Cotality’s house price results for October noted that values are growing more strongly at the lower-to-middle end of the market.

Across the combined capital cities, dwelling values in October rose by 1.4% across the middle market and by 1.2% across the lower quartile, while the upper quartile values increased by only 0.7% over the month.

Cotality research director Tim Lawless noted that competition from first home buyers and investors was fueling the stronger growth across the low-to-middle market.

“Stronger housing demand at the lower price points is likely a culmination of serviceability constraints eroding purchasing power, persistently higher than average levels of investor activity, and what is likely a pickup in first home buyers taking advantage of the expanded deposit guarantee”, Lawless said.

At the same time as Labor’s 5% deposit scheme is stimulating first home buyer demand, investor demand is also surging.

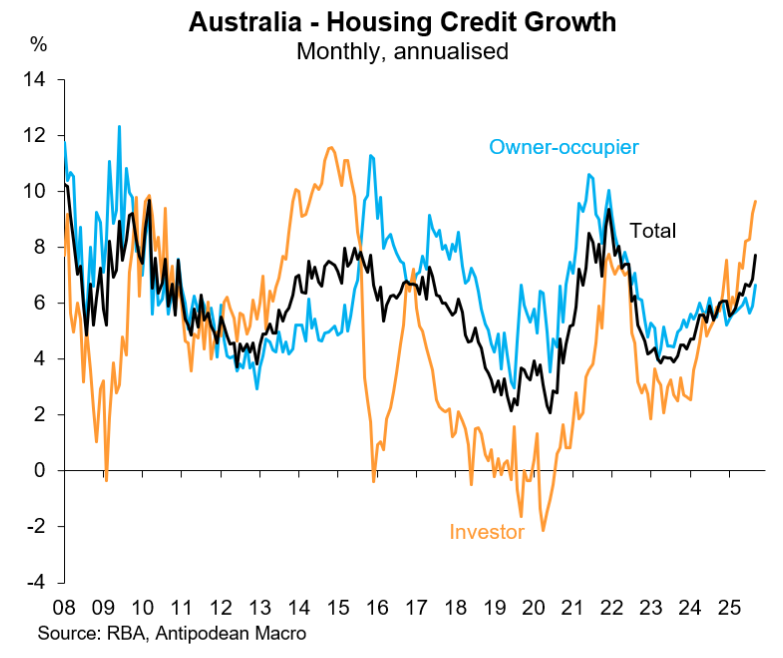

As illustrated below by Justin Fabo from Antipodean Macro, investor housing credit growth has surged, rising by around 10% on a monthly annualised basis in September, the strongest growth in a decade.

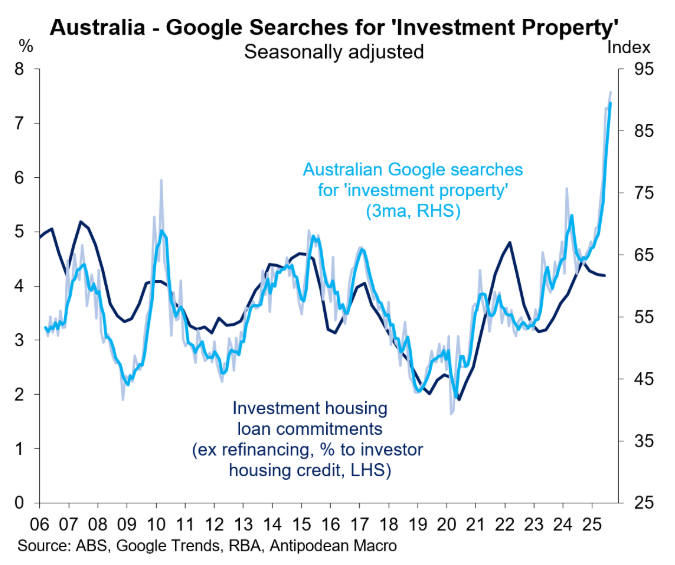

A few weeks back, Fabo posted the following chart showing that Google searches for “investment property” had surged to their highest level in at least two decades:

