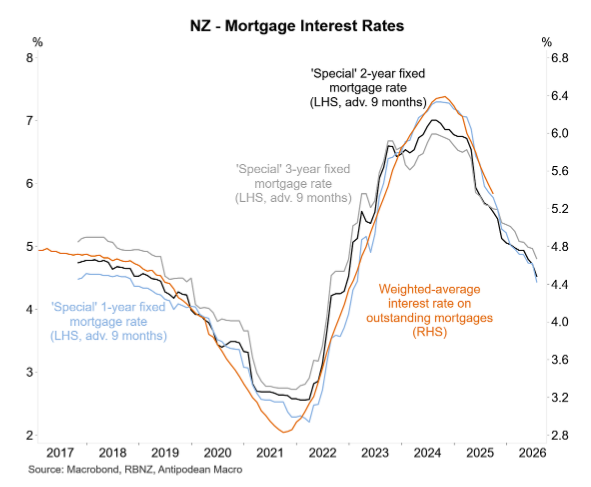

As illustrated below by Justin Fabo from Antipodean Macro, New Zealand mortgage rates have fallen sharply in response to the Reserve Bank’s monetary easing:

The interest rates on new one- and two-year mortgages are now tracking at levels last seen in 2017-18, prior to the pandemic.

Normally, such a sharp decline in mortgage rates would be associated with rapidly rising housing prices, due to the positive impacts on borrowing capacity and loan serviceability.

However, this time around, there has been no such rebound.

