The housing market appears to have lost some momentum due to the recent inflation shock and expectations that the Reserve Bank of Australia (RBA) will keep interest rates on hold for the foreseeable future.

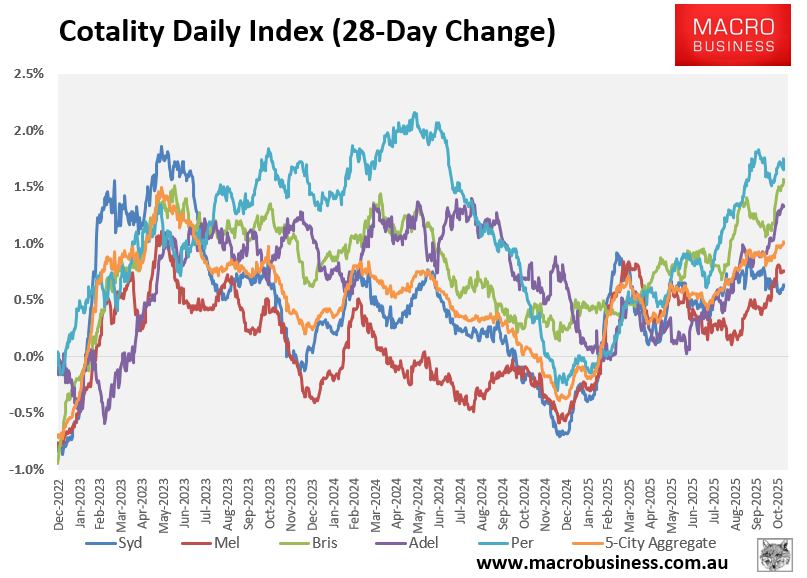

Cotality’s daily dwelling values index continues to show the strongest growth in over two years, measured on a rolling 28-day basis:

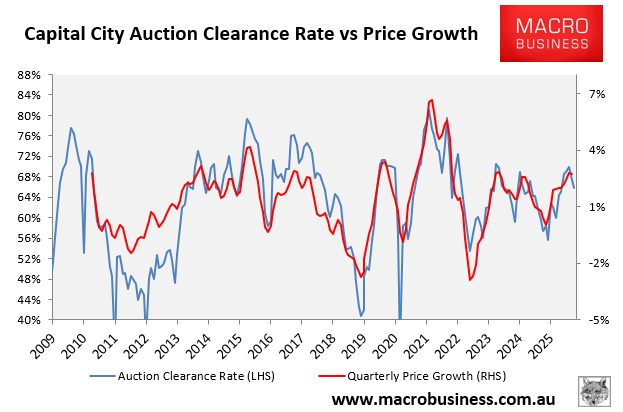

However, auction clearance rates have softened materially, as illustrated below, which is generally a leading indicator of dwelling value growth:

Indeed, despite nine out of 10 auctions selling, leading Sydney auctioneer Tom Panos reported over the weekend that the market has “come to a bit of a reality check”, with the “high levels of fear of missing out (FOMO) over the last month” dissipating “because the narrative of interest rates has changed significantly”.

“We were led to believe that we were going to have a rate cut on Melbourne Cup Day”, Panos added. “That did not happen. And what’s also interesting is that the commentary that the Reserve Bank gave when they announced there was no rate cut on Tuesday was that there probably won’t be a rate cut for some time”.

“When you interview bankers, who are the most senior people in the institutions, they’re actually saying that most likely a rate cut no sooner than the middle of next year”.

“This is not a bad thing because I was seeing a little bit of a frenzy happening, and that frenzy was mostly happening at the under $2 million mark, specifically the lower end of the market in each state. And that’s been fueled by the amount of buyers that are taking advantage of the 5% deposit scheme that allows you to borrow 95%”.

Panos also warned that buyers utilising the federal government’s 5% deposit scheme risk being caught out when interest rates inevitably rise.

“You don’t want to fall into the trap that a lot of the 95% borrowers did back in 2007”, Panos said, in reference to the US sub-prime mortgage crisis.

“I believe that borrowing 95% on a principal place of residence is high risk if you don’t have amazing income. Because when rates do go up, and they will, you’re going to be in a position of having a 95% loan at a higher loan repayment than now”.

“So, what I’m saying is get comfortable with your current position because you don’t want to be in a situation in the years to come where rates go up, loan repayments go uncontrollably high, and then people are stuck”.