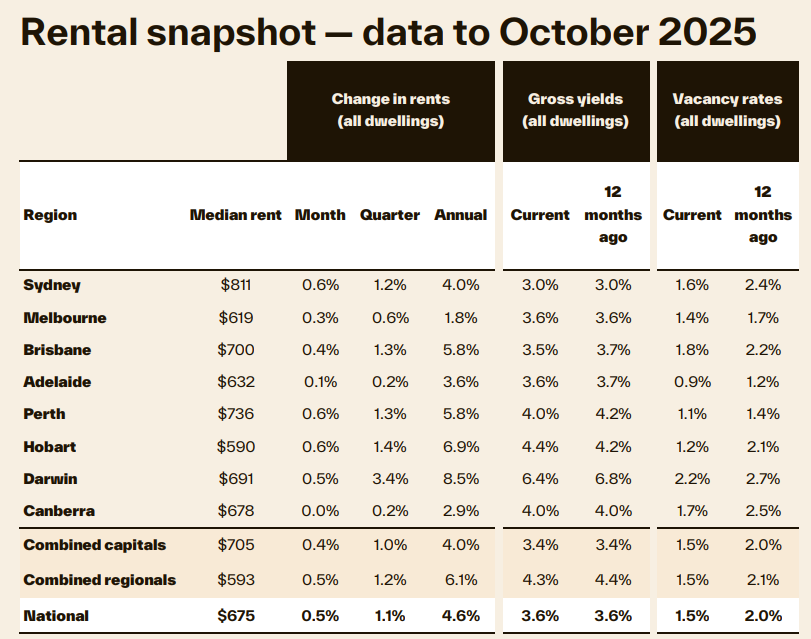

Investors are likely being enticed into the market by the structural shortage of housing, which has seen rental vacancies collapse to record lows, according to Cotality.

Source: Cotality

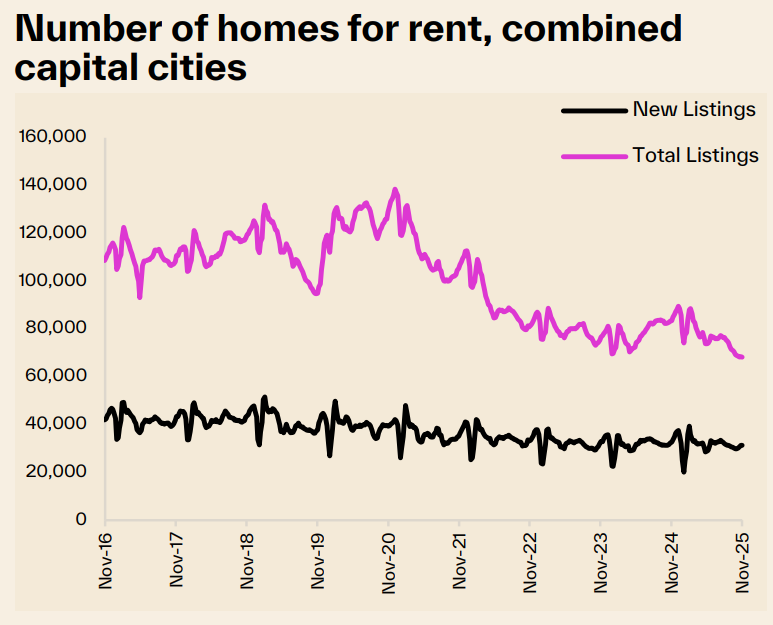

Rental listings have also collapsed to a record low following an 18.2% annual decline:

Source: Cotality

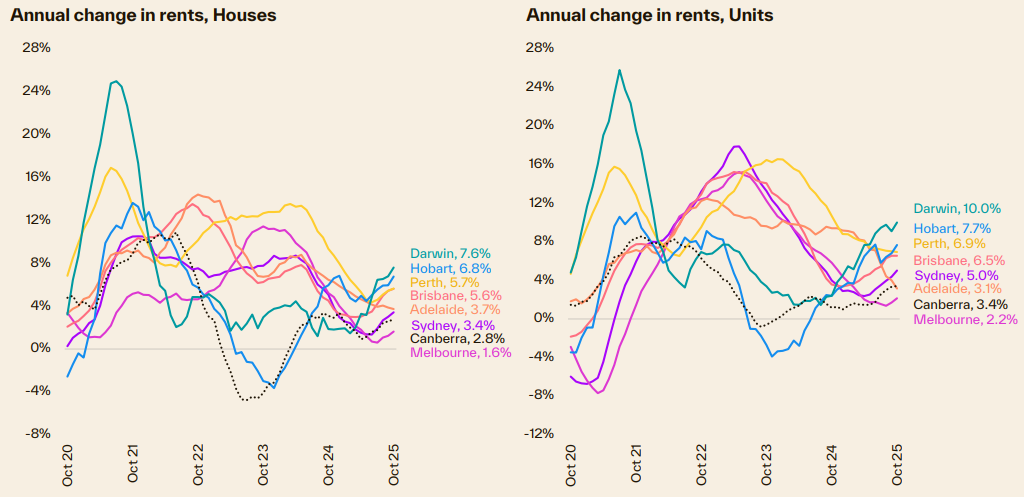

As a result, rents are climbing once again. Cotality’s national rental index has risen by half a percent per month over the past three months, the highest monthly growth in rents since May 2024.

After slowing through 2024, the annual trend in rental growth is once again on the upswing across most cities:

Source: Cotality

Therefore, investors are seeking to profit from rising values and rents, increasing competition with first home buyers.

With supply remaining tight, these forces will inevitably see prices rising further from their already lofty heights, led by the more affordable end of the market, even in the absence of further rate cuts.

The prospect of further price rises is obviously terrible news for Australian housing affordability, which already ranks among the worst in the world.