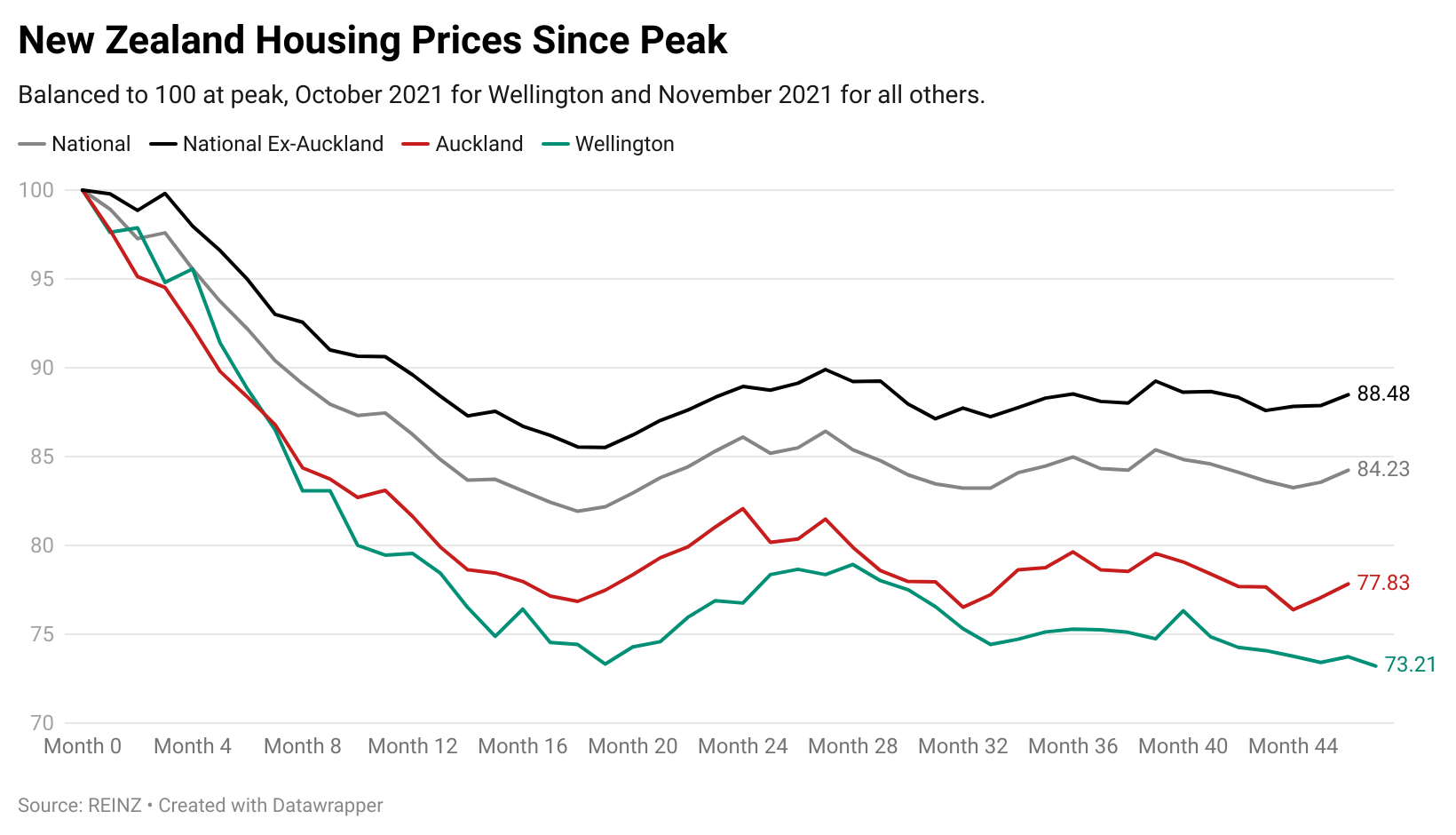

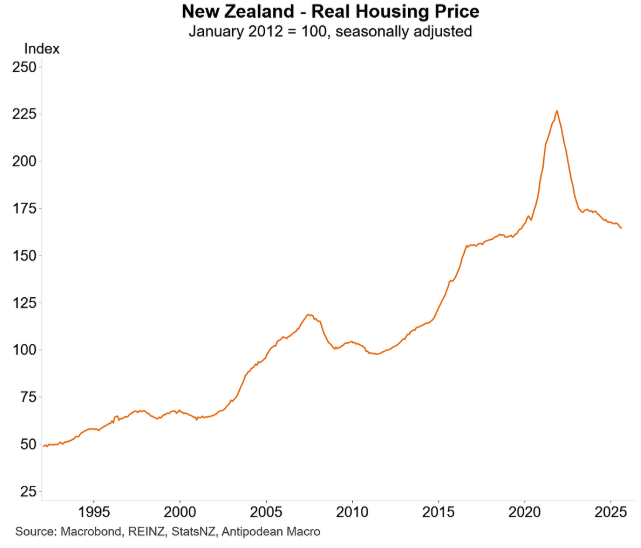

As Tarric Brooker shows below, New Zealand home values have fallen by 11.5% from their peak in October 2021:

In real inflation-adjusted terms, national values have crashed back to 2019 levels and continue to decline:

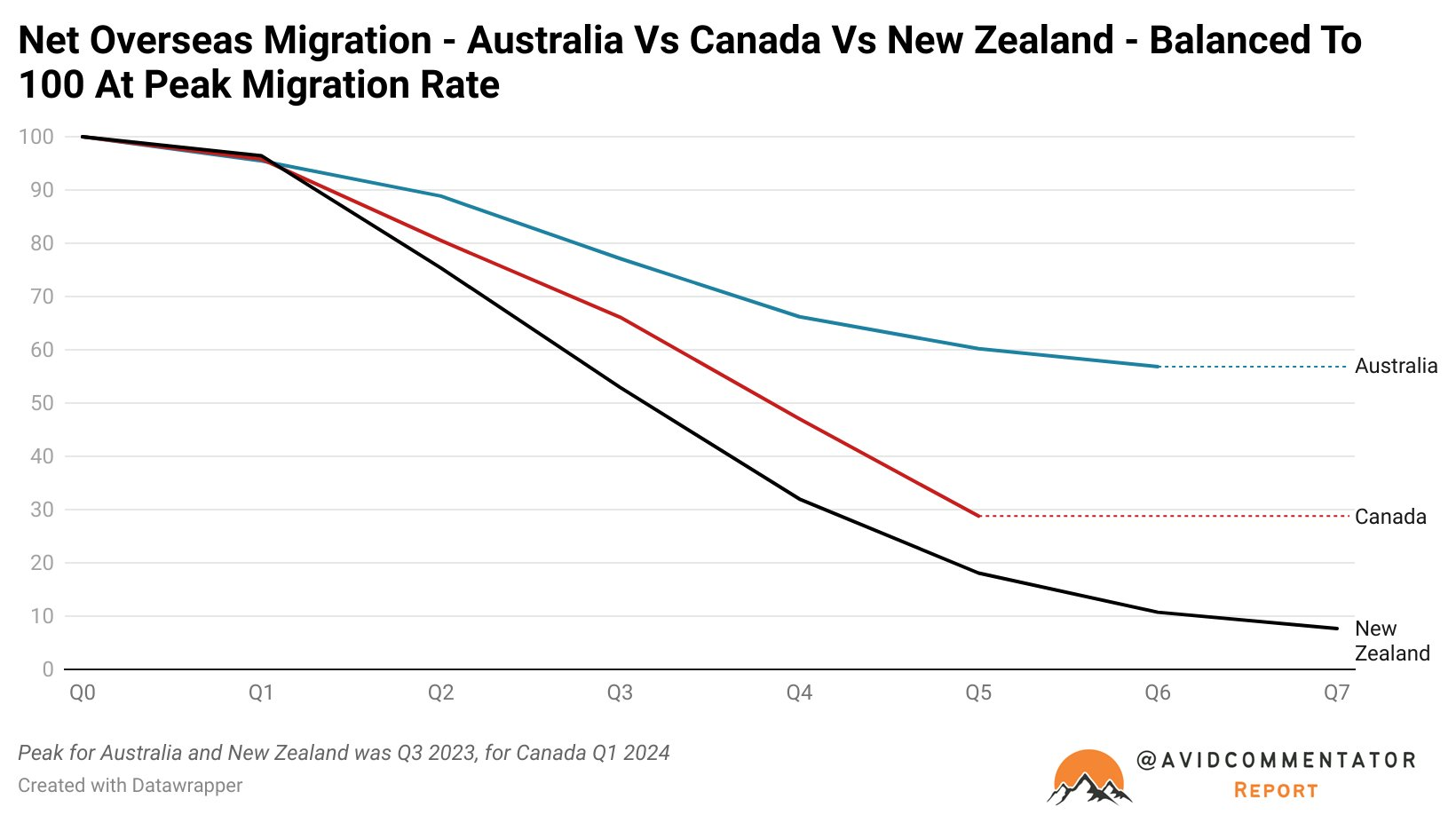

Despite the crashing mortgage rates and improved affordability, New Zealand’s housing prices continue to be weighed down by sharply lower immigration:

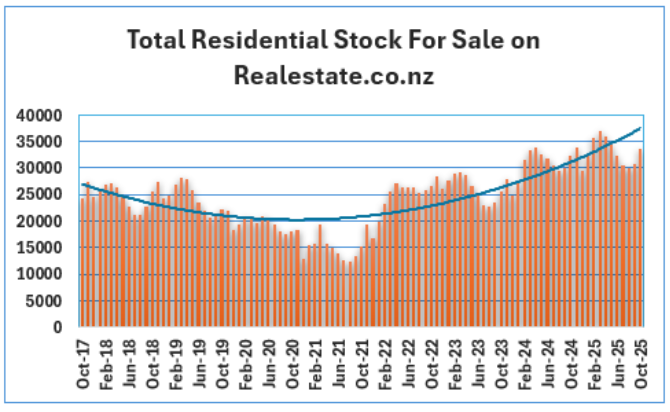

The volume of homes listed for sale in New Zealand is also tracking at decade highs.

As reported by Greg Ninness at Interest.co.nz, Realestate.co.nz received 12,209 new residential listings in October, which was 5.5% higher than October last year and the most for the month of October since 2018.

“This helped push the total stock of properties for sale on Realestate.co.nz to 33,588 at the end of October, up 3.9% compared to October last year and the highest for an October month since 2014”, noted Ninness.

“That will ensure potential buyers have plenty of properties to choose from at the start of the summer season and will likely maintain the buyer’s market conditions that persisted through winter, which helped to keep a lid on property prices”.

The combination of historically low immigration and high for-sale listings is currently outweighing the stimulus from lower mortgage rates.