ANZ has a few nice charts showing how labour costs have nothing to do with the recent inflation pop.

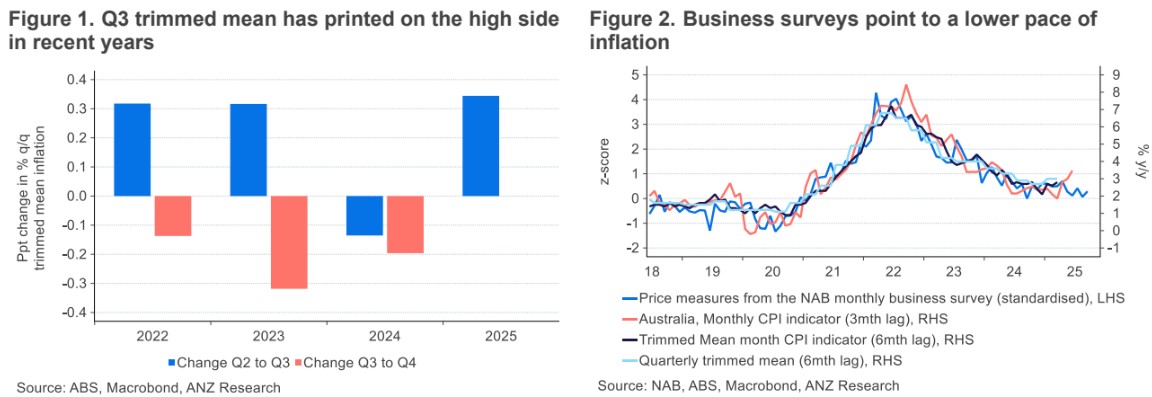

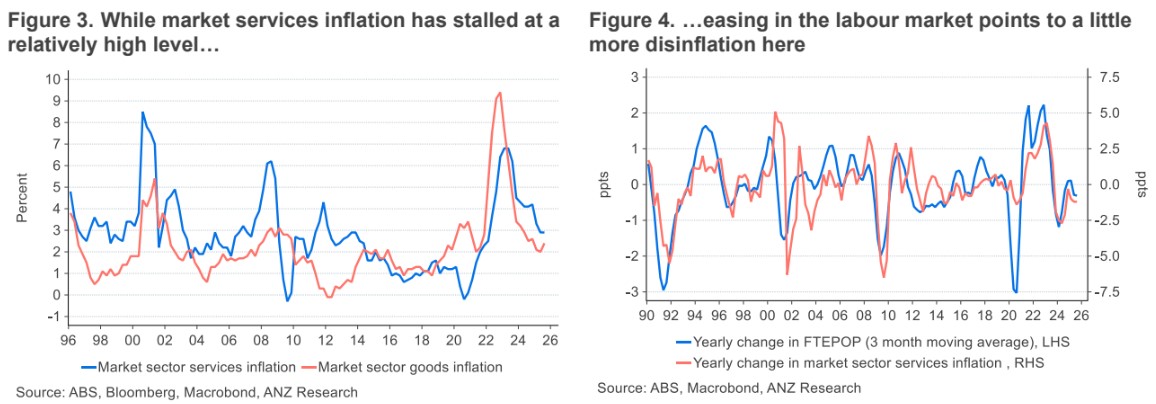

The Q3 trimmed mean inflation print is likely to have been a ‘one-off’.

Several factors point to that conclusion, including business survey price and cost measures, the tendency for Q3 inflation prints in recent years to come in on the high side, the easing in labour market conditions, gains in the AUD Trade Weighted Index (TWI) and recent trends in oil prices.

Overall, the balance of top-down inflation indicators and influences suggests inflation is likely to moderate over the coming year.

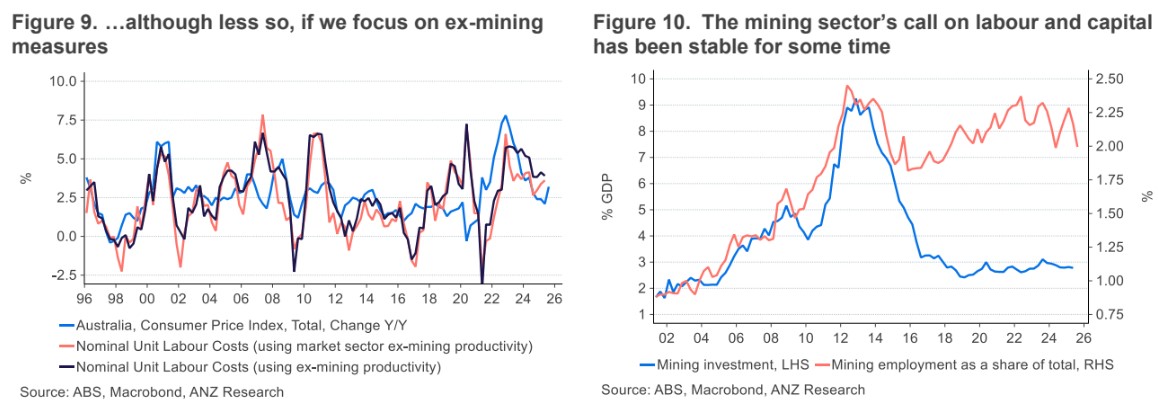

Hers is the kicker for labour pressures, which continue to fade.

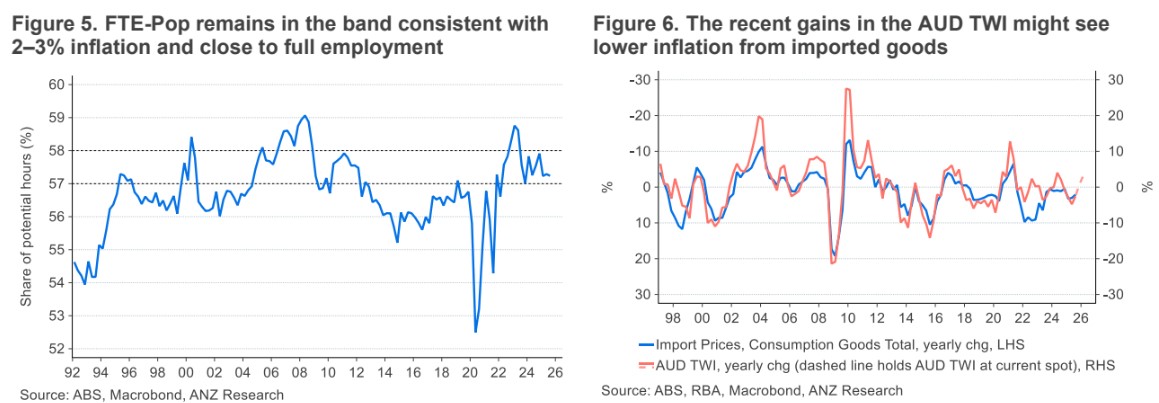

These indicators are consistent with inflation within the band.

Especially in market services, the area that is so bothering the RBA.

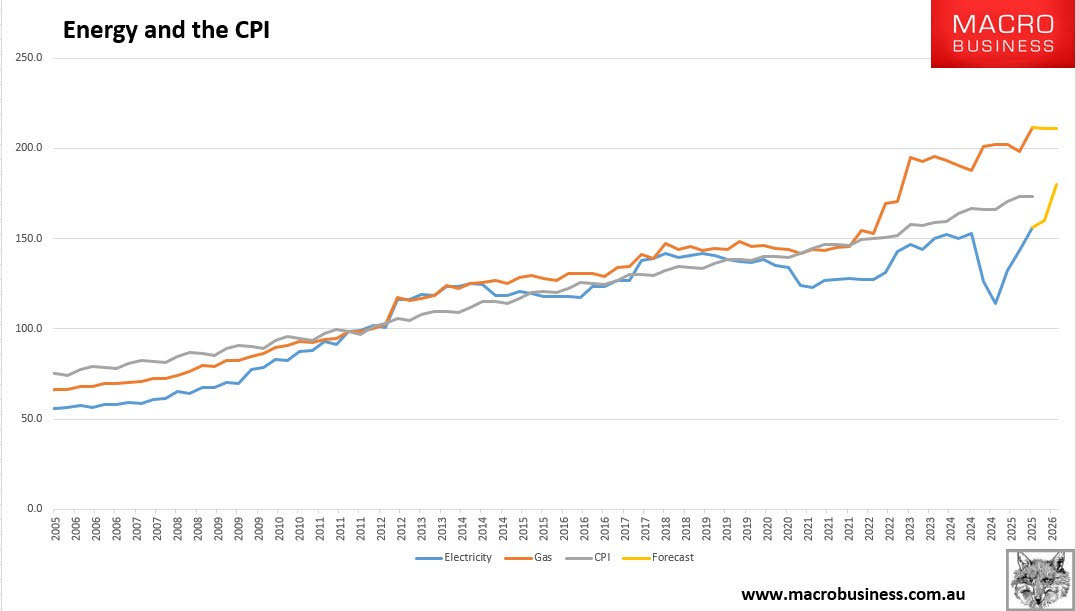

Everybody outside of the RBA’s asbestos ivory tower knows the real cause of the inflation rebound: the Energy shock.

My view remains that unemployment is going higher and rates lower than most expect. Especially so after the RBA panic.

The Bullock RBA is probably the dumbest I have seen, and that is saying something.