Sadly, the Albanese government’s 5% deposit scheme for first home buyers has added unnecessary fuel to the housing bonfire and will likely create an entire generation of over-leveraged mortgage serfs.

The only positive aspect is that the RBA is no longer exacerbating the situation by further lowering interest rates.

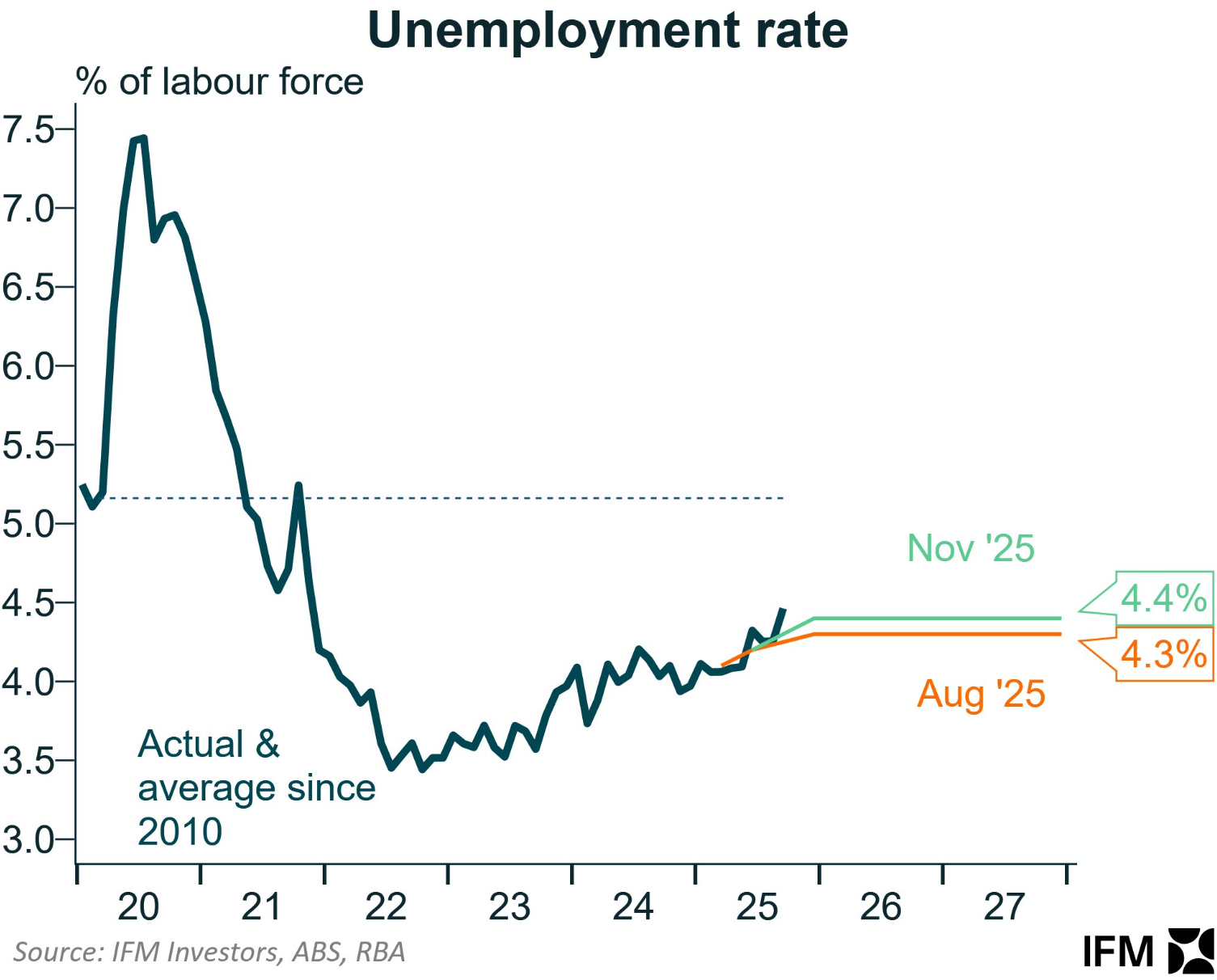

However, if the unemployment rate surges significantly higher than the RBA’s optimistic forecasts, additional rate relief could arrive in mid-2